The US Now Exports More Energy Than It Imports

Yesterday the Energy Information Agency released their monthly snapshot of energy markets data for the United States. Much of the data is somewhat lagged; the data discussed in this post is only updated through May.

Our first chart highlights the huge shift away from coal and towards natural gas as an energy source, driven by both regulation and the economics of fracking. Also notable is the growth of wind and solar energy; solar especially is having an incredible year as production has risen an astounding 140% annualized in 2020.

The other recent shift in the domestic energy market is the COVID-driven plunge in petroleum share of total energy output. In April, petroleum fell below one-third of total US energy consumption as driving activity plunged. Obviously, this is very short-term and will rebound, but the growth of renewables and natural gas amidst the decline of coal will continue, unlike shorter-term trends like the highest share of nuclear power consumption on record.

We also wanted to highlight the energy trade balance. Historically, the US has imported vastly more energy than it has produced, but the massive expansion of domestic oil and natural gas production has reversed that precedent entirely.

As shown below, the US went from importing 2.5 trillion more BTUs of energy than it produced back in 2006 to exporting more energy than it imports beginning in August of last year. “Energy independence” isn’t a realistic or helpful goal, because large gross trade flows can increase efficiency, but on a net basis, the US has now been energy independent for about a year. This post was originally published in our post-market macro report — The Closer — on 9/14/20. Click here to start a free trial to Bespoke Institutional and receive our nightly Closer for the next two weeks, featuring more commentary and data on macro markets.

Lumber Squeezed, But Savings Super A Few Months Out

Today is the last day of trading for the September 2020 lumber future. Unlike the constant front-month, which now references November delivery futures, September lumber settled at $984.50 yesterday. The physical lumber market remains extremely tight, fueled by booming demand from construction, COVID’s impact on production eating into inventories, and now the forest fires in the West. Buyers who can wait a couple of months for delivery save 32% off the price of the current front-month contract; going out to next May that number is an impressive 48%; the futures market is pushing off construction into later quarters via price. Click here to start a free trial to Bespoke Institutional and receive our nightly Closer for the next two weeks, featuring more commentary and data on macro markets.

Gold and Bitcoin Bounce Off Support

With all the liquidity that has been put into the system, the number of Americans concerned about the dollar’s purchasing power has seen a great deal of inflation. Just last week, legendary investor Stanley Druckenmiller became the latest person to publicly worry about the possibility of double-digit inflation in the coming years. With those types of concerns becoming increasingly mainstream, it’s no wonder that the price of gold remains right near record highs. Despite the recent 5% pullback in prices, gold remains just under $2,000 per ounce after bouncing off support just above $1,900 which is a level that also coincides with its 50-day moving average. Since its high in early August, each bounce off the $1,900 level has been met with a lower high, so until this consolidation phase either breaks above $2,000 or below $1,900, it’s probably best to just sit tight.

Bitcoin has also been trading in somewhat of a consolidation pattern after breaking above resistance at $10,000 in late July. While bitcoin’s price rallied above $12,000 just as gold was peaking, its price pulled back in early September as risk assets corrected. However, just as $10,000 provided stiff resistance on the way up for the past year, the first test of $10,000 to the downside has held up so far. Investors increasingly view bitcoin as the digital version of gold, so by that logic, any bullish argument for gold should apply to bitcoin as well. Like what you see? Make sure to sign up for a free trial to unlock all of Bespoke’s analysis and interactive tools.

No New Highs For High Yield

The S&P 500 may have broken out above its February highs back in late August and still remains above February’s highs after today’s advance, but performance in the high yield market hasn’t been quite as strong. The chart below shows the B of A High Yield Master Index on a total return basis over the last 12 months. The index saw its peak back on 2/20 just a day after the S&P 500’s first-half high. Those gains quickly turned into a decline of nearly 20% before the markets started to recover. On September 2nd, just as the S&P 500 was getting off to a strong September start, the total return of the High Yield Master Index came just shy of topping its 2/20 high, but as markets started to swoon, the high yield market also suffered and prices pulled back.

While total return levels in the high yield market are important to track, spreads in high yield debt relative to treasuries provide a more useful barometer. In this respect, the high yield market has still come up short. The chart below compares spreads in the high yield market relative to treasuries over the last year. Remember, high yield spreads tend to move in the opposite direction as equities. When stocks rise, spreads tend to fall and vice versa. Back in January, high yield spreads bottomed out at 339 basis points (bps) nearly a full month before the S&P 500 peaked. They subsequently widened out to 1,087 bps on 3/23 which was the same day the S&P 500 bottomed. Since then, spreads have been more than cut in half to the current level of 521 bps. That’s an impressive move, but spreads are still nowhere near their prior lows. Like what you see? Make sure to sign up for a free trial to unlock all of Bespoke’s analysis and interactive tools.

Bespoke Brunch Reads: 9/13/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Pandemic Payoffs

Golf sees huge upswing with women and young adults: ‘You can take your bag full of White Claws’ by Melody Hahm (Yahoo! Finance)

Left for dead by shifting demographics and no taste for the links among younger folks, golf is suddenly getting a massive boon from COVID, with low disease risk and spare capacity for folks to head out and hit some balls. [Link; auto-playing video]

Locked Down in the Ritz-Carlton: Winning the Quarantine Hotel Lottery by Chong Koh Ping (WSJ)

Folks arriving in Singapore must pass a mandatory 14 day quarantine, but the hotel they spend their time at is assigned by lottery. For some, that lottery is a big payoff. [Link; paywall]

Battery Power

Pandemic e-commerce surge spurs race for ‘Tesla-like’ electric delivery vans by Nick Carey (Reuters)

In addition to targeting zero-emissions, last mile logistics companies are also looking for capabilities like autonomous driving and analytics which are already a part of basic Tesla capabilities. [Link]

Why Tesla’s Battery Day Will Actually Live Up to the Hype by Steve LeVine (Medium)

In a couple of weeks, Tesla will host a live webcast “battery day” alongside the company’s shareholders meeting; reading the tea leaves, it’s possible that CEO Elon Musk will announce its battery technology efficiency has improved to cost-parity with gasoline cars. [Link]

Alternative Approaches

To Manage Wildfire, California Looks To What Tribes Have Known All Along by Lauren Sommer (NPR)

Historically, Indigenous people around North America actively used wildfires as a way to manage the biosphere; returning to managed burns could reduce the scale and intensity of fires which have wracked California in recent summers. [Link]

Call police for a woman who is changing clothes in an alley? A new program in Denver sends mental health professionals instead. by Elise Schmelzer (The Denver Post)

A pilot program in Denver that focuses on mental health and social service intervention instead of police presence has led to a successful series of de-escalations rather than arrests and confrontation. [Link]

A $12 Billion Trust Fund Is About to Crack Open for U.K. Teens by Edward Robinson (Bloomberg)

15 years ago the Blair government created a trust fund that included government contributions, market gains, and family contributions to accounts. The first generation of recipients is set to start receiving the money this year, providing a firmer financial footing for all UK young adults. [Link]

Doomed Enterprises

Those boats in Texas paraded at the wrong speed by Brendan Greeley (FTAV)

You might think a boat parade would be a pretty straightforward enterprise, but the physics can get very complicated and very dangerous in a hurry, as was the case in Texas this week. [Link; registration required]

A Gender-Reveal Celebration Is Blamed for a Wildfire. It Isn’t the First Time. by Christina Morales and Allyson Waller (NYT)

A “smoke-generating pyrotechnic device” designed to spew the gender of a baby ignited a fire that consumed thousands of acres near Los Angeles, one of a number of similar incidents in recent years as the trend of over-the-top gender reveals and extreme wildfire conditions have coalesced. [Link; soft paywall]

Social Media

WeChat and TikTok Taking China Censorship Global, Study Says by Jamie Tarabay (Bloomberg)

Chinese social media apps used in the US often censor content deemed sensitive by the Chinese government, one among many reasons that Chinese tech is decoupling from the rest of the world. [Link; soft paywall]

Trading

NYSE Exchanges to Prepare for Potential Move From New Jersey by Stacie Sherman (Bloomberg)

In response to New Jersey’s discussion of a financial transaction tax, NYSE is preparing to move its digital infrastructure across state lines to dodge the tax. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

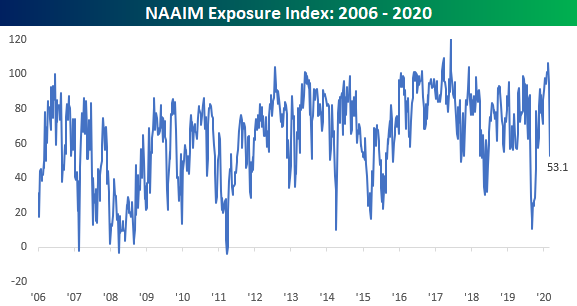

Active Managers Do an About Face

The National Association of Active Investment Managers (NAAIM) has an index which tracks the exposure of its members to US equity markets. Each week, members are asked to provide a number that represents their exposure to markets. A reading of -200 means they are leveraged short, -100 indicates fully short, 0 is neutral, 100% is fully invested, and 200% indicates leveraged long. Two weeks ago, in our Bespoke Report, we highlighted the fact that the exposure index had moved to one of the highest levels in its 15-year history. Now, just two weeks later, these same active managers have reigned in their exposure considerably as this week’s reading dropped from just under 100 to 53.1.

This week’s drop was the second-largest one week decline in the index’s history and just the 10th time that the index lost more than a third (33 points) in a single week. The most recent occurrence was back in early March in the middle of the Covid crash, and every other prior period where the index saw a similar drop, the S&P 500 was also down every time by an average of 2.3%. Therefore, it’s not much of a surprise to see the big drop this week given the big declines in the market. But what about going forward? Do big drops in the NAAIM Index mean a bounce back for markets or further declines? Find out in this weekend’s Bespoke Report newsletter where we cover this much more in depth. If you aren’t currently a client of any of Bespoke’s research services, make sure to sign up for a free trial today in order to unlock access to this week’s report.

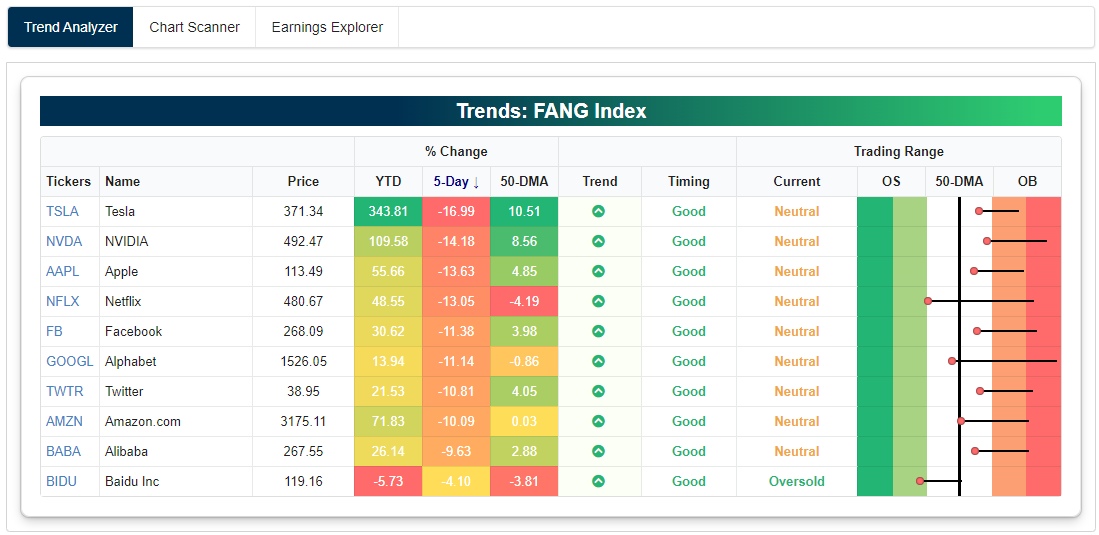

Mean Reversion Shows up in Trend Analyzer

Our popular Trend Analyzer tool is a very helpful way for Bespoke members to monitor overbought and oversold levels for large baskets of stocks or ETFs across asset classes. Below is a snapshot of major US index ETFs from our Trend Analyzer tool as of this morning.

When looking at the Trend Analyzer’s “Trading Range” section (far right of snapshot), the dot for each stock or ETF represents where its share price is currently trading relative to its 50-day moving average (DMA). In the snapshot below, the 50-DMA for each ticker is represented by the vertical black line in the middle of the trading range. Price is below the 50-DMA when it is to the left of the 50-DMA line and above the 50-DMA when it is to the right of the black line. Additionally, the tail for each ticker in the Trading Range section shows where the stock or ETF was relative to its range one week ago. So when the dot is to the left of the tail, it means price moved lower within its trading range over the last week. When the dot is to the right of the tail, it means price moved higher within its trading range over the last week.

Long tails mean price moved a lot over the last week on a relative basis, while short tails indicate little price movement. In today’s snapshot of US index ETFs, you can see that all of them have long tails with price moving lower over the last week. This highlights the significant downside mean reversion that US equities have experienced recently. In early September, pretty much everywhere you looked, prices were very overbought (extended well above their 50-day moving average). Over the last week or so, however, as equities have sold off they’re now trading at more neutral levels within their trading ranges.

When looking for an entry point or exit point on a position, it’s useful to take overbought or oversold levels into account. We use our “Timing” score within the Trend Analyzer to help members identify attractive (or unattractive) set ups. Members looking to add a new position or add to an existing position like to do so when price is trading at neutral or oversold levels as opposed to placing a bid when price is extremely overbought.

Looking at US sector ETFs, our Trend Analyzer shows that all of them have moved lower within their trading ranges over the past week, which gives them “Good” timing scores as opposed to the “Poor” timing scores these same ETFs had when they were trading at extreme overbought levels a few weeks ago.

The Energy sector (XLE) is the main outlier here with an extreme oversold reading. While every other sector is either neutral or overbought (Materials), Energy just can’t seem to get out of its own way this year. The sector entered today down 7.5% over the last week, 10.84% below its 50-day moving average, and down 43.7% year-to-date.

Finally, below is a snapshot of the stocks that make of the NYSE FANG+ index run through our Trend Analyzer. Similar to what we’ve seen around the rest of the US equity space recently, all of the FANG+ stocks are down significantly over the last week (8 of 10 down 10%+), and this has caused most of them to move out of overbought territory and back into neutral territory. For those that have been waiting for a pullback in these names to add exposure, now you’ve gotten it. Click here to start a free trial to Bespoke Premium and immediately gain access to our Trend Analyzer tool.

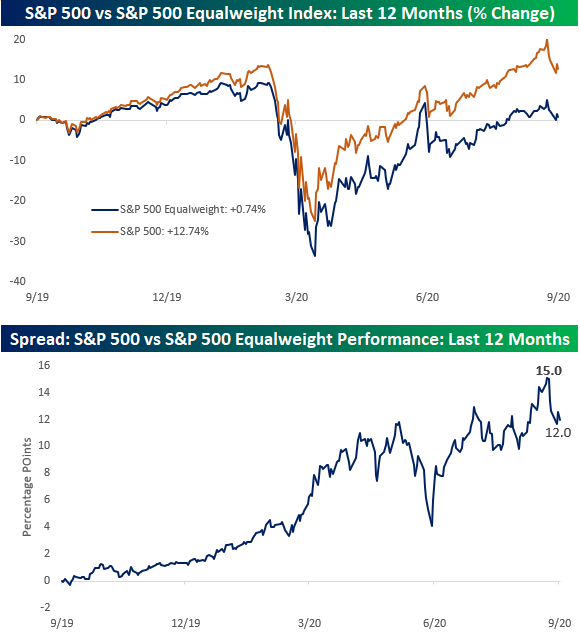

Gap Between Market Cap and Equalweight Shrinks a Bit

From the lows in March right up to now, one of the number one preoccupations of investors has been the widening gap between the market-cap-weighted S&P 500 and the equal-weighted index. When the market-cap-weighted index outperforms the equal-weight index, it indicates that stocks with the largest market caps are outperforming their relatively smaller peers and vice versa when the equal-weight index outperforms. As shown in the top chart below, through this afternoon, the S&P 500 has rallied more than 12.74% over the last year compared to a gain of just 0.74% for the equal-weight index for a gap of 12 percentage points.

The second chart below shows the performance spread between the S&P 500 and the equal-weighted index over the last 12 months. While the spread is wide now, just over a week ago it was even wider at 15 percentage points. The sell-off of the last few days has certainly narrowed the gap a bit, but there is still a lot of space between the two indices where they sit now. If the recovery from the pandemic recession continues, we would expect to see some broadening out of performance across market caps, but if the recovery derails or hits a roadblock, then the largest of the largest stocks could see their lead start to widen again. Click here to view Bespoke’s premium membership options for the best market analysis available.

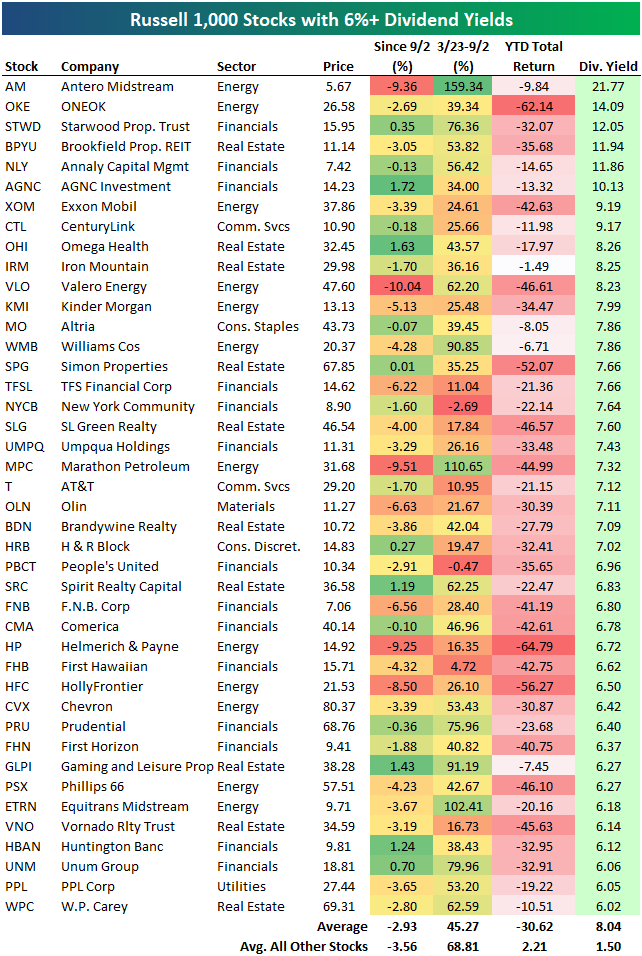

A Look at the Highest Dividend Yields in the Russell 1,000

There are currently 42 stocks in the Russell 1,000 that have dividend yields of more than 6%. These 42 stocks are listed in the table below. Given that every single one of these stocks is down on a year-to-date basis, and many are down 30-50%, the stability of these dividends is certainly in question. Many names on the list are from the beaten-down Energy sector. Antero Midstream (AM) has an indicated yield of 21.77% at the moment, followed by ONEOK (OKE) at 14%. Other Energy names on the list include Exxon Mobil (XOM) with its yield of 9.19%, Valero Energy (VLO) at 8.23%, and Marathon Petroleum (MPC) at 7.32%.

One of the only stocks on the list that’s not from the Energy, Financials, or Real Estate sectors is AT&T (T). AT&T is still down more than 20% year-to-date, and it has an indicated yield of 7.12%. Click here to view Bespoke’s premium membership options for our best research available.

The Most and Least Heavily Shorted Stocks in the Russell 1,000

Below is an updated look at the most heavily shorted stocks in the Russell 1,000. Each of these 30 stocks has at least 15% of its equity float sold short.

At the top of the list is Nordstrom (JWN) with 38.66% of its float sold short. With a YTD decline of 61.86%, the shorts have crushed it with JWN this year.

With its huge portfolio of office and retail real estate, Brookfield Property REIT(BPYU) has the second highest short interest in the Russell 1,000 at 33.7%. BPYU is down 35.7% YTD.

There are plenty of other well-known companies on the list of the most heavily shorted stocks. Examples include American Airlines (AAL), Virgin Galactic (SPCE), LendingTree (TREE), Wayfair (W), Dick’s Sporting Goods (DKS), ADT, TripAdvisor (TRIP), Beyond Meat (BYND), and Kohl’s (KSS).

One name that is no longer on the list of most shorted stocks is Tesla (TSLA). When we provided an update on short interest back in February (a pre-COVID world), Tesla (TSLA) had more than 17% of its float sold short, but that number is all the way down to 8.3% as of the most recent filing.

These 30 stocks with the highest short interest are down an average of 3.01% since last Wednesday (9/2) when the S&P 500 made its last closing high. That’s actually a little bit better than the 3.55% average decline for the rest of the stocks in the Russell 1,000. And year-to-date, these 30 stocks are up an average of 0.60% versus an average gain of 0.81% for the rest of the index. That’s not much of a difference!

Below is a list of the 30 least shorted stocks in the Russell 1,000 as a percentage of equity float. None of these stocks have more than 0.71% of their float sold short, and they’re mostly made up of more conservative names in the Health Care and Consumer Staples sectors.

Johnson & Johnson (JNJ) has the lowest short interest as a percentage of float in the Russell 1,000 at just 0.36%. Microsoft (MSFT) — one of the key mega-cap Tech names — has the second lowest short interest, followed by Merck (MRK), Eli Lilly (LLY), and Medtronic (MDT).

Somewhat surprisingly, Amazon (AMZN) is the sixth least shorted stock in the entire Russell 1,000. While AMZN is still thought of as a high-flying momentum name by many investors, its short interest levels tell a much different story, painting it as more of a non-cyclical stock like Pepsi (PEP), Procter & Gamble (PG), or Coca- Cola (KO).

While the 30 most heavily shorted stocks in the Russell 1,000 are up 0.60% YTD, the 30 least shorted stocks in the index are up much more at +8%. This group has MSFT, AMZN, HD, and AAPL to thank for that strong performance! Click here to view Bespoke’s premium membership options for our best research available.