Bespoke Brunch Reads: 11/21/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Finance

The hidden ‘replication crisis’ of finance by Robin Wigglesworth (FT)

One of the cornerstones of science (even social science, like academic finance) is replication or the idea that results can be repeated by future researchers; if something can’t be replicated, it’s probably not accurate. Finance has a major issue with these sorts of efforts. [Link; paywall]

Michael Mauboussin Is Unshaken by Eric Uhlfelder (RIAIntel)

An interview capturing the investment approach and experience of Michael Mauboussin, the legendary Columbia University professor and widely recognized strategist. [Link]

Retirement Fund Giant Calpers Votes to Use Leverage, More Alternative Assets by Heather Gillers (WSJ)

California’s pension giant (managing almost half a trillion dollars) sees below-typical historical returns that won’t be high enough to pay out on its obligations. The response from CalPERS is to add leverage to bring return targets back to their goal. [Link; paywall]

SARK launches as short interest in ARKK jumps to new record by Steve Johnson and Emma Boyde (FT)

In a first, an ETF has launched with the explicit goal of trading in the opposite direction of another ETF, specifically the ARKK vehicle which is the cornerstone of Cathie Wood’s ARK Invest empire. [Link; paywall]

Crypto

Tokenize Everything by Dave Nadig (ETF Trends)

Background on the rapidly expanding world of ERC-20 tokens, which are starting to look a lot like single stocks complete with vehicles for gaining index exposure to tokens (analogous to ETFs). [Link]

ConstitutionDAO — a $20 million stupid Ethereum trick by David Gerard and Andrew Molitor (David Gerard)

Decentralized Autonomous Organizations (DAOs) are an interesting approach to crowdfunding, charity work, or business structuring, but the highest-profile DAO so far descended into farce amidst a blaze of hype when it tried to buy a copy of the US Constitution. [Link]

Sustainability

Norway Is Running Out of Gas-Guzzling Cars to Tax by Morgan Meaker (Wired)

The vast majority of new cars sold in Norway are electric, which has created a >$2bn revenue problem for the country’s national government as the tax base of ICE vehicles craters. [Link; soft paywall]

Elon Musk Wants to Show Germans How to Build Cars by William Wilkes and Stefan Nicola (Bloomberg)

The German factory that will flood Europe with Teslas is taking a very different approach to traditional auto manufacturers, which could rapidly ramp up production with lower labor cost than traditional manufacturers are able to manage. [Link; soft paywall]

The Potentially Game-Changing Celera 500L Has Finished Its First Round Of Flight Tests by Joseph Trevithick (The Drive)

A new general aviation plane prototype is claiming to deliver operating costs 84% below what comparable private jets can manage, with fuel economy many times as high and more than twice the maximum range. [Link]

Streaming

How Much Does Mariah Carey Make When ‘All I Want for Christmas Is You’ Is Streamed? by Jermell Prigeon (NBC Philadelphia)

The fantastic popularity of Mariah Carey’s holiday anthem rises every year in a perfect seasonal pattern. Even at a penny per stream, the results are spectacular: almost $2mm per year in royalties accrue to the Christmas Queen. [Link]

Inflation

No, the real inflation rate isn’t 15 percent by Timothy B Lee (Full Stack Economics)

The CEO of Twitter has proudly amplified a statistical series that claims to adjust for changes in BLS methodology, but is itself founded on a complete misunderstanding which leads to a laughably incorrect representation of prices. [Link]

Hoops

Stephen Curry’s Scientific Quest for the Perfect Shot by Ben Cohen (WSJ)

Data science and optical sensors power Steph Curry’s offseason workouts, where anything more than three inches from dead center is considered a miss. [Link; paywall]

Modern Work

Ping. Ding. Chirp. Notifications Are Driving Us Crazy. by Rachel Feintzeig (WSJ)

Research suggests constant notifications are a huge factor in reducing productivity, regardless of the source. And between emails, Slack, and the cacophony of other alerts we receive, you can forget on deep and prolonged focus. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

COVID Trade Back in Full Swing

As we discussed in today’s Morning Lineup, the major headline of the day is the announcement of new lockdowns in Austria and other parts of Europe as case counts have risen sharply there recently. You can see the big spike in case counts in Europe in the chart below. We track a number of different Covid metrics in our daily Morning Lineup for Bespoke Premium subscribers.

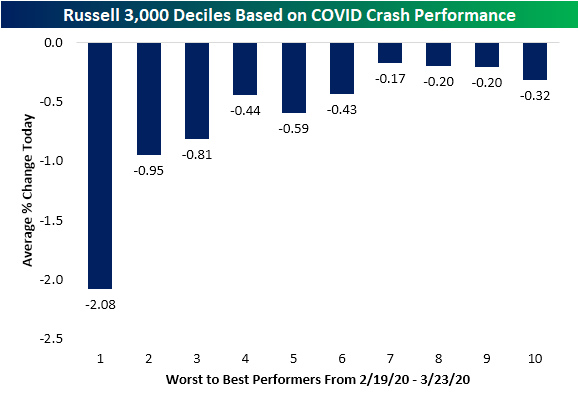

The news of rising case counts and potential lockdowns appears to have impacted stocks in a pretty big way today. In the chart below we broke the Russell 3,000 into deciles based on stock performance during the initial “COVID Crash” that occurred last year from 2/19/20 to 3/23/20. The first decile of stocks is comprised of those stocks that were hardest hit during the COVID Crash last year. As shown, this group of stocks is easily down the most today with an average decline of more than 2%. Moving across deciles, the stocks that held up better during the Covid Crash are also performing better today. That being said, every decile is in the red, but the first decile is the only one down by more than 1%.

Taking a look at industry groups, Energy, Retail, and Media and Entertainment stocks are the ones whose stocks are down the most on average today. Energy stocks are the worst of these with a 4.4% average decline. On the other hand, Household & Personal Products, Semis, and Utilities are the only industries whose stocks are in the green on average.

Given Energy is the weakest industry group, crude oil is also getting hit hard with a drop of 3.67% today. While crude oil began rolling over late last month, today’s drop marks the steepest one-day decline since July 19th. That leaves WTI futures at $76.11, which is the lowest price since the start of October. Crude is also back below its 50-DMA for the first time since September.

As for how that plays into prices at the pump, in the second chart below, we show the year-to-date change in the national average price for gasoline from AAA this year as well as on average from 2005 through 2020. As shown, historically Labor Day through the end of the year has typically marked the point in the year that prices experience a seasonal decline. This year, though, prices have rallied right through November and have only just now started to plateau. Click here to learn more about Bespoke’s premium subscription services.

BIG Charts of the Week – 11/19/21

You’ve likely seen Bespoke’s premium research before, but we continue to publish unique and timely analysis in reports like our Morning Lineup, BIG Tips, Sector Snapshot, Bespoke Baskets, Closer, and more.

Additionally, every Friday we publish our Bespoke Report newsletter — a detailed PDF that is easily digestible but super informative. You can see Bespoke’s current thoughts on global markets and the economy in this report.

If you’re not yet a Bespoke subscriber, you can gain access by simply starting a two-week trial to any of the three Bespoke membership levels listed below. You can revisit our membership options here.

Join Bespoke Newsletter (Weekly Bespoke Report + COTD; Lowest price)

Join Bespoke Premium (Newsletter research + Morning Lineup, BIG Tips, and more)

Join Bespoke Institutional (Access to everything!)

Below is a look at a handful of charts published this week that we thought were interesting or noteworthy. Additionally, we included a few quotes from Corporate America that we heard on earnings calls this week that have implications for the broader economy. Receive charts and analysis like this in your inbox daily by signing up for a two-week trial to Bespoke Premium.

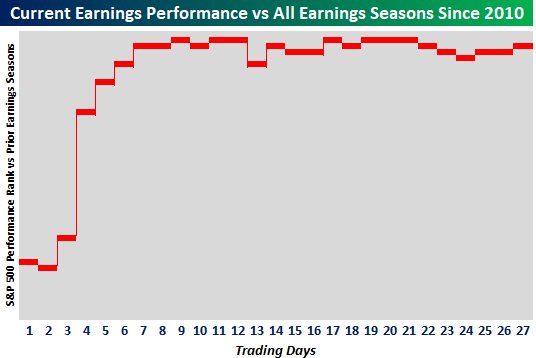

As earnings season unofficially ended this week, we took a look back at the S&P 500’s performance during the season. Despite the numerous headwinds supposedly facing the economy, earnings reports were generally strong this quarter, and the market reacted positively. As you can see, we significantly outperformed the average earnings season performance since 2010.

Although performance has been strong as of late, bullish sentiment pulled back to normal levels this week. Bullish sentiment from the weekly AAII sentiment reading pulled back by 9.2 percentage points, which is the largest week over week decline since September 16th. However, the reading of 38.8% is within one percentage point of the historical average.

Typically, consumer sentiment and quit rates tend to be correlated, as employees feel more comfortable quitting when they are confident in the economy. However, there has been a divergence between these two readings recently. This may be in part due to the labor shortage experienced by the economy, and although consumers have a reduced sentiment, employees still feel like they can easily find another job.

COVID cases have ticked up recently in North America and Europe. In today’s Morning Lineup, we discussed the lockdowns being initiated by regions within countries like Austria and Germany. The last thing our supply-ridden economy needs is lockdowns, so this will be an important development to watch moving forward.

Rivian (RIVN) IPO’d recently and caught the eyes of many investors. Remarkably, it took Tesla 2,407 trading days to reach a $100 billion market cap versus just 3 trading days for Rivian. Although the cause of this is uncertain, it appears as if investors do not want to miss the next Tesla and are willing to pay up massively for exposure to EV producers.

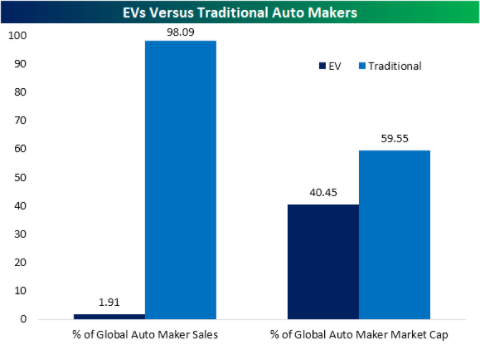

Although traditional auto manufacturers currently sell over 98% of vehicles globally, EV companies now make up more than 40% of global automaker market cap! This separation between revenue and market cap may point to the general froth in the market, and leaves some investors concerned about current valuations on a broad basis.

Throughout this earnings season, we have been reporting on and summarizing select conference calls for our Bespoke Institutional subscribers. Here are some of the notable quotes from this week’s calls with implications for the broader economy:

NVIDIA CFO Colette Kress stated, “Last week, we announced general availability of Omniverse Enterprise, a platform for simulating physically accurate 3D world and digital twins. Initial market reception to Omniverse has been incredible.”

Target CEO Brian Cornell commented, “We don’t expect those supply chain challenges that go away as we go into the start of next year… I think they will dissipate overtime…we know that we’re going to still face some supply chain challenges as we go into 2022.”

Home Depot COO Ted Baker added, “We are also seeing rising cost pressures across several different product categories.”

Walmart CFO Brett Biggs commented, “Despite the various macro and industry challenges, our inventory position is good. Stores and fulfillment centers are well staffed and our price position remains strong.”

Tyson Foods CEO Donnie King stated, “Labor has been very challenging throughout the year, but as we’ve mentioned in the script earlier, we are seeing a light at the end of this tunnel, we’re seeing our ability to get plant staff… we are almost fully staffed since November 1st.”

To see the summaries of the earnings reports we covered, you can login if you’re a member or start a two-week Bespoke Institutional trial.

In addition to this earnings coverage, you will also have access to our recently debuted Little Known Stocks (LIKS) report as an Institutional subscriber. On Wednesday, we published our fourth LIKS report.

In these reports, we provide an in-depth breakdown of a stock that likely remains under the radar of most investors. In this week’s report, we analyzed a company that operates in a space that has been experiencing massive growth with no signs of slowing down. Through 2025, this industry is expected to grow at a whopping 68% per year, and this company has grown its revenue at a rate of 24% per year over the last four years. Again, you can start a two-week trial to Bespoke Institutional to see this LIKS report and others.

That’s it for this week. Have a great weekend and we’ll be back at it on Monday!

Bespoke’s Morning Lineup – 11/19/21 – Lockdowns Make a Comeback

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Failure is simply the opportunity to begin again, this time more intelligently.” – Henry Ford

After the near-complete shutdown last year and the gradual re-opening of the economy in fits and starts around the world since then, most people probably thought we would never return to the days of lockdowns again, but Austria and other parts of Europe are changing that mindset this morning. In Austria, two regions of the country are locking down beginning on Monday by closing non-essential businesses and schools for a month. Whether these lockdowns extend to the entire country remains to be seen. Outside of Austria, parts of Germany have also announced that bars and restaurants will be temporarily closed in an effort to halt the spread. With case counts rising in other parts of Europe as well, a spread of these restrictions to other parts of Europe can’t be ruled out.

Not surprisingly, the new restrictions on activity being placed in Europe have put pressure modest pressure on equities in the region and here in the US this morning while treasury yields decline and crude oil is down sharply falling to its lowest level since October 1st. The weakness in equities this morning isn’t all one-sided, though. Re-opening stocks are under pretty significant pressure and the Russell 2000 is down over 1%, while ‘work from home stocks’ have been catching a bid with the Nasdaq indicated to open higher.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The charts below are what have government officials in Europe and investors around the world on edge. Starting with Germany but spreading to other countries, COVID case numbers across major European economies have been surging in recent weeks. As shown in the chart at left, case numbers in Europe as a whole have been surging and are now well back above levels (per million people) in the US (where case levels have also started a new leg higher). Within the European continent (right chart), Germany has been leading the way higher in terms of total new case counts which are actually at a new high for that country, but if you look a little closer at the chart, you can also see that case numbers in France, Italy, Spain, and Sweden have also started to trend higher.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Sentiment Back to Average

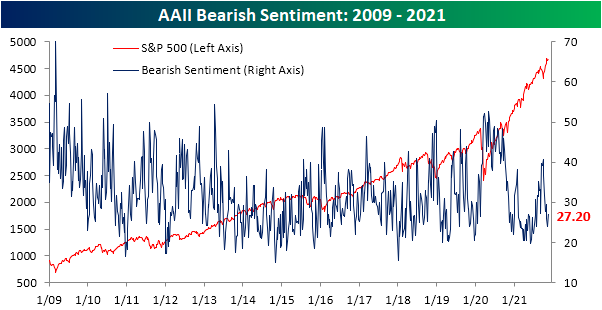

The past week has seen the S&P 500 hover right below but not at record highs. The lack of new highs in price appears to have left individual investors apprehensive as bullish sentiment in the AAII survey pulled back 9.2 percentage points to 38.8%. That was the biggest one-week drop since a 16.5 percentage point decline in the week of September 16th, though back then, bullish sentiment sat much lower at 22.4%. At the current level, bullish sentiment is still within one percentage point of the historical average.

While bullish sentiment saw a sharp reversal lower, bearish sentiment rose modestly to 27.2%. That is the highest level since the end of October and that remains roughly 3 percentage points below the historical average.

Those inverse moves resulted in the bull-bear spread falling to 11.6. While lower, that still indicates overall sentiment favors optimists.

A greater share of the losses to bullish sentiment shifted to the neutral camp with around a third of respondents reporting as such. That is the highest level since the first week of October. That reading is a few percentage points above the historical average meaning that like bullish and bearish sentiment, current survey readings do not indicate sentiment is elevated or depressed to any sort of notable extent. Click here to view Bespoke’s premium membership options.

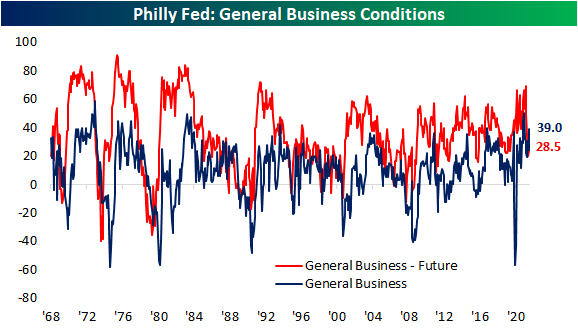

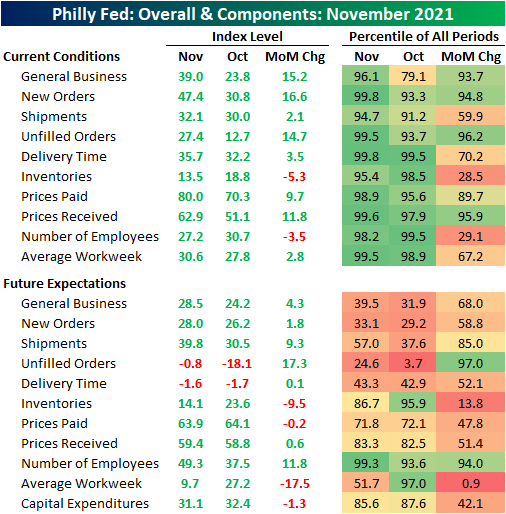

Demand Surges in Philly

There were two regional Fed bank manufacturing survey results for the month of November released this morning. The first and stronger of these was out of the Philly Fed. Like the neighboring Empire Fed reading out earlier this week, the Philadelphia Fed’s survey showed an acceleration in activity this month that exceeded expectations. The index for General Business Conditions rose 15.2 points to 39.0 versus a more modest expected increase to only 24. That brings the index from a 79th percentile reading last month to a 96th percentile reading which is the strongest since April’s near-record level.

Not only was there a big increase in the headline number, but many of the other categories also saw significant increases this month including new orders, unfilled orders, and prices received which all saw month over month gains that rank in the roughly top 5% of each index’s respective history. Overall, the report showed continued growth in the region’s manufacturing economy with almost every category accelerating MoM in November.

Demand saw massive improvement this month as the index for New Orders leaped higher by 16.6 points to 47.4. That leaves the index at the second strongest level on record behind March 1973. Shipments also rose but the increase was far more modest relative to gains for demand. As a result, Unfilled Orders are also surging. That index came in at the fourth-highest level to date with the only higher readings occurring in May of this year and January and March of 1973.

It isn’t a new story, but one headwind in spite of—or perhaps even partially because of—that strong demand is supply chain issues. Higher readings in the Delivery Times index imply that products take longer to reach their destination. As with other reports, this index has been coming in at unprecedentedly high levels for several months now, but the Philly Fed differs in that this summer saw a big reversal lower. The increase this fall has now given up most of those improvements. Additionally, expectations are fairly optimistic with two months of negative readings in a row.

One other impressive aspect of the surge in demand is it comes as prices were hiked at a historic rate. The Prices Received index rose to 62.9 which is the third-highest reading on record. The only months with higher readings were February and June 1974. Prices Paid also rose month over month, but that index came up short of a new high. Click here to view Bespoke’s premium membership options.

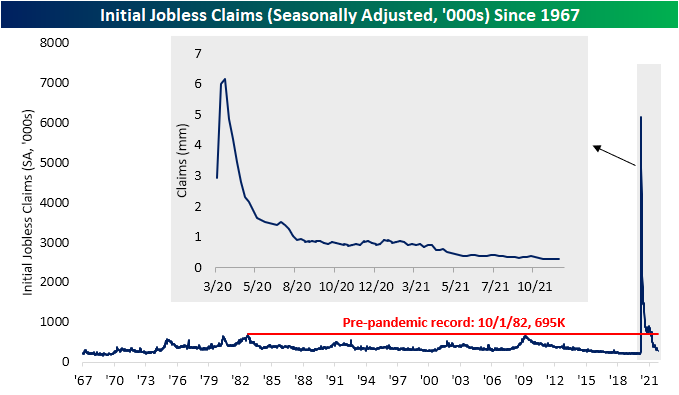

New Lows And Oddities for Jobless Claims

Jobless claims were slightly weaker in the most recent data released this morning. Expectations were calling for a drop to 260K, but instead claims only fell to 268K from last week’s 2K upwardly revised reading of 269K. Given that revision, claims have now fallen for seven weeks in a row with new lows for the pandemic. Initial claims are also now only 12K above the pre-pandemic reading of 256K from March 13, 2020; the last week before claims began to print in the millions.

On a non-seasonally adjusted basis, that pre-pandemic low was finally taken out this week. Unadjusted claims totaled 238.9K from 257K last week. That is the lowest level since the first week of March 2020 when claims were a hair below 200K. With the program’s expiration now even further in the rearview, PUA claims continue to have a minimal impact of only 1,390.

From a seasonal perspective, 2021—particularly this fall—has been an interesting year. For starters, claims have more or less returned to historically normal levels even when factoring in auxiliary programs. Furthermore, from Labor Day through the end of the year has historically marked a period of the year that claims have had a tendency to rise, but this year the opposite has been the case. In the context of that bucked seasonal trend, the current week of the year (46th) actually has a seasonal tailwind with claims rising week over week only 16.67% of the time since 1967. In other words, this week’s drop could be expected but the new low it resulted in is thanks to seasonally unusual declines in weeks leading up to now.

Lagged one week to initial claims, continuing claims were the better part of the claims release. Continuing claims fell to 2.08 million versus expectations of a decline to 2.12 million from last week’s reading of 2.16 million. As with initial claims, that resulted in the strongest level for claims since March of last year when the reading sat below 2 million.

Using the non-seasonally adjusted data and including all other programs adds one more week of lag to the data making the most recent reading through the last week of October. The end of last month saw an uptick in claims across programs with the biggest contributor being PUA claims which rose by over half a million. At 791.1K, PUA claims were at the highest reading since the week of September 10th; right after pandemic programs expired.

While an uptick in PUA claims sounds puzzling given the program is expired nationally, delving deeper into the data shows the US uptick is all thanks to one state: California. As shown below, California has continuously made up for a large share of national PUA continuing claims since the start of the program. While the state has seen a substantial drop like the rest of the country this fall, this week’s rise leads California’s claims counts from this program to be a multiple larger than the 52 other states and territories combined. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 11/18/21 – Philly Fed Jumps

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Trying to sell short in this market is like being run over by a train that’s going to derail a mile down the road.” – Julian Robertson

We may be at the tail end of earnings season, but it’s not going out quietly as we’re seeing some significant earnings-related moves this morning. On the downside, both Cisco (CSCO) and Alibaba (BABA) are down over 6% as they both missed sales estimates and lowered guidance. On the upside, even after the run it has had into earnings, Nvidia (NVDA) is up over 8%. In the retail space, a number of stocks including Victoria’s Secret (VSCO), Kohl’s (KSS), and Macy’s (M) are all up by at least 7%.

Today is also a fairly busy one for economic data as well with Jobless Claims and the Philly Fed at 8:30 and then Leading Indicators at 10 AM. Then, at 11 AM we’ll close out the week’s economic calendar (there are no reports scheduled for tomorrow) with the KC Fed r manufacturing report. Jobless Claims were pretty much right inline with expectations coming in at a post-COVID low of 268K while continuing claims were much lower than expected at 2.08 million. The Philly Fed report also came in better than expected coming in at a level of 39.0 which was the best reading since April.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Relative to last Wednesday’s close, major US equity averages have generally had a positive bias but have seen little in the way of moves in either direction. As shown in our Trend Analyzer snapshot of US index ETFs, the only one that has moved up or down 1% during this period is the Micro-Cap index (IWC) with a decline of 1.17%. Despite the decline, though, IWC remains at overbought levels and is still one of the top-performing ETFs YTD. Behind IWC, the next worst performing index ETF in our snapshot is IWM which is down 0.9% over the last week. Like IWC and every other index ETF listed below, IWM remains at overbought levels, so it’s not as though these moves have been significant.

With small caps and large caps at two different ends of the performance spectrum this week, we wanted to highlight each index’s price chart to show how the moves look from a longer-term perspective. IWM has seen a pretty swift reversal in the last week, but it also follows a short-term move that was much steeper to the upside. Large caps like SPY, on the other hand, saw more gradual (relatively) increases leading up to their recent highs and remain right near all-time highs with the S&P 500 actually coming up just short of a record closing high on Tuesday.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

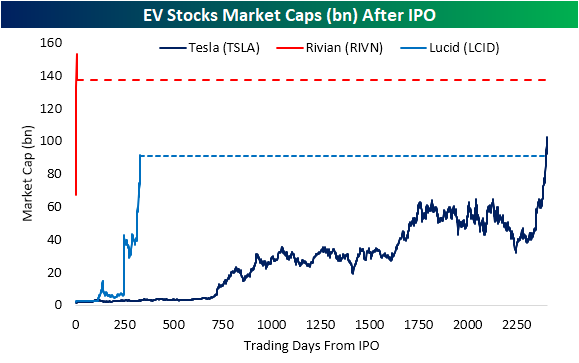

EV Market Caps Disregarding Sales

The newest EV IPO — Rivian (RIVN) — was down 15% today, but it still has a market cap of $125 billion, and it took only three trading days for the stock to close with a market cap of more than $100 billion.

Remember in the mid-2010s when Tesla (TSLA) bears complained about the company’s multi-billion dollar market cap even though it hardly had any revenues? Well, the action in the EV space lately makes those prior Tesla complaints look laughable.

With Rivian (RIVN) now worth over $100 billion after just a few trading days and Tesla competitor Lucid (LCID) worth more than $80 billion, we wanted to highlight how long it took Tesla (TSLA) to trade at a similar market cap. As shown below, it wasn’t until January 13, 2020 that TSLA’s market cap first crossed above Lucid’s current market cap, and TSLA didn’t cross above Rivian’s (RIVN) market cap until February 2nd, 2020. While it took Tesla 2,407 trading days from its IPO to hit $100 billion in market cap, it only took three trading days for RIVN to do the same.

When Tesla first reached $100 billion in market cap in January 2020, the company had reported revenues of $7.4 billion in the most recent quarter. RIVN and LCID, on the other hand, are still considered “pre-revenue” companies!

The rise of the electric vehicle is an overarching trend that consistently finds its way into the headlines. As shown below, Google Trends scores for terms like “Electric Car” and “EV” are approaching record highs and have more generally been grinding higher over the past few years with particular acceleration in 2020 and beyond.

The past couple of months has seen plenty of EV stock headlines ranging from the surge in Tesla (TSLA) as it eclipsed a $1 trillion market cap and the strong IPO of Rivian (RIVN). As a result of the strong performance of these stocks, looking at the largest global automobile manufacturers by market cap, EV names now have a significant presence. In fact, of a universe of 118 global auto stocks with market caps of at least $100 million (USD adjusted), 42% of the combined market cap is made up of four EV names—Tesla (TSLA), NIO (NIO), Lucid (LICD), and Rivian (RIVN). TSLA is of course the bulk of this with nearly a third of that total share, but Rivian (RIVN) is also high up on the list ranking as the third-largest of any single auto stock, and that is only after trading for a few days!

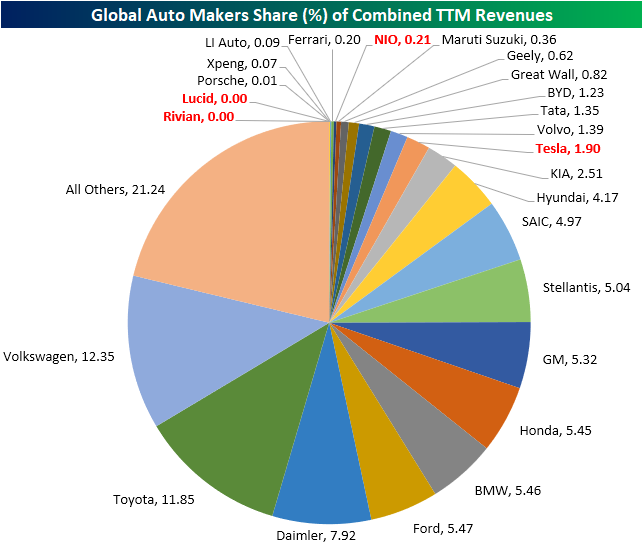

With that said, those valuations are pretty extreme when compared to sales (again USD adjusted). In the chart below, we show the same stocks but as their share of the group’s trailing 12-month revenues. As shown, the most legacy company of the EVs, TSLA, only made up for 1.9% of the industry’s revenues. NIO is the only other one with any sales to speak of.

Obviously, there is a major disconnect between these stocks’ sales figures over the past year and their market caps. Traditional automakers are bringing in far higher revenues than EV’s which for whatever reasons (rational or not) are not being reflected in market caps. Click here to view Bespoke’s premium membership options.

Stocks Most Impacted by 7-10 Year Treasuries

Since the beginning of the pandemic, investors have consistently discussed the relationship between treasury yields and the performance of equities. Of course, every company is different, and there are some companies that benefit from higher Treasury yields while others outperform when rates decline.

The table below summarizes the S&P 500 members that perform best when the iShares 7-10 Year Treasury Bonds ETF (IEF) loses value. We measure this by calculating the correlation coefficient of individual stock prices against the price of IEF since the start of 2020. In other words, when rates increase (IEF price declines), these stocks experience positive price movement. M&T Bank (MTB), American Airlines (AAL), and Hewlett Packard (HPE) top this list, and all the names on this list have high correlation coefficients implying that they are closely tied to the performance of IEF on an inverse basis. Other notable names on this list include Ralph Lauren (RL), Citigroup (C), Fox Corp (FOX), and Tyson Foods (TSN). Of the 20 companies on this list, six come out of the Industrials sector and 5 are from the Financials sector. The average YTD performance of the names on this list through 11/15 was a gain of 31.1% (median: +25.2%).

To help you visualize exactly what we are looking at, take a look at the chart below. MTB is the stock most inversely correlated to IEF. Since 2020, it has routinely moved in the opposite direction as IEF. When IEF moves up, MTB tends to decline, and vice-versa. If you believe that treasury yields will rise, MTB and the other names on the list are ones that have historically benefitted in that environment.

The next table shows the S&P 500 stocks that have benefitted during periods of falling yields, which would be represented by an upward move in the price of IEF. The stocks on this list are generally less correlated to the movements of IEF, so the correlation coefficients are less statistically significant. The average returns for the stocks on this list on a YTD basis is a decline of 1.9% (median: -2.1%) through 11/15. Clorox (CLX), Vertex (VRTX), and Incyte (INCY) have the highest correlation coefficients to IEF, and other notable names include Regeneron (REGN), MarketAxess (MKTX), and General Mills (GIS). 7 of the 20 companies on this list are from the Consumer Staples sector, 4 are in the Health Care sector, and 3 are in the Real Estate sector.

As you can see, the price movements between CLX and IEF have been quite similar since the start of 2020. While prices of CLX and IEF have been well correlated since the start of 2020, we would note that outside of the first five stocks on the list, none of the other names listed have a correlation coefficient of more than 0.5 indicating that the relationships are not nearly as strong as the names on the first list above. In terms of both lists, the correlation coefficients are simply telling us how each stock has traded with respect to IEF since the start of 2020, but whether those relationships hold up going forward is uncertain, Click here to view Bespoke’s premium membership options.