Oct 12, 2018

It’s a much different picture for the equity market this morning than it was yesterday, with futures indicating a sharply higher open. Just to reiterate our point from yesterday, though, we continue to expect violent moves both up and down throughout the trading day. On a positive note, JPMorgan, Citi, and Wells Fargo are all currently trading up on earnings. Hopefully, that initial positive reaction can hold.

After yesterday’s big decline, the S&P 500 closed 3.77 standard deviations below its 50-DMA, which is the most oversold reading for the index since August 2015! As shown in the chart below, occurrences of the S&P 500 trading 3.5 standard deviations or more below its 50-DMA are few and far between in the index’s history. Since 1928, there have only been 18 such occurrences.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 11, 2018

It’s not looking like a pretty morning for equity bulls today, but with the DJIA futures indicating an opening decline of just over 200 points, things look a lot better than they did a few hours ago. As always when the market’s get into one of their moods, things tend to move in fits and starts before calming down, so expect to see some violent swings throughout the day. The opening bell is only an hour away, but we could just as easily see an up open when the bell rings as we could see a down 400+ open. In the big picture, while today’s early weakness is disappointing, positive futures following a day like yesterday are often met with selling.

In today’s Chart of the Day, which was just sent out a short time ago, we looked at S&P 500 performance figures following 3% down days. Be sure to check it out.

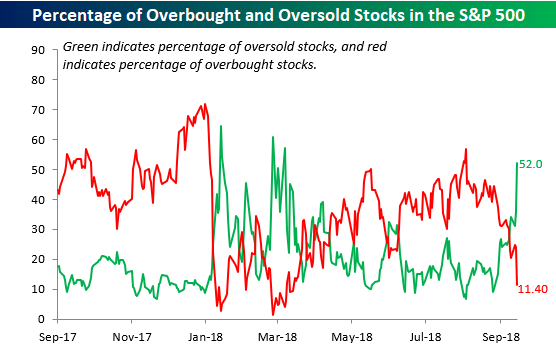

Yesterday’s fifth straight day of declines has really moved the S&P 500, most of its sectors, and a lot of stocks into oversold territory. Among individual S&P 500 stocks, more than half (52%) are now trading more than one standard deviation below their 50-DMA, which is the highest reading in over six months.

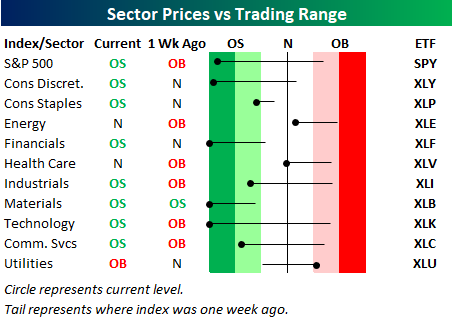

Among the S&P 500’s major sectors, just three (Energy, Health Care, and Utilities) are not oversold and three (Financials, Materials, and Technology) are trading more than three standard deviations below their 50-day moving average- a level that we would unscientifically call ‘waayyy’ oversold. The S&P 500 is also trading at oversold levels, but still hasn’t quite reached those ‘waayyy’ oversold levels.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 10, 2018

Futures may be trading pretty flattish ahead of the open, and the S&P 500 may be right at its 50-day moving average, but don’t let the sense of calm fool you. There’s still a lot of rotation and big swings underneath the surface.

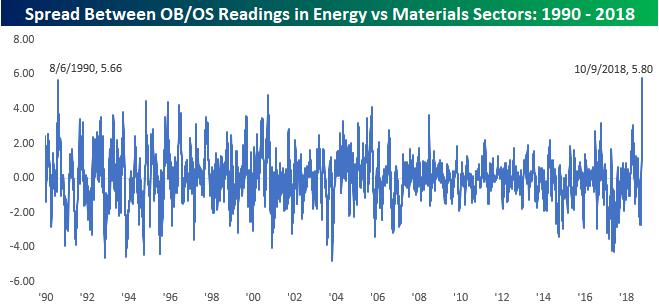

One example of that rotation is evident in the Materials and Energy sectors. As of yesterday, the Materials sector closed 3.83 standard deviations below its 50-DMA after dropping more than 3% yesterday. Meanwhile, the Energy sector has been acting well and finished the day 1.97 standard deviations above its 50-DMA. Going all the way back to 1990, there has never been a point where the spread between the two sectors Overbought/Oversold readings was wider. The prior record spread between the two sectors was in August 1990 just after Iraq invaded Kuwait. Talk about a divergence!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 9, 2018

Futures are trading lower again this morning as rising interest rates and weakness in Europe are keeping a lid on any gains in the US. Worries over earnings are also a concern as we head into earnings season.

Earnings season hasn’t even started, but already we may have one company that will serve as a microcosm for all the concerns that investors have heading into the period. Last night, PPG Industries (PPG) lowered guidance for the quarter citing factors like rising input costs, weaker demand from the auto sector for its paints, softening demand from China due to trade tensions, the stronger dollar hurting foreign demand and weakness in emerging markets. If you were to sum up all of the concerns that investors have that could possibly have a negative impact on company results in Q3, PPG mentioned them!

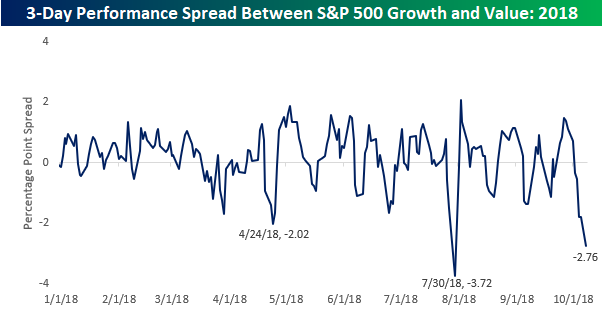

Growth stocks have been taking it on the chin over the last three days, and once again we find ourselves in a situation where they are sharply underperforming value stocks in the short term. Over the last three trading days, the S&P 500 Growth index is underperforming the S&P 500 Value index by over 2.5%. So far this year, this is only the third time that the S&P 500 Growth index has underperformed Value by more than two percentage points over a three trading day period. The last two occurrences were in late April and late July.

This is the third time this year that growth has underperformed value by over 2% in 3 days.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 8, 2018

Up here in the Northeast, Autumn seemed to literally come right before our eyes this weekend as the solid green blanket of foliage still in place Saturday morning gave way to the annual mosaic of yellows, oranges, and reds by Sunday afternoon. It really came quick!

In the market last week, we also saw some big shifts in performance as sectors like Consumer Discretionary, Technology, and Consumer Staples all sold off and dropped below their 50-day moving averages, while sectors like Financials and Energy moved in the other direction. Whether or not this is part of a longer-term cyclical shift remains to be seen, but the picture is no longer as green as it once was.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 5, 2018

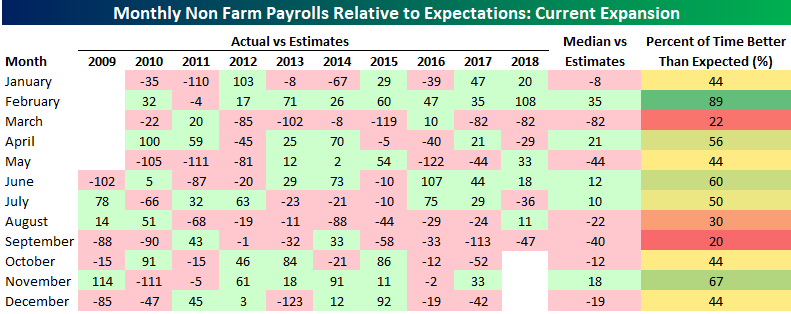

This morning’s release of the September Non-Farm Payrolls (NFP) report came in considerably weaker than expected at a level of 134K vs estimates for a gain of 181K. This weaker reading was especially surprising given the fact that most secondary indicators of employment for the month were positive. In this case, though, it must have all come down to seasonality. As we highlighted in yesterday’s preview report, “Seasonality is one factor not working in favor of a strong report tomorrow. Along with March, no other month has seen a weaker than expected initial release of the NFP more often than September.”

As shown in the table below, with today’s NFP report coming in weaker than expected again, September is now in the lead all by itself in terms of the greatest frequency of weaker than expected reports. In September reports over the last ten years, the initial release has only exceeded forecasts twice.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.