Bespoke Brunch Reads: 10/16/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Billionaire Whimsy

Elon Musk Has the World’s Strangest Social Calendar by Joseph Bernstein (NYT)

A categorization of the strange and fragmented social life enjoyed – or perhaps, not enjoyed – by the Tesla CEO, who hops from one fragmentary encounter to the next across a sea of private jet flights, galas, and VIP lounges. [Link; soft paywall]

‘I Am Energy’: Inside the Bang Billionaire’s Reeling Empire by Anders Melin (Bloomberg)

A heartrate-popping profile of an energy drink company taking on the giants of the industry fueled by the mashup of hype, energy, and shady dealings that scream “Florida” from top to bottom. [Link; soft paywall]

China

World Bank Cuts China Growth Forecast as Covid-19, Real-Estate Crunch Take Toll by Jason Douglas (WSJ)

The combination of collapsing property activity and restrictions on activity related to COVID-19 are suppressing Chinese growth that is also hampered by Fed tightening. [Link; paywall]

Ocean plastics: How much do rich countries contribute by shipping their waste overseas? by Hannah Ritchie (Our World In Data)

A ban on imports of plastic waste to China has helped push down global plastics trade volumes dramatically, helping to reduce the volume of plastic being transported by sea and therefore plastic waste that makes it in to oceans. [Link]

Labor Relations

Exxon’s Exodus: Employees Have Finally Had Enough of Its Toxic Culture by Kevin Crowley (Bloomberg)

A revealing narrative that illustrates how pressure on companies to decarbonize or behave more ethically often comes internally, rather than externally from investors following the precepts of ESG investing. [Link; soft paywall]

Medical Marvels

Human hibernation is a real possibility – this is how it might work by Alex Wilkins (NewScientist)

Our ancient ancestors may have hibernated, a common survival strategy among mammals. Dormant brain paths may be the key to recovering that ability which has since been lost. [Link; paywall]

How a Diabetes Drug Became the Talk of Hollywood, Tech and the Hamptons by Sara Ashley O’Brien (WSJ)

A drug meant to help manage Type 2 diabetes is being used off-label for weight loss; another drug that uses a similar active ingredient is approved for weight loss among those with clinical weight management challenges. [Link; paywall]

Policy

Biden Proposal Could Lead to Employee Status for Gig Workers by Noam Scheiber (NYT)

A proposed rulemaking by the Labor Department would create a test to determine whether gig workers are employees or contractors, opening up a potential requirement to pay benefits and minimum wages at scale. [Link; soft paywall]

It’s Official: The Fed’s in the Red by Tracy Alloway (Bloomberg)

Rising payouts of interest amidst a stable yield on portfolio securities mean the Federal Reserve is now recording operating losses on a weekly basis. [Link; soft paywall]

How California’s Bullet Train Went Off the Rails by Ralph Vartabedian (NYT)

Good old fashioned corruption turned a laudable effort at building a high speed rail link into a boondoggle of historic proportions. [Link; soft paywall]

Astrophysics

Black Hole Pukes Up Star Years After Eating It by Isaac Schultz (Gizmodo)

After gobbling down a star three years ago, a black hole spit back up material at half the speed of light. Scientists are trying to understand why. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Equity Risk Gauge

This week’s Bespoke Report newsletter is now available for members.

In this week’s newsletter, we highlight some absolutely crazy market stats from the last few trading days and then introduce a new “equity market risk gauge” that clients can use to quickly understand our overall market view using eight key components.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Bespoke’s Morning Lineup – 10/14/22 – Let the Games Begin

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Just before you break through the sound barrier, the cockpit shakes the most.” – Chuck Yeager

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Let the games begin. Today marks the unofficial start to earnings season as the major banks come out of the gate with what have generally been positive results. Of the seven banks reporting, five exceeded EPS forecasts, one (Morgan Stanley) missed and one was inline (US Bancorp). Besides the Financials, UnitedHealth (UNH) also reported and topped forecasts on both the top and bottom lines. It’s still early, but so far, no major disasters. JPMorgan Chase (JPM) is even poised to trade higher in reaction to earnings which, if it holds, would be something it hasn’t done in over two years!

Outside of earnings, it’s a busy day for economic data this morning with Retail Sales (mixed relative to expectations), Import Prices (lower than expected), Business Inventories, and Michigan Sentiment all on the docket between now and 10 AM. If that wasn’t enough, we’ll also hear from three different Fed officials (George, Cook, and Waller). So much for a quiet Friday.

In international news, the German economic ministry said that a recession likely started in Q3 and will last for three quarters. The political situation in the UK continues to be a mess as PM Truss will reportedly reverse her tax plans and allow the corporate tax rate to increase while at the same time sacking her finance minister. That news has pushed the yield on the 10-year gilt down 23 bps and below 4%.

US Futures are still in positive territory, but they are well off their highs, and if the last several weeks have told us anything, it’s that where the market starts the day and where it finishes usually varies widely.

75 years ago today, Chuck Yeager accomplished the ‘impossible’ becoming the first pilot to ever break the sound barrier. Up until that time, the thought among ‘experts’ was that once an aircraft approached the speed of sound it would break apart resulting in the death of the pilot. Not really the way anyone wants to go out. Yeager proved the experts wrong, but in the moments leading up to that point, he remarked that the cockpit of the aircraft starts to shake violently.

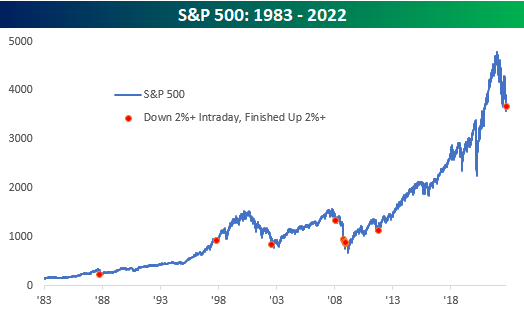

Based on Yeager’s description, the market looks like it’s trying to break its own sound barrier. After trading up over 1% in pre-market trading yesterday, the stronger-than-expected CPI erased all the gains and more. Shortly after the open, the S&P 500 had dropped nearly 4% from its pre-market highs before staging an epic rally of over 5%. Even in this ‘all or nothing’ type of market environment, reversals of that magnitude are rare.

As shown below, prior to yesterday there were only nine other days since 1983 when the S&P 500 fell more than 2% intraday but finished the day up over 2%. The most recent occurrence was over eleven years ago on 10/4/11 and before that, there were five separate occurrences in 2008 alone! The three remaining reversals were in 2002, 1997, and 1987.

We’re not sure when or where the ultimate bottom in stocks will end up, but violent moves like yesterday tend to occur closer to lows than highs. It’s easy to remember the good parts of a bull market where stocks rally, but people usually forget that long-term rallies emerge out of chaos where investors become increasingly convinced that the only viable path if any exists at all, is lower. The early days of bull markets feel like anything but a sure thing.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke 50 Growth Stocks — 10/13/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Hurricane Claims Come In

Last week’s jobless claims number went unrevised whereas the latest week’s data rose by 9K up to 228K. That brings the seasonally adjusted number back up to the highest level since the end of August and was the first back-to-back increase since the first week of August.

On a non-seasonally adjusted basis, claims remain a hair below 200K and in line with the readings from the comparable weeks of the year in the few years before the pandemic. We would also note that the increase in claims at this point of the year is very much a regular occurrence.

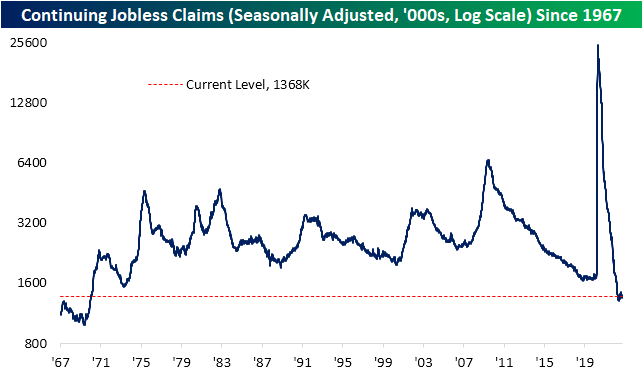

Turning to continuing claims, the latest print for data through the end of September saw a modest 3K increase to 1.368 million. That is only the highest level in three weeks as the indicator remains well below pre-pandemic levels, unlike initial claims.

On a national level, claims are moving higher but it is perhaps too early to say we are in a new trend as opposed to things like seasonality and one-off events like the weather. While 80% of states and territories saw claims move higher this week, a large share of the national move was concentrated in the Southeast likely as a result of Hurricane Ian. In the table below, we show the state-level readings for initial and continuing claims (NSA). Roughly a third of the national move in claims was thanks to claims in Florida more than tripling week over week. Now, initial claims in that state are at the highest level since May of last year. That was matched with a significant pickup in continuing claims as well. Although they have a smaller impact on national claims, other hurricane-impacted areas like Puerto Rico also saw a significant uptick in initial claims. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 10/13/22 – Pre Inflation Strength

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Inflation is the crabgrass in your savings.” – Robert Orben

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures were higher most of the night but really picked up steam in the last hour following reports out of the UK that the Truss government was looking to reverse some of its recent tax proposals. In reaction, gilt prices are rallying, the pound is surging, and equity futures around the world have rallied. Now, if only the CPI report would cooperate. The pace of earnings is starting to pick up and this morning we got better-than-expected reports from Blackrock (BLK) and Taiwan Semi (TSM), while Delta (DAL) and Domino’s (DPZ) missed on the bottom line.

Weaker-than-expected CPI reports have become endangered over the last several months as economists just haven’t been able to keep up with the rapid increase in prices. Heading into today’s report for September, there have only been three reports in the last two years where headline CPI came in lower than expected and just one in the last year. In both cases, the 12- and 24-month totals have been at or near record lows. The average 12 and 24-month totals of weaker-than-expected reports have been 8 and 4, respectively, indicating that two-thirds of the time consensus forecasts are either at or below the actual reading. Simply put, economists have historically underestimated inflation, but the recent degree of underestimating price increases has been unprecedented to the point where betting on a higher-than-expected report has been nearly as bankable as it used to be taking the over in the NBA all-star game.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Semis Set to Turn?

In last night’s Closer, we highlighted the diverging performance of two industries that have often been considered leading groups for the broader market: the Philadelphia Semiconductor index (SOX) and the Dow Jones Transportation Average. As of this writing, that divergence has continued today with the Transports gaining another 1% while the more new age semiconductors are down 0.7%. As a result, the ratio of the transports to the semis has continued to rally off its recent lows.

![]()

In fact, the five-day rate of change of that ratio has now risen into the double digits as it sits 12.23% above last week’s levels. Surges in the ratio like we have seen over the last week have historical precedence, but very little following the dot com era. The only recent increases that were as large or larger than the current run were in March of last year (2021) and December 2017.

![]()

In the table below, we show each time since 1994 (when the Philly Semiconductor Index begins) that the ratio mentioned above has risen by at least 10% in a one-week span without another occurrence in the prior 3 months. The current run higher in the ratio has been on the larger side of those prior instances.

However, that outperformance has not necessarily carried forward. The next week has consistently seen the Dow Transports turn lower whereas the semis have consistently posted solid gains. Looking at performance in the medium to longer term, again the semis tend to outperform with more consistently positive moves that are also much better than the norm. For example, three and six-month performances for the semis have, on average, been around three times larger than the norm for all periods. Transports, meanwhile, have seen performance that is more in line with the historical norm. Click here to learn more about Bespoke’s premium stock market research service.

![]()

Bespoke’s Morning Lineup – 10/12/22 – Is That Green on the Screen?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is well that war is so terrible, or we should grow too fond of it.” – Robert E. Lee

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The big news item of the day will be the September PPI which is being released as we type this, and the results were not all that good. Headline PPI came in at 0.4% versus forecasts for an increase of 0.2%. Core PPI was in line with forecasts at 0.3%. On a y/y basis, the headline reading came in at 8.5% versus forecasts for an increase of 8.4%. Y/Y Core PPI was actually slightly weaker than expected at 7.2% versus forecasts for 7.3%. Futures were higher heading into the print along with US Treasury yields as the 10-year trades back up near 4%, but equities have now given up nearly all of their gains in the immediate aftermath of the report.

Pepsi (PEP) reported better-than-expected earnings and sales and also raised guidance this morning, and the stock is trading 2.5% higher in response. Today is really just the warmup for tomorrow, though, when we’ll get the release of CPI and banks will kick off the Q3 earnings season. In the meantime, keep an eye on the UK as officials there can’t seem to make up their minds on how long they intend to support the gilt market.

With the S&P 500 down five days in a row, the number of down days this year continues to pile up. Through Tuesday’s close, the S&P 500 has traded down on 56.9% of all trading days. That may not sound all that extreme, but since the five-trading day week began in late 1952, this year is currently on pace to have the second-highest percentage of down days in a given calendar year. The only one with a higher percentage of down days was 1974 (58.3%) when the S&P 500 was down 29.7% for the calendar year. Barring a major reversal in Fed policy, which is only taking on an increasingly hawkish stance even as economic activity shows signs of weakness, 2022 could end up in the record books.

Not only has the S&P 500 experienced a large number of down days, but the frequency of big down days has also been at historical extremes. 2022 just took out 1974 for third place in terms of the percentage of down 1% days, trailing only 2008 (29.6%) and 2002 (28.6%). Just as the S&P 500 was down nearly 30% in 1974, 2008 and 2002 were horrible years as well with declines of 38.5% and 23.4%, respectively. If it Ever Went Up, They Wouldn’t Call it Losing

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

B.I.G Tips – Apprehension Ahead of Earnings Season

We’re on the cusp of another earnings season as Thursday will unofficially kick off the Q3 reporting period when the major banks and brokers start to report their results. Once again this quarter, there’s no shortage of concerns for investors and analysts to factor into their models, so the upcoming period promises to be volatile. For a more detailed rundown of the earnings schedule for the upcoming season, please see our Earnings Explorer Tool (available to all Institutional clients) on the Tools section of our website, and to see our quarterly preview of the upcoming earnings season with respect to analyst sentiment heading into it, start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Inflation and Labor Still A Problem

The NFIB released its latest small business survey this morning with data as of the month of September. As we discussed in today’s Morning Lineup, the report showed sentiment rebounded in September although labor market indicators decelerated further. That was also reflected in the report’s survey of what businesses consider to be their most important problem. While those reporting ‘cost of labor’ as the biggest problem went unchanged, the percentage of respondents reporting quality of labor as their biggest concern dropped four percentage points to 22%. While there was an even lower reading as recently as July, it was the biggest drop since last December, and the current level has fallen out of the top decile of historical readings.

While the lower reading in labor market-related problems seems to reaffirm the slowing employment situation, inflation concerns ramped up modestly in September. 30% of businesses (versus 29% in August) reported inflation as their biggest concern. Additionally, another inflation-adjacent reading also rose with 5% reporting the cost or availability of insurance to be their biggest problem.

On a combined basis, government-related concerns saw a net lower reading last month as well. Concerns around requirements and red tape rose up to a 5% share of responses, but those gains were offset by a two percentage point drop in the share of respondents seeing taxes as their biggest issue. With inflation and labor concerns remaining front and center of small business problems, government-related concerns continue to be muted to a historic degree.

While the bulk of responses view labor or inflation as their biggest issues—62% of combined responses report one of these to be their biggest problem—there was a considerable pickup in those choosing “other” as their response last month. That reading rose from 5% to 8% bringing it from a 14th percentile reading all the way up to the 65th percentile. That is now the highest reading since May when it came in at an elevated 11%. Unfortunately, the report does not provide further detail as to what those “other” concerns specifically are but geo-political issues are likely part of the mix. Click here to learn more about Bespoke’s premium stock market research service.