Bespoke’s Morning Lineup – 3/11/22 – It’s Friday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“And Lord, we’re especially thankful for nuclear power, the cleanest safest energy source there is. Except for solar, which is just a pipe dream.” – Homer Simpson

It’s just a coincidence that Google searches for the term ‘nuclear war’ are hitting a record high as we’re marking the 11th anniversary of the Fukushima nuclear disaster in Japan, but the term nuclear has been showing up a lot lately. Whether it is Germany’s plan to shut down its nuclear power plants and make it even more reliant on Russian energy, or the Russian invasion of Ukraine that has raised risks of a nuclear accident at the site of the former Chernobyl plant or Ukraine’s other nuclear power plants that are operational, or the risk of nuclear war with Russia if NATO comes in to actively help defend Ukraine, you can’t get away from the subject of nuclear lately.

Thankfully, equity markets look to be putting a lot of these concerns aside temporarily giving investors a reprieve heading into the weekend. S&P 500 futures are currently up over 1%, crude oil is up over 1%, gold is down 1.5%, the 10-year yield is flat right at about 2.0%, and bitcoin is right around $40,000. The positive tone in equities was present for most of the night but just got an added boost shortly before 7 AM on reports that Russian President Putin said there were positive shifts in talks with Ukraine. At this point, the markets will take whatever good news they can get, but keep in mind that Putin is also the one who said Russia wouldn’t invade Ukraine.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s been a pretty nasty week for US equities since the close last Thursday. During that span, the S&P 500 is down over 2% while the Nasdaq is down 3%. The worst performing sector during this period has been Consumer Staples (XLP) which is down close to 5%, while Technology (XLK) and Financials (XLF) are both down over 3%. Rounding out the top five of biggest losers, Communication Services (XLC) and Consumer Discretionary (XLY) are both down over 2.5%. Not surprisingly, all five of the aforementioned sectors are also at short-term oversold levels.

While most sectors are lower, three have managed to buck the trend over the last week. Energy (XLE) has been the biggest winner, rising close to 6%, followed by Utilities (XLU) and Real Estate (XLRE). Unfortunately for the broader market, though, these three sectors are also the smallest sectors in terms of their weightings in the overall S&P 500.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Inflation Surge Continues, Fiscal Tightening, Strong Bond Bidding – 3/10/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight by taking a look at the backwardation of crude oil and crack spreads followed by an update on the situation in Ukraine. We then dive into today’s inflation data. Next, we look at government receipts and today’s historically strong 30 year bond sale.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

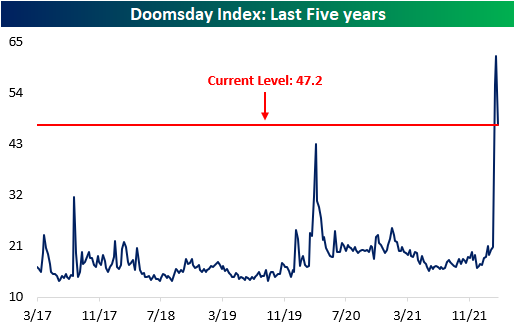

Doomsday Fear Index

During the Cold War, American children and adults were educated on how to best protect themselves from a nuclear explosion. This included measures from the silly “duck and cover” campaign to nuclear fallout shelter instructions. If you happen to be curious about the federal government’s current recommendations in regards to protection from a nuclear blast, you can read up on the instructions here. We’re not sure how focused people will be about wearing a mask in the event of nuclear fallout, but we guess you can never be too careful!

With tensions between Western nations and Russia reaching levels not seen since the Cold War, we took a look at Google Trends to identify the level of fear in the American population with respect to the current war in Ukraine. We looked at the search volumes for terms like nuclear war, WWIII, canned food, Potassium Iodide, and gas mask. Searches for many of these terms hit five-year highs in the early days of the Russian invasion but have subsided since. The current level is still well above normalcy, but fears appear to have eased over the last week as the West’s retaliation has been almost entirely economic (or maybe there is no internet service in the fallout shelters). The aggregate index is pictured below.

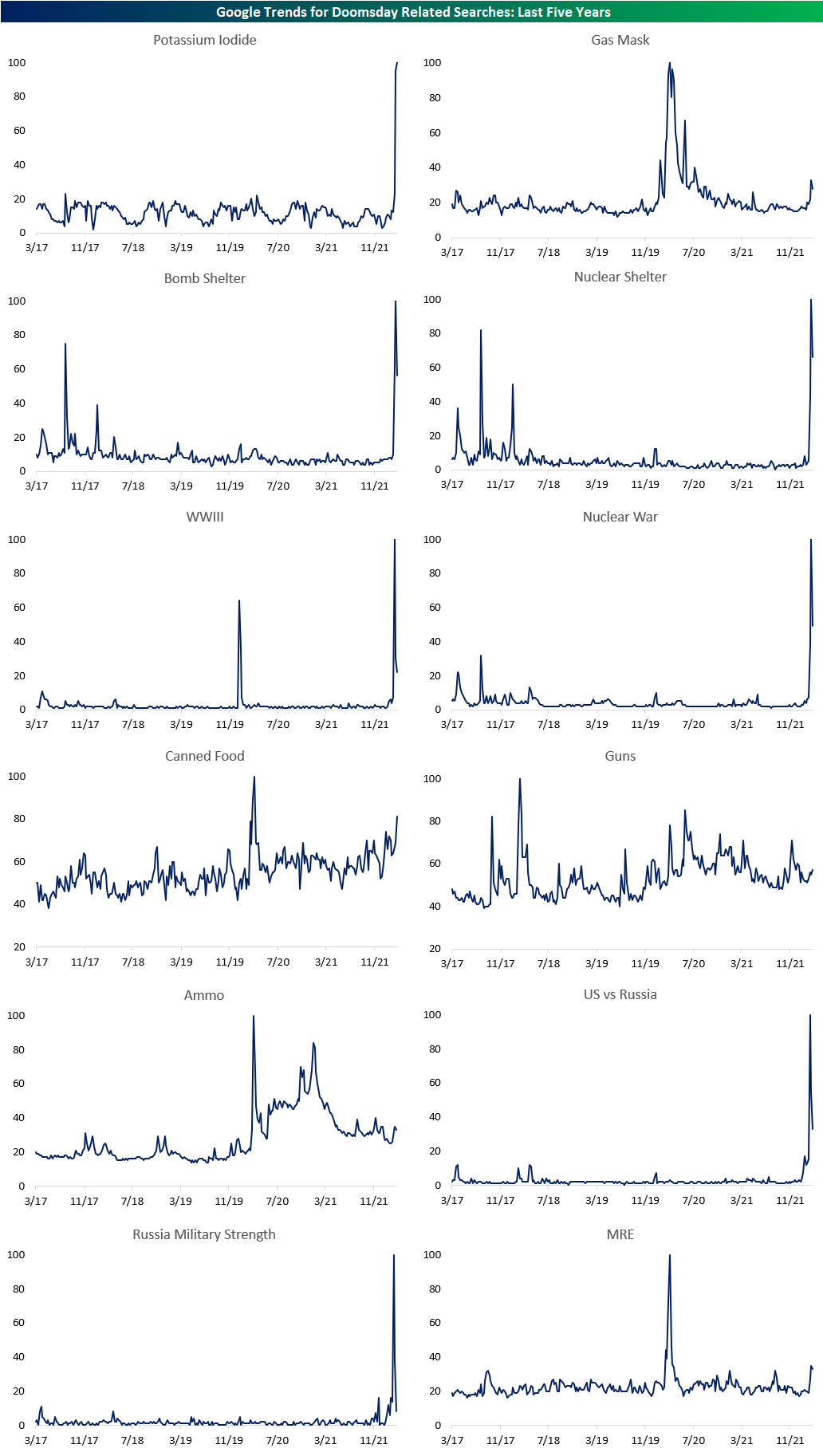

Below are charts of each search term we utilized in the composition of our index. Potassium Iodide, the compound utilized to mitigate the effects of excessive radiation exposure, is the only term that remains at a five-year high in terms of search volume. While searches for some of these terms were actually much higher during the early days of COVID, they all experienced upticks in the last few weeks. All-in-all, based on search trends based on fears of a nuclear situation or war with Russia spiked when the Ukraine invasion first started, but those fears have over the course of the last week. Click here to view Bespoke’s premium membership options.

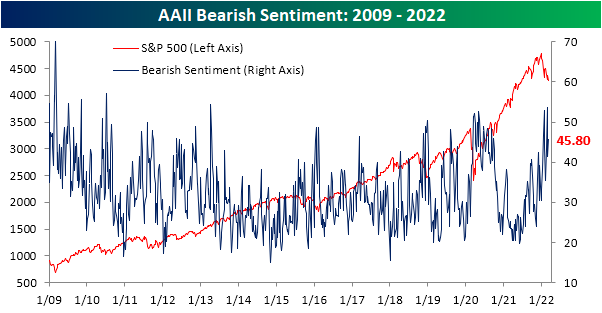

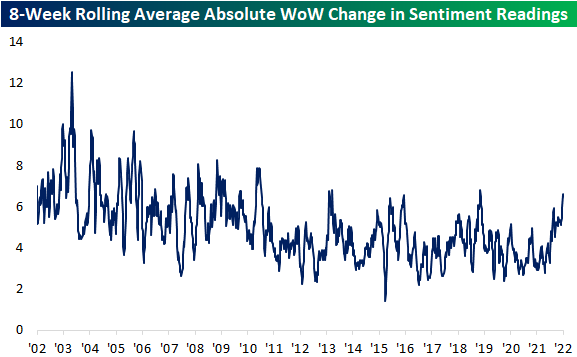

Investor Sentiment Remains Volatile

Considering equities and other risk asset prices continue to swing violently, so too have readings on investor sentiment. The weekly AAII survey of individual investors saw the percentage of respondents reporting as bullish fall back below 25% this week after rising above 30% last week. While that is not the largest drop in recent months (the second week of January saw bullish sentiment fall 7.9 percentage points compared to 6.4 today), it nonetheless reaffirmed that investor confidence is shaky, if not undecided, at the moment.

The drop in bullish sentiment was mostly picked up by those reporting as bearish. Bearish sentiment rose 4.4 percentage points to 45.8%. While that reading is roughly 15 percentage points above the historical average for bearish sentiment, the reading is still lower than an even more pessimistic reading only two weeks ago when more than half of respondents reported as bearish.

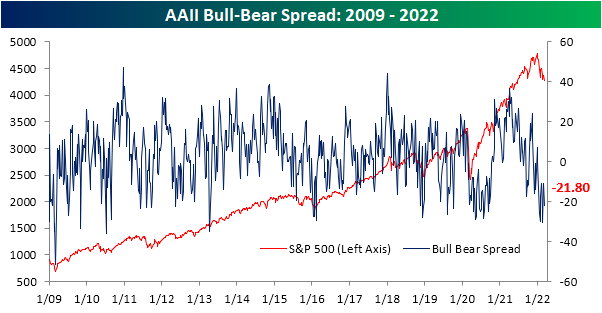

With the inverse moves in bullish and bearish sentiment, the bull-bear spread has pulled back to -21.8. As with bullish and bearish sentiment, even if that does not set a new low, it is only in the 5th percentile of readings going back to the start of the survey.

After the largest single-week decline in nearly 20 years two weeks ago, neutral sentiment has been clawing its way back into the range it was in for most of the past year. Gaining another 2 percentage points this week, the reading is now back above 30%.

Across each category of the report, there have been sizable swings in the past two months. To highlight this, in the chart below we show the eight-week rolling average of the absolute week over week change for each sentiment reading (bullish, bearish, and neutral) over the past 20 years. Over the history of the survey, weekly changes have gravitated towards smaller swings meaning the past decade is structurally a bit different relative to the decade before that. That being said, the weekly swings in the AAII readings on sentiment have been some of the largest of any period of the post-Global Financial Criss era. In fact, not even the COVID crash saw such volatility in sentiment (given optimism collapsed and then remained muted for some time rather than swing back and forth) while the only times this average was as high as now in the past decade were the spring of 2013, February 2016, and January 2019. Click here to view Bespoke’s premium membership options.

Little Need to Worry About Rising Claims

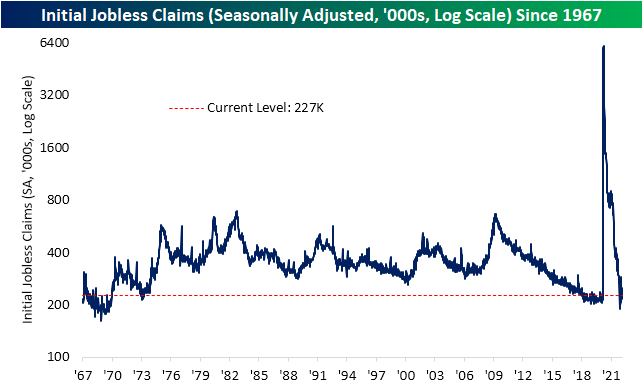

While today’s CPI data did not come in hotter than expected as feared (matching expectations of 7.9% YoY growth), jobless claims came in worse than expected for both initial and continuing claims. Seasonally adjusted initial claims rose to 227K versus expectations of a 2K increase from last week’s unrevised level of 215K. In addition to the higher reading this week, the last print was also revised up by 1K. In spite of the lack of improvement in claims recently (it’s been over 3 months since the multi-decade low of 188K set in early December), the level of claims remains historically low.

On a non-seasonally adjusted basis, claims for the current week of the year are in line with readings from the few years prior to the beginning of the pandemic. In terms of the seasonal pattern, the current week of the year typically has not seen claims rise week over week as they did this year. Claims tend to fall at this point of the year with the few weeks surrounding the current period marking some of the weeks of the year with the most consistent declines in claims. Regardless of the somewhat seasonally unusual move, the broader seasonal pattern this year has not marked a major divergence versus history.

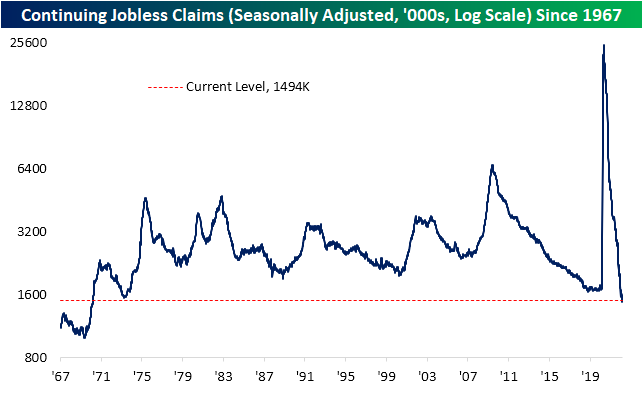

Continuing claims were expected to fall from 1.476 million down to 1.450 million. Instead, claims rose by 18K. As with initial claims, even though that is not as strong a reading as anticipated. It is far from leaving claims at any sort of worrisome level.Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 3/10/22 – Inflation Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The best way to destroy the capitalist system is to debauch the currency.” – Vladimir Lenin

It was fun while it lasted. After a much-welcomed rally Wednesday, futures are firmly in the red this morning and set to give up a little more than a third of their gains from yesterday, and as we’ve been typing this the losses have only been mounting. For the S&P 500, that would put this week’s losses at over 2% for the week. Meetings between foreign ministers from Russia and Ukraine did not yield any substantive results, so the fighting looks set to continue. Elsewhere in Europe this morning, the ECB left rates unchanged (as expected), but announced a faster timeline for its plan to wind down asset purchases.

The big economic event of the day is obviously CPI, and it’s not going to be pretty as the headline reading is expected to increase 0.8% relative to January, while the core reading is forecasted to increase 0.5%. Don’t forget about jobless claims, though. The weekly reading on initial claims is expected to come in at a level of 225K. One combination of data that the markets will not want to see is higher than expected readings on both fronts.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

There’s no arguing that the current levels of inflation are high and likely to go even higher in the months ahead. Since the start of 2021, there has only been one month (August 2021) where headline CPI has come in weaker than expected, and the compounded impact of these higher than expected monthly readings is the fact that today’s report for the month of February will mark the 9th straight month that y/y headline CPI has been above 5%. That’s a pretty long streak, but looking back over history, it’s nowhere close to as long as some of the prior streaks we have seen. Late in WWII and into 1920, headline CPI was above 5% for nearly five years. In the early 1940s during WWII through 1951, there were three separate streaks where headline CPI was above 5% y/y for at least a year. Then there was the 1970s coming out of the Vietnam War and into the early 1980s when there were three streaks that lasted at least 20 months including a five and a half year streak ending in 1982.

To put it another way, in the entire decade of the 1970s, more than 75% of all CPI readings were above 5% and the average y/y reading was 7.1%. Inflation is painful right now and will likely get worse from here, but the current period is still nowhere near the 1970s.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

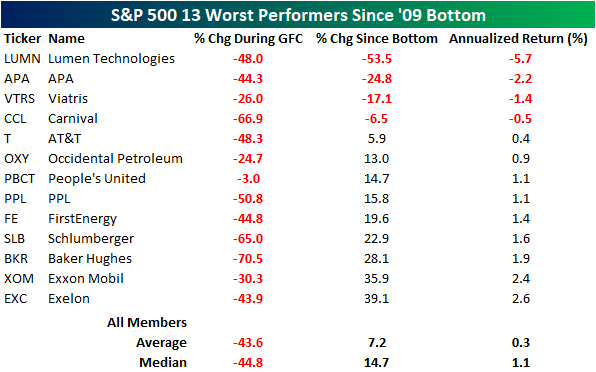

13 Years After the ’09 Bottom

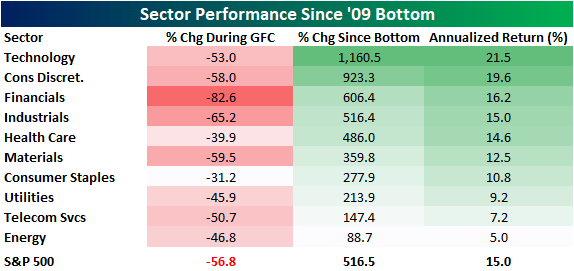

As we highlighted in a post this morning, today marks the thirteen-year anniversary of the 2009 market bottom of the Global Financial Crisis. Since then, the equity market has roared to the upside, rallying 531% (not including dividend) as of yesterday’s close, which constitutes annualized returns of 15%.

As expected, sector performance has been uneven. Technology has led the way to the upside, rising more than 11-fold and booking an annualized return of 21.5%. The Consumer Discretionary sector comes in second, with price appreciation of 923.3% and an annualized return of 19.6%. Energy has been the worst-performing sector, returning just 88.7%, which is an annualized gain of 5.0%. Telecommunication Services is the second-worst, gaining 147.4% (7.2% annualized). Again, all of these returns do not include dividends.

Turning to individual equities, the tables below highlight the thirteen best and worst-performing current members of the S&P 500 since the March 2009 lows. For each stock, we also include how the stock performed during the crisis (10/7/07 through 3/9/09). Starting with the winners, all but two of them fell more than 50% during the crisis with United Rentals (URI) falling more than 90%! All of these stocks have made up for those losses, though, with three rising more than 10,000% (an increase of 100X) over the last thirteen years. Of the current S&P 500 members, DexCom (DXCM) is the best performer in terms of price appreciation, booking an annualized return of 44.1%. NVIDIA (NVDA) and United Rentals (URI) have gained 42.9% and 42.8% annualized, respectively. Apple (AAPL) was already a large company in 2009, but its 35.7% annualized return moved it to the top of the charts in terms of the world’s largest companies.

There are only four current S&P 500 members that have seen negative price action since the bottom of the Global Financial Crisis, with those being Lumen Technologies (LUMN), APA (APA), Viatris (VTRS), and Carnival (CCL). The median annualized return of these names is a loss of 1.8 percent, not including dividends. Just to put this in perspective, only 11 of the 500 names currently in the S&P 500 have performed worse than the current 10-year treasury yield. The only one of these that is higher now than it was at the October 2007 peak is People’s United (PBCT). Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 3/9/22 – Rally Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Your reality is as you perceive it to be. So, it is true, that by altering this perception we can alter our reality.” – William Constantine

Equities are experiencing a monster rally this morning with S&P 500 futures up over 1.5% and the Nasdaq indicated to open higher by more than 2%. European stocks have rallied even more with Germany’s DAX up nearly 5%! As we have pointed out several times over the last several weeks, though, futures are only telling us where the market is now, and where we finish the day can easily look a lot different than it does now. Take the current level of futures, for example. At the open today, the S&P 500 will still be trading below yesterday’s afternoon high. We’ll take what we can get, though.

There’s seemingly not much in the way of a catalyst that can be cited for this morning’s move, but comments from a Russian spokesperson saying that Russia isn’t looking to overthrow the Ukrainian government have been cited by some as contributing to the move. These types of comments have been common over the last two weeks, though, and they differ from what has actually been taking place on the ground in Ukraine.

The only economic report on the calendar this morning is the JOLTS report, but it’s a January report, so it won’t be telling us anything we don’t already know.

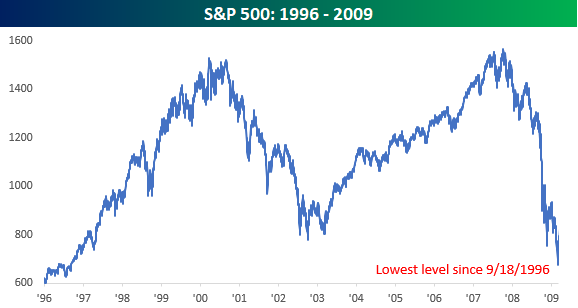

Lastly, today marks the 13-year anniversary of the Financial Crisis low in March 2009, ending what was one of the worst bear markets in US history, and if you remember that day, there wasn’t a lot of hope for investors as it looked like there was no way out for the market. The thing to remember regarding bear markets and market corrections, though, is that at the lows, the way out is never obvious.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Energy stocks have had a rally this year that can only be described as insane. Over the last 50 trading days, the Energy sector ETF (XLE) is up over 40% while the S&P 500 ETF (SPY) is down more than 11%. That works out to a spread of nearly 53 percentage points! Since XLE started trading in 1999, there has never been a 50-trading day period where the XLE outperformed SPY by as wide or wider of a margin.

Looking at the above chart, it’s hard not to argue that the Energy sector has massively gotten ahead of itself. 50 percentage points of outperformance in 50 days? Changing perspective a bit, though, shows just how depressed the Energy sector was relative to the rest of the market. The chart below shows the long-term relative strength of XLE versus SPY since the start of 1999. What a ride it’s been!

Basically from the time XLE started trading to mid-2008, it handily outperformed SPY, but in the 12 years that followed, XLE gave up all of its outperformance and more, only just recently getting back to even. Since the start of 1999, both ETFs have essentially experienced the same returns (+232% for XLE and +238% for SPY). So even after the recent surge in XLE, it is still slightly underperforming SPY over the last 23 years, and if you measure performance since the lows of the Financial crisis, SPY’s performance is more than five times the return of XLE!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Happy Anniversary!

Today marks the 13-year anniversary of the day when things got as bad as they can get for financial markets. After more than a year-long bear market which cut the value of the US stock market by over half, on 3/9/09, the S&P 500 closed at its lowest level since September 1996. A peak to trough haircut of more than 50% is enough, but bear markets are crueler than that, and this one was especially so. A case in point- on its way to zero in 2008, Lehman Brothers saw separate rallies of 24%, 53%, 26%, 70%, 34%, etc. and with each one, investors kept getting sucked back in thinking the worst was over.

Now, replay that scenario with every other stock in the Financials sector and you start to get the picture. On a market-wide basis; in the two weeks after the 2008 Election, the S&P 500 dropped more than 20%. Then, as President-Elect Obama started to announce his cabinet, markets breathed a sigh of relief. The naming of Tim Geithner as Treasury Secretary elicited an especially strong response, and from late November through year-end 2008, stocks recovered and rallied more than 20%. It was a new bull market! But at the start of 2009, any hopes of an enduring rally quickly faded as the S&P 500 resumed its downward slide.

As catastrophic as the stock market declines were, most Americans couldn’t be bothered with it, not because they weren’t busy losing their shirts or retirement saving, but instead because they were too busy wondering if the ATMs would still be working tomorrow or where they would stay when their homes were foreclosed. We hear a lot of market people who consider making it through the COVID Crash as a badge of honor, but for the markets, COVID was just a bad month.

The phrase gets tossed around a lot, but the period spanning the late 1990s through 2009 really was a lost decade for the US equity market and marked the first time since 1941 that the rolling 10-year return for the S&P 500 was negative. In the 1990s, we were all told that stocks only go higher over the long-term, but ten years later we had all just experienced the harsh reality first hand.

If you lived through it, late 2008/early 2009 was as bad or close to as bad as it gets. Financial blood was in the streets and the bodies of failed banks and brokerages were piled up. By March 2009, no one even wanted to hear the word stock, and the mere mention of the stock market was enough to leave you by yourself at a party. As these things often work, March 2009 ended what was a nearly 13-year period of no gains in the stock market and the beginning of a nearly 13-year massive rally. There were bumps along the way, but they were mostly short-lived, and even after this year’s brutal start, the S&P 500 is still up over 500% from those lows.

As much as sentiment has worsened and as painful as the declines from the January highs feel now, they are a blip when viewed in the context of the last 13 years. Just to put things in perspective, on Monday, the S&P 500 fell more than 2.95% for its worst one-day decline since October 2020. From September 2008 through March 2009, though, there were more than 30 one-day declines of 2.95%! For another example, the CBOE Volatility Index (VIX) closed above 30 for the 7th straight day on Tuesday, which is one of just 17 streaks where it has closed over 30 for seven or more days. On 3/9/09, though, the VIX closed at just under 50 in what was the 121st straight day of closes above 30 and ultimately the longest ever streak of closes above 30 (170). In other words, as bad as it feels now, things could get a lot worse.

Conversely, whenever you hear someone say there’s no way out from here for equities, remember March 2009, March 2020 at the COVID lows, and every other bear market or correction low. The way out for the market was never obvious. It never is. Click here to view Bespoke’s premium membership options.

/

/{kind=link}

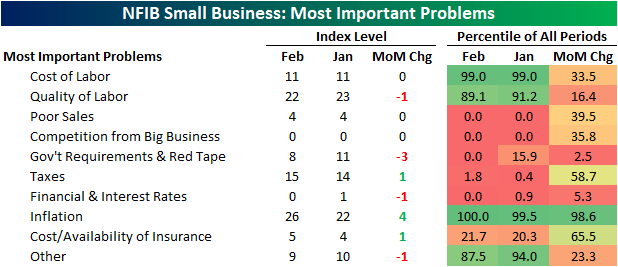

The Little Guy Eying Inflation

Looking across the range of issues surveyed by the NFIB, labor and inflation remain front and center of what most concerns small businesses. As shown below, the combined percentage of respondents reporting either cost or quality of labor as their most important problem continues to be the most prevalent topic with 33% of firms reporting as such. That is down slightly from 34% in January thanks to the decline in quality of labor. Most other categories fell to or remained at record lows. Such was the case for Poor Sales, Competition from Big Business, Government Requirements and Red Tape, and Financial & Interest Rates.

Last month the percentage of respondents reporting inflation as their biggest problem went unchanged from the December reading of 22%. This month that reading gained another 4 percentage points to cross above a quarter of all respondents for the first time on record going back to 1986. Behind labor concerns (the combined reading of cost and quality of labor), this is the most commonly reported problem, and based on the action in commodities prices over the last couple of weeks, this reading will almost certainly increase again next month.

That means what has usually been the second most important problem on a combined basis recently, government requirement and taxes, dropped in the ranking. In fact, the 3 percentage point decline in government requirements offset the one percentage point increase in taxes to tie the November 2005 reading for the lowest on record. As we have noted in the past, the past few presidential cycles have structurally seen lower readings in these indices when Republicans were in office and vice versa when Democrats have held the presidency. With Biden currently in office, the record low reading is somewhat unusual from this political perspective.

That is not the only category that has fallen to record lows. Poor sales and competition from big business have both fallen dramatically in the past couple of years. Click here to view Bespoke’s premium membership options.