Oct 4, 2018

Global bond yields have been on the rise all night and all morning continuing the trend that started in US Treasuries yesterday. Equity futures are trading lower in reaction, and semis will be an area to watch again as Deutsche Bank is the latest in the chorus of sell-side firms to cut numbers on the group. Despite the uptick in negative analyst commentary, the Philadelphia Semiconductor index has traded up for five straight days. If the sector can squeeze out a sixth straight day of gains in spite of the negative commentary, that could signal a turn for the group.

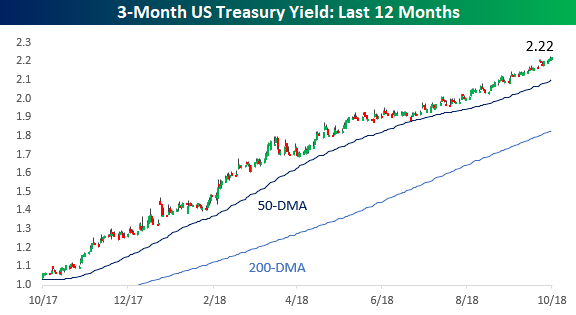

As mentioned above, interest rates are the main focus today. At the short end of the curve, the 3-month Treasury yield continues to move steadily higher hitting a level of 2.22% this morning.

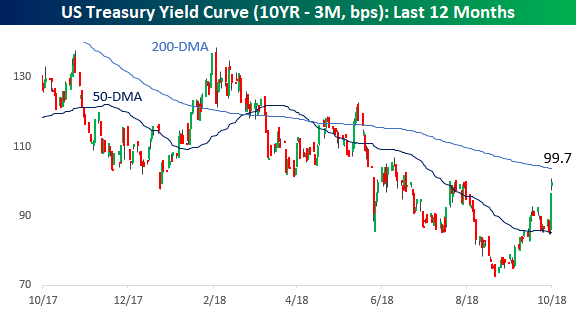

There’s been nothing ‘steady’ about yields at the longer end of the curve, though, as the 10-year yield broke out to 3.22%- its highest yield since 2011!

With that breakout in the long end of the curve, the yield curve has spiked from its recent lows in the 70-bps range to just under 100 bps today.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 3, 2018

Relief out of Italy that the country may reign in spending a bit more than previously planned has European equities trading higher this morning, and Us equity futures are following along in the footsteps.

Two of the most hated sectors in the market right now are homebuilders and semis, and this morning there is news that could impact both sectors. One good and one bad.

First the good news. In the homebuilder space, Lennar (LEN) reported better than expected earnings on revenues that were slightly better than estimates. The stock is trading up over 2% in reaction, but it will be important to see if those gains can hold. Recent positive news for the sector hasn’t had much staying power.

In the semiconductor space, Morgan Stanley cut estimates on the group after downgrading the sector back in the Summer. There’s been a lot of negative commentary towards the semis in recent weeks, so how the group reacts to today’s negative commentary could provide a good tell for the fourth quarter.

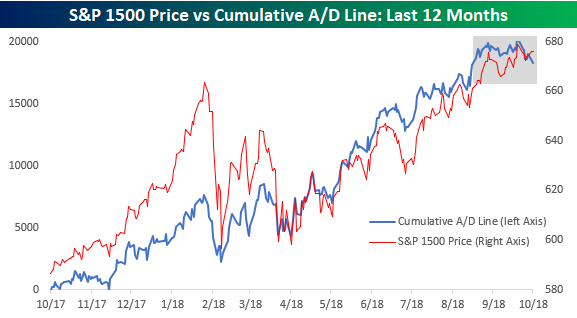

As the number of stocks hitting 52-week lows has increased in recent sessions, there’s been a lot of talk about weakening breadth in the market over the last several sessions. We have repeatedly highlighted the fact that breadth among large-cap stocks continues to be strong, but we’ll be the first to admit that among smaller and mid-cap stocks, breadth hasn’t been as positive.

The chart below shows the S&P 1500 (which comprises large-cap stocks in the S&P 500 as well as mid-cap stocks from the S&P 400 and small-cap stocks from the S&P 600). While the picture here isn’t quite as strong, it is hardly showing signs of a major negative divergence either. In fact, both the cumulative A/D line and the index’s price both hit their most recent all-time highs on the same day (9/20). That said, there is a clear case to be made that in the short-term breadth among the S&P 1500 stocks has flattened out, even as equities have rallied. In fact, while the S&P 1500’s cumulative A/D line is at the same levels it was at on 8/20- a month before the peak- the S&P 1500’s price is 2.3% higher. Not a major divergence yet, but something worth keeping an eye on.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 2, 2018

What was looking like quite a bad morning for US equities when our alarms went off a few hours ago is looking a lot more manageable now as futures have rallied off their lows.

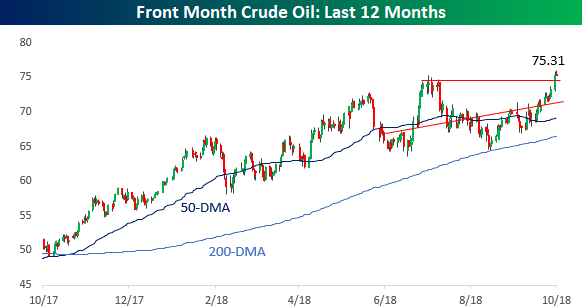

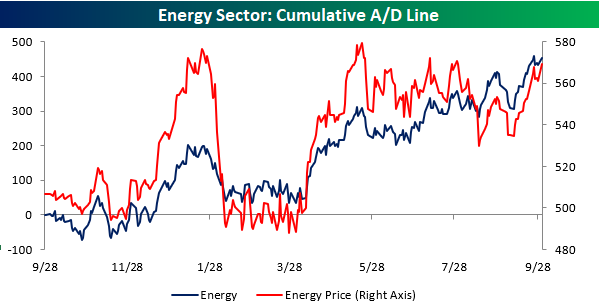

In yesterday’s session, the big star of the day was oil and the Energy sector in general. Driven by a 2.8% rally in crude oil prices, the S&P 500 Energy sector jumped 1.5%. Checking out the charts for oil and the Energy sector show some positive trends.

Crude oil prices are relatively quiet today, but yesterday’s rally took the front month future to a new 52-week high with a breakout above the summer highs.

While not at a new high, the S&P 500 Energy sector looks to be on the right path after convincingly breaking its downtrend from the highs in the Spring. Also working in the sector’s favor is that along with the rally in crude oil, natural gas prices also rallied yesterday to their highest prices since January.

Internals for the Energy sector also look positive. The chart below compares the sector’s price and cumulative A/D line. While prices aren’t yet at new highs, breadth has been strong and consistently trending higher for the last several weeks.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Oct 1, 2018

The opening bell hasn’t even rung yet, but already Q4 is looking to pick up right where Q3 left off with futures indicating a strong start to the week, month, and final quarter of 2018. Obviously, the big catalyst this morning is the announced trade deal the US has reached with Canada to join the US-Mexico trade agreement.

Another area where Q4 is picking up right where Q3 left off is in analyst sentiment towards the semis. As shown in our “Analyst Actions” section of the Morning Lineup, there’s been a number of downgrades of semiconductor stocks this morning with Morgan Stanley downgrading Intel (INTC), Baird cutting AMD, and both Mizuho and Deutsche Bank cutting Lam Research (LRCX).

The negative sentiment towards the semis is really nothing new at this point. Intel, for example, is down 17% from its highs. Short interest levels also show that negative bets towards the semis have been building for some time. As the most recent data (through mid-September) illustrates, the average short interest as a percentage of float for stocks in the semiconductor group is at the highest levels since October 2014!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Sep 28, 2018

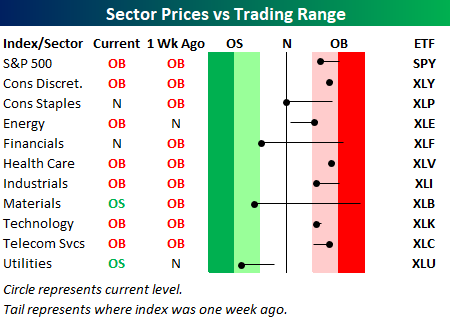

Investors are getting back to focusing on markets this morning yesterday’s spectacle in Washington has come and gone. With just one trading day left in the week though, we thought it would be a good idea to highlight where things stand on a sector by sector level.

The chart below is from the second page of our Morning Lineup and shows where sectors are trading with respect to their trading ranges and how they’ve moved over the last week. The S&P 500 and most sectors continue to trade at overbought levels, although everyone with the exception of Energy and Communication Services has moved lower with respect to its trading range over the last week. The big movers, though, have been Materials and Financials, which have moved from overbought to either oversold or near oversold in the course of only a week. While it’s perfectly normal for sectors to ‘digest’ gains after a big move, those kinds of shifts aren’t particularly normal and suggest a good deal of uncertainty towards the sectors on the part of investors.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Sep 27, 2018

US equity futures are slightly higher this morning as the markets try to recover from yesterday’s post-FOMC swoon, but things are really likely to quiet down shortly after the open this morning when the Kavanaugh hearing kicks off at 10 AM.

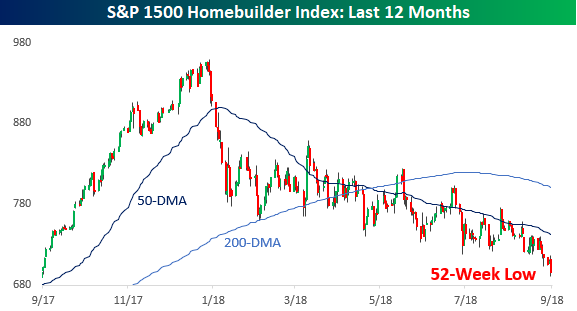

While the broader market continues to trade right near all-time highs, a number of key areas of the market are not only missing out of the party, but they’re at 52-week lows. Exhibit A is the homebuilders (chart below), but along with them, stocks like Whirlpool (WHR), and Bed, Bath, and Beyond (BBY) are also at multi-year lows, while the two ‘generals’ of General Electric (GE) and General Motors (GM) are acting more like ‘privates’.

It’s still earnings off-season, but from the few reports we have seen so far, companies aren’t exactly wowing investors. We first highlighted this in last week’s Bespoke Report, but this week we are seeing the trend continue a bit as just over half of companies reporting managed to exceed their revenue forecasts. Once earnings season comes, they are going to have to do better than that!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.