Bespoke’s Morning Lineup – 12/7/21 – Strong Start With Nasdaq in the Lead

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I would say that financial markets are very inefficient, and capable of extremes of being completely dysfunctional.” – Jeremy Grantham

Forget about a ‘turnaround’ for now, this Tuesday is looking more like a terrific one as US futures, led by the Nasdaq, are sharply higher following through on Monday’s rally. The opening bell hasn’t even rung yet, though, so there’s plenty of time left in the day. That said, early indications are pointing higher with risk assets all trading higher, although long-term Treasury yields are moving much less higher than you would expect given the move in equity futures. Crypto assets are also in rally mode this morning as bitcoin is back above $50K, and ether is back above its 50-day moving average.

In economic data, the revision to Non-Farm Productivity was lower than expected (-5.2% vs -4.7%) while Unit Labor Costs increased more than expected (9.6% vs 8.3%).

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The Russell is indicated to open more than 1.5% higher this morning continuing what has been a volatile run for the small-cap benchmark index. So far during this sell-off from a false breakout, IWM has managed to stay within its prior trading range after falling below both its 50 and 200-day moving averages. In addition to the consistency of much higher than average volume during the last seven trading days, IWM has also had an intraday trading range of more than 2% and averaging more than 3.3% during that span. The last time IWM experienced a run of 2%+ intraday ranges for seven consecutive trading days was back in July 2020.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

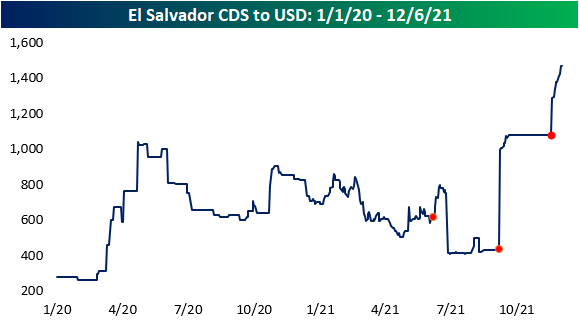

El Salvador Hurt By Bitcoin

On 6/5, El Salvador passed a bill that made Bitcoin legal tender in the nation effective 9/17. Since passing the bill, the country hosted a Bitcoin Week, which generated excitement from the crypto community in which he and political/industry leaders spoke about the logistics and benefits of legalizing Bitcoin as a legal tender. During Bitcoin week, El Salvador’s leadership unveiled its plans for ‘Bitcoin City’, which will be funded by issuing a $1 billion Bitcoin Bond. The city (and the Bitcoin mining inside of it) will be powered by geothermal power generated from a nearby Volcano.

Over the weekend, El Salvador’s President, Nayib Bukele took to Twitter, stating that “El Salvador bought the dip” and added that he trades cryptocurrency for his country through his phone. Although Bitcoin enthusiasts view this adoption as revolutionary, the investing community has taken a different view. Since the country officially announced that Bitcoin would become legal tender, its bonds have declined in value. As one example, the price of the country’s 7.65% bonds maturing in June 2035 has plummeted by 37.5%. Investors are wary of the idea of tying a country’s assets and balance of payments to an extremely volatile asset, and that has caused the yield on the bond shown below to rise nearly over 600 bps from under 8% to over 14% now.

The cost of insuring against default for El Salvador’s debt (credit default swaps) has risen significantly since the nation legalized Bitcoin as legal tender, and CDS spreads have more than doubled over the period. Will this dissuade other countries from using cryptocurrencies as legal tender? Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 12/6/21 – Nasdaq Lags

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I would say that financial markets are very inefficient, and capable of extremes of being completely dysfunctional.” – Jeremy Grantham

US equity futures are tentatively higher this morning with leadership in the Dow while the Nasdaq continues to lag. The economic calendar is empty today, but investors already have an eye out for Friday’s CPI report. Omicron continues to be a concern, and while there’s still a lot more we don’t know than we do know about the latest strain, reports continue to suggest that despite the higher transmissibility, its impact has not been nearly as harsh. In the crypto space, bitcoin has been relatively stable since Sunday following a sharp decline Friday night into Saturday morning.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

While companies valued at high multiples to revenues have been hit hard since the emergence of the omicron variant and the FOMC’s hawkish pivot just after Thanksgiving, there’s been a decent amount of disparity in performance among international markets with developed markets falling in the last week while emerging markets actually eked out gains. As shown below in the snapshot of international regional ETFs from our Trend Analyzer, the worst-performing ETF of the group was the MSCI All Country World (ACWI) which fell just over 1%. Moving down the list, at the bottom, the lone ETFs that were positive on the week were related to Emerging Markets. US equities were also a drag on performance last week. While the ACWI was down just over 1%, CWI, which is the MSCI All Country World ex-US Index was only down -0.07% on the week.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 12/5/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Crime

A Michigan woman tried to hire an assassin online at RentAHitman.com. Now, she’s going to prison. by Jonathan Edwards (WaPo)

A website run by a North Carolina man has served as a honeypot for those with murderous intentions for over a decade, with a Michigan woman angry at her ex-husband the latest would-be killer to be ensnared by law enforcement after requesting information from the site. [Link; soft paywall]

Hiding in plain sight: How one of the country’s most-wanted fugitives led a quiet life in Lynnfield by Emily Sweeney (Boston Globe)

A 1969 bank robbery was never solved after a teller walked out with the equivalent of $1.6mm in today’s dollars, slipping into obscurity as a resident of a Boston suburb. [Link; soft paywall]

Metaverse Madness

A plot of virtual land that went for $4.3 million in The Sandbox is the most expensive metaverse property sale ever by Carla Mozée (Business Insider)

Republic Realm, a firm focused on the purchase and development of digital real estate and assets, purchased space in the Sandbox metaverse for $4.3mm this week. We wish we knew what that meant, exactly. [Link]

Metaverse Real Estate Piles Up Record Sales in Sandbox and Other Virtual Realms by Konrad Putzier (WSJ)

This explainer on the process of digital land sales offers some further explanation as to what exactly is going on with the process, but we still have many questions, not least of which being how the supply of land is constrained. [Link; paywall]

Macy’s Turns Thanksgiving Day Parade Balloons Into NFTs by Joseph Pisani (WSJ)

Just about everything is being turned into an NFT these days, with the iconic balloons floating above Manhattan the latest unique items being assigned an arbitrary value and slapped on the blockchain. [Link; paywall]

History

America’s First Banned Book Really Ticked Off the Plymouth Puritans by Matthew Taub (Atlas Obscura/Pocket)

One of the country’s first banned books was a jeremiad against the leadership of Puritan New England’s early colonial management. The 1637 tome wasn’t the only thing its author did to enrage the other colonists. [Link]

Autos

Ford teases a new cable capable of charging electric cars in 5 minutes by Mark Wilson (Fast Company)

Ford (F) is researching a new cable that would allow a massive dump of electricity into a vehicle battery and turn a charging stop into the same layover time as a gas station visit in an ICE vehicle. [Link]

Auto chip shortage shows new sign of easing as inventories rise by Ryosuke Eguchi (Nikkei Asia)

Semiconductors which find their way into new cars are finally becoming easier to lay hands on as major suppliers reported higher inventories for the first time in at least 9 months during the month of September. [Link]

Extreme Biology

Microsoft Makes Breakthrough in the Quest to Use DNA as Data Storage by Phillip Tracy (Gizmodo)

DNA is a remarkably dense storage medium, with every movie ever made able to fit in a volume the size of a sugar cube. It’ll be some time before DNA-based memory storage is viable commercially but researchers are getting closer to that holy grail of cheap data warehousing. [Link]

World’s vast networks of underground fungi to be mapped for first time by Fiona Harvey (The Guardian)

Huge networks of underground plants in the same family as mushrooms are a critical support for biological systems like forests. A new initiative seeks to understand and map the networks around the world. [Link]

Labor Markets

The US is facing an unlikely shortage: Santas. by Sarah Al-Arshani (Business Insider)

Lots of people are looking for Santa, with inquiries to hiresanta.com surging 121% this year compared to the last two years. At the same time, many Santas are retiring, and others are worried about the pandemic; still more have passed away thanks to COVID. [Link]

North Carolina’s Furniture Hub Is Booming. What Comes Next? by Jeanna Smialek (NYT)

The surge in demand for furniture fueled by the pandemic is proving a temporary boon for furniture makers in North Carolina, but factories fear orders will drop off and as a result are hesitant to ramp up hiring and capacity expansion. [Link]

Numbers

Today’s date is rare: It reads the same way forward, backward and upside down by Jay Cannon (USAToday)

Not only was the 2nd of December a palindrome, reading the date also reads the same upside down. Another such palindrome date is due until March 2nd of 2030. [Link]

Mining Bitcoin with pencil and paper: 0.67 hashes per day by Ken Shirriff (Righto)

There is some very complicated math underpinning cryptocurrencies like Bitcoin, but that doesn’t mean it can’t still be done by hand. [Link]

Easy Marks

Notable Bets: November among worst months ever for betting public by David Purdum (ESPN)

Amidst an explosion of gambling legalization and betting apps, 60% of November NFL games had seen underdogs cover the spread, leading to a historic route among bettors. [Link]

Stock Funds Took in More Cash in 2021 Than Two Decades Combined by Ksenia Glouchko (Bloomberg)

Nearly $1trn has followed into ETF and mutual funds this year, more than each of the last 19 years…combined! [Link; soft paywall]

COVID

Do childhood colds help the body respond to COVID? by Rachel Brazil (Nature)

Children who are exposed to a given strain of flu are better at fighting that strain off the rest of their lives. It’s an open question whether the same process will play out with COVID. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Stocks Down 2%+ Every Day This Week

This week was particularly volatile for the stock market with the S&P 500 seeing 1%+ moves every trading day from Monday through Thursday and then a decline of close to 1% on Friday. We came across Etsy (ETSY) on Friday when it was down 7% on the day, and then we noticed that the stock had been down 2% or more on every trading day this week. In wondering how many other stocks were down 2%+ every day this week, we found a total of 12, and they’re all listed below. Along with Etsy, the other notable losers include Affirm (AFRM), Oatly (OTLY), and Clear Secure (YOU). Affirm’s worst day was Wednesday when it fell 8%, but it fell another 5.7% on Friday to close the week down 21.7%. Oatly began the week down 3.7% on Monday and down 3.9% Tuesday before falling 6.1% on Wednesday. Smaller declines of 2% on Thursday and 2.8% on Friday left OTLY only down 17.3% for the week. That’s relatively good compared to Kirkland’s (KIRK), which fell 39.1% on the week after losing a quarter of its value on Thursday and then another 8.5% on Friday.

Small-Cap Corrections

At the close on Wednesday (12/1), the small-cap Russell 2,000 had fallen 12.1% from its recent high on November 8th, leaving the index in “correction” territory. A market “correction” is a drop of 10%+ that was preceded by a rally of at least 10% on a closing basis. This correction for the Russell 2,000 is its 58th since data for the index begins in 1978. Below is a table showing prior corrections for the Russell. The average correction sees the index fall 18.35%, which is just shy of the 20% threshold for a “bear market.” The median correction is a little smaller at -15.4%. In terms of length, the average Russell correction has lasted 73 days, while the median is 62 days. For the current Russell 2,000 correction to reach average levels, it would need to fall another 7% from here, and it would come to an end on January 20th, 2022.

In terms of extremes, the biggest correction that the Russell 2,000 has ever experienced was the 41.9% decline seen during the initial COVID Crash from 1/16/20 to 3/18/20. The longest correction lasted 397 days from 6/24/83 to 7/25/84. In terms of the shortest correction, there were two that lasted 3 days. One of those came during the Financial Crisis while the other happened last June. Like this type of analysis? See more of it with a Bespoke Premium membership. Click here to learn more and start a two-week trial.

Bespoke’s Morning Lineup – 12/3/21 – A Day of Rest?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Never confuse genius with a bull market.” – Unknown

After five days where the S&P 500 has moved up or down 1%, futures are practically flat this morning as the market tries to catch its breath from all the volatility. The quiet tone may not last long, though, as Non-Farm Payrolls was just released and came in much weaker than expected at just 210K compared to estimates for a gain well in excess of 500K. Despite the weak print, the unemployment rate was much less than expected (4.2% vs 4.5%). In terms of average hourly earnings, month/month growth was 0.3% vs 0.4%. In addition to the jobs data, we’ll be getting ISM Services, Factory Orders, and Durable Goods all at 10 AM. The initial reaction to the jobs number has been slightly positive with Nasdaq futures leading the way.

Last night, the state of New York announced five additional COVID cases related to the omicron variant, and Hawaii announced one case. At this point, all the cases appear to be mild which is encouraging. In South Africa, where the variant was first detected, the number of cases has tripled within the last three days, but thankfully, hospitalizations are not rising nearly as fast. Barely a week after the omicron variant first made headlines, there’s still a lot we don’t know about this variant, but based on data so far, it doesn’t appear to be any worse than other strains.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s been quite a week in the markets, so investors probably deserve a quiet day for a change. Check out the carnage that we’ve seen in US stocks since Thanksgiving when news of the Omicron variant first surfaced and then Powell’s hawkish pivot this week. Every major US index ET we track in our Trend Analyzer is down more than 2%, while small caps are down more than twice that. Market cap has really been a factor in market performance this week as the Micro-Cap ETF (IWC) is down close to 6% while mega-cap indices like the Nasdaq 100 (QQQ) and S&P 100 (OEF) are both down less than 2.5%.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Consumer Pulse Report – December 2021

Sentiment Collapse

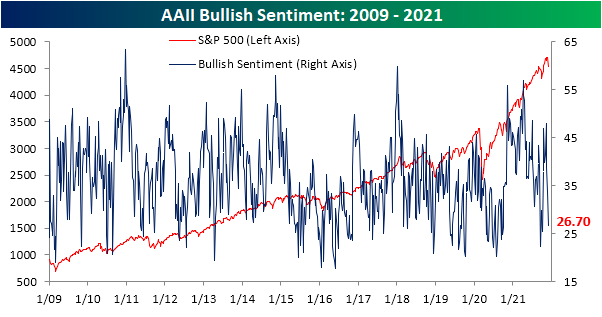

In the past three weeks, sentiment has taken a big hit with the percentage of respondents to the AAII survey reporting as bullish falling 21.3 percentage points. That is the biggest three-week decline since March 2018 when bullish sentiment fell a slightly larger 22.12 percentage points. With 26.7% of respondents bullish, market optimism is at the lowest level since the first week of October when 25.5% of respondents reported as bullish.

That big drop in bullish sentiment also means bearish sentiment has rocketed higher to 42.4%. That is the highest reading in bearish sentiment since the first week of October of last year. Similar to bullish sentiment, since the recent low of 24% three weeks ago, the 18.4 percentage point increase was the largest three-week uptick since March 2020.

Due to the big inverse moves in bullish and bearish sentiment, the bull-bear spread has also collapsed from double-digit positive readings only two weeks ago down to the bottom decile of its historical range. At -15.7, the bull-bear spread is now at the lowest level since September 16th.

Even though bullish and bearish sentiments have seen big shifts, the percentage of respondents reporting as neutral has gone little changed. There was only a half percentage point increase this week up to 31% which leaves neutral sentiment roughly in line with its historical average (31.43%).

The AAII readings were not the only sentiment indicators that have collapsed. The NAAIM Exposure index has fallen to 87.87 this week; the first sub-100 reading in five weeks. Meanwhile, the Investors Intelligence (II) survey saw the highest reading in bearish sentiment since May 2020. Combined with a decline in bullish sentiment, the bull-bear spread has hit the lowest level since October 20th. In the chart below, we have created a sentiment composite taking the z-scores of the current readings across each of these three surveys (AAII and II bull-bear spreads and the NAAIM index). This shows that sentiment readings have gone from a historically elevated reading that is a full standard deviation above the historical norm all the way back to zero in three weeks’ time. In other words, sentiment has made a sharp pessimistic turn in the past few weeks, but current readings are overall not exactly bearish to any extreme degree. Click here to view Bespoke’s premium membership options.

Claims Remain Low

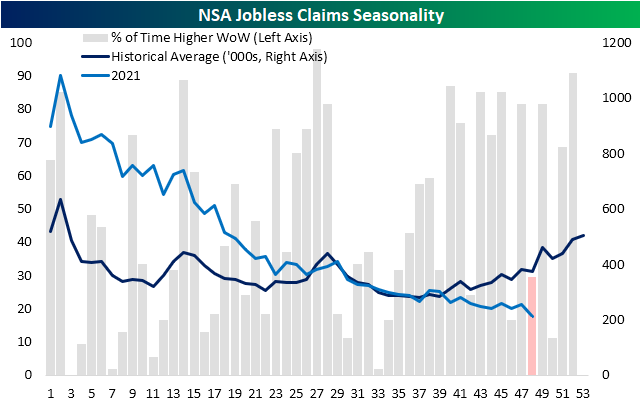

Last week saw the first sub-200K seasonally adjusted initial jobless claims print in over 50 years. This week, that number was revised even lower to 194K. While that reading sets a historic low, the most recent data for the week ending November 27th, however, saw claims rise by 28K to 222K. Although that marks the biggest one-week uptick in claims since July, the level of claims remains handily below pandemic levels and below the level of 256K from right before the COVID surge that took claims into the millions.

Last week, seasonal adjustments gave a significant boost to jobless claims as NSA claims actually came in at 253.5K versus the 194K adjusted reading. This week, NSA claims were the lower of the two coming in at 211.9K which is the lowest level since the first week of March 2020. With claims declining further, they continue to buck the seasonal trend. As shown below, the current week of the year has consistently seen a lower reading in NSA claims than the prior week as was the case in the most recent print. Currently, claims are at a new low for the year whereas historically they have been on the rise for several weeks now.

Lagged one week to initial claims, continuing claims also hit a pandemic low for the first sub-2 million print since March 2020. The 107K decline from last week’s revised number was the biggest one-week decline since October 22nd.

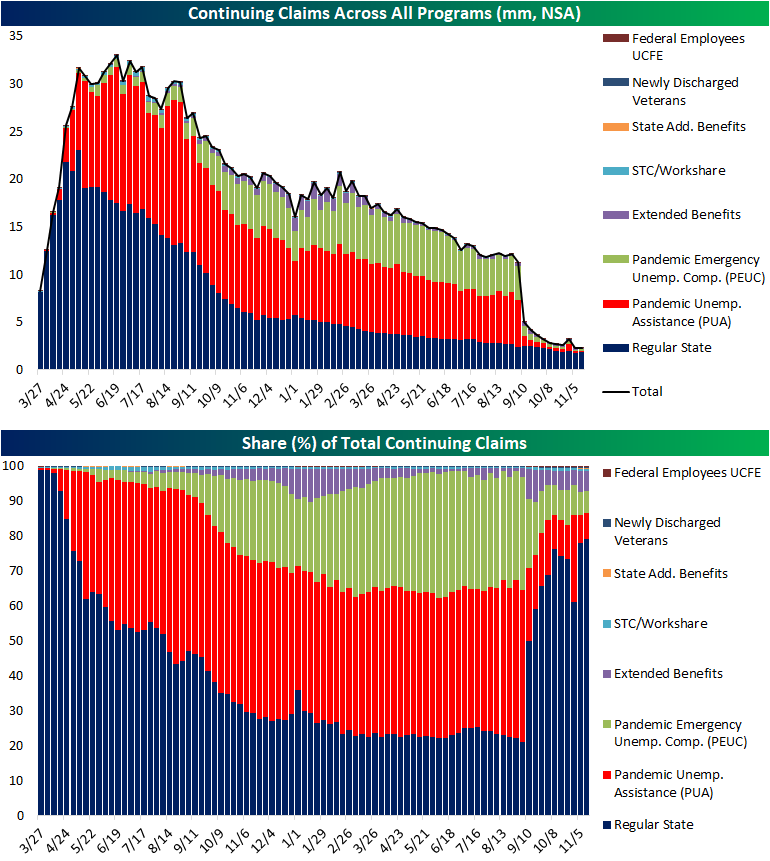

Including all programs delays the data by another week making the most recent reading through the week of November 12th. That week saw a slight uptick in claims led by gains in regular state programs. Pandemic era programs are largely unwound by now, but there is still a significant presence with over 300K claims coming from the PUA and PEUC programs. Click here to view Bespoke’s premium membership options.