Nov 15, 2018

It’s been one of the busier days in quite some time for economic data, and relative to expectations, it has been a mixed bag. Jobless Claims came in slightly higher than expected, Empire manufacturing was better than expected while Philly missed, Retail Sales were stronger than expected at the headline level, but a bit weaker underneath the surface, and Import and Export Prices both came in higher than expected. All in all, there was nothing here to put in doubt FOMC Chair Powell’s view Wednesday evening that the US economy remains on solid ground.

In terms of individual stock news, Walmart (WMT) concluded earnings season with an earnings beat and is trading higher, while JC Penney (JCP) had disappointing results and is down nearly 10%. Homebuilders are down across the board this morning after KB Home (KBH) lowered guidance last night and is trading down over 10% and dragging the rest of the group lower in the process.

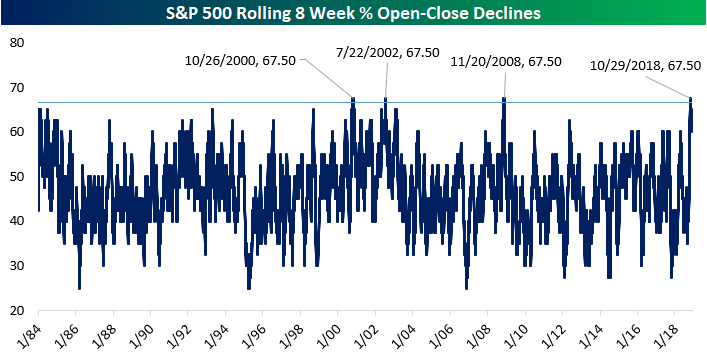

If it feels lately like the market does nothing but go down, well, that’s basically because it’s true. As noted in last night’s Closer report, over the 8 weeks ending October 29th, the percentage of open-close declines was the joint-highest for any period since 1984, with the start and finish of the 2000s bear market and the near depths of the financial crisis the only other periods when stocks declined intraday so frequently. Unfortunately, there’s not a lot to take away from the prior periods in terms of forward returns; one occurred early in a bear market, the other towards the end, and the third right in the middle. What this chart does confirm, though, is how lousy the recent market environment has been for anyone holding equities.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Nov 14, 2018

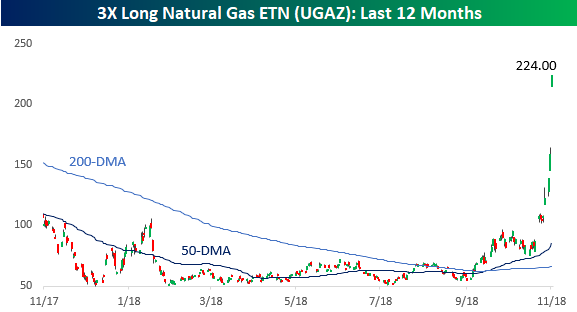

Crude oil prices are trying to recover this morning as Natural Gas prices continue to go bananas. Equity futures are picking up steam to the upside, and CPI came in right inline with expectations.

With the surge in natural gas over the last couple of days and into this morning, one security that has been absolutely on fire over the last week is the Natural Gas Triple Leveraged ETN (UGAZ). While it was trading around $80 per share a week or so ago, it closed yesterday at $158 and is trading above $220 in the pre-market this morning. When you see moves like this in such a short period of time, it’s tempting for some to want to get in on the action.

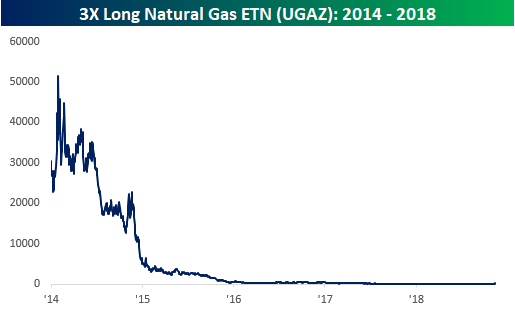

Besides the fact that these leveraged ETNs go down just as fast as they go up, it is important to remember that the way they are structured makes holding them for any extended period of time a sucker’s bet. Just take a look at the long-term chart of UGAZ below. After taking all of the reverse splits into account over the years, of which there were three (1-10, 1-25, 1-5), UGAZ’s price in early 2014 was over $50,000 per share. So, even though the price has tripled in the last two weeks, UGAZ is still down over 99.5% from its high less than five years ago. Next time you hear someone talk about buying one of these ETNs do them a favor and take their money instead.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Nov 13, 2018

It’s a small dent, but US equities are attempting to get back some of Monday’s losses following optimistic news on trade between China and the US as well as positive earnings reports from Home Depot (HD) and Beazer (BZH). Positive openings haven’t been the problem over the last several weeks, though. It is what the market does from the opening to the closing bell that has been the problem! On trade, there’s still absolutely nothing concrete, so it wouldn’t take much to reverse that optimism. Housing-related stocks should get a boost from the HD and BZH news, and if they can’t, that may be an even bigger tell for the market.

Besides providing a good case for why the stock market should be closed on bond market holidays, yesterday’s equity market decline was disheartening from a technical perspective. Last week, bulls were all excited that the S&P 500 traded back above its 200-DMA after a short time below that level. With yesterday’s decline, the stint above the 200-DMA was even shorter. It’s also never encouraging to see a major index fail to hold onto its already downward sloping 200-DMA. If there’s one thing the bulls can hope for it is that yesterday’s drop is the beginning of a second shoulder in an inverse head-and-shoulders pattern. It is Tuesday, so there’s no better time for a turnaround!

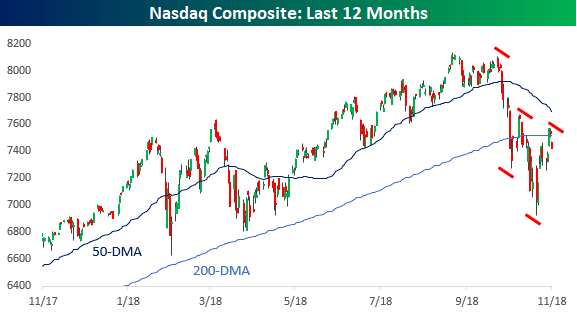

The chart of the Nasdaq isn’t any better, and you could make the case that it looks even worse. Unlike the S&P 500, which rallied back last week to the same levels it hit in mid-October, the Nasdaq actually formed what now looks like a second lower high. Unlike the correction earlier this year, the days of tech offering a port in the storm are done.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Nov 12, 2018

As if the stock market being open on a bond market holiday isn’t bad enough, pre-opening futures are making bulls feel even worse as all three major averages are set to open lower on the day. Futures aren’t down by a large amount, but they are getting progressively worse as the morning goes on. One catalyst for the weakness is a profit warning from iPhone supplier Lumentom (LITE), which cited a decline in orders from “one of our largest Industrial and Consumer customers” as the reason for the shortfall. Outside of that, though, there is little data on the schedule and the bond market is closed for Veterans Day, so don’t expect much in the way of major news to come.

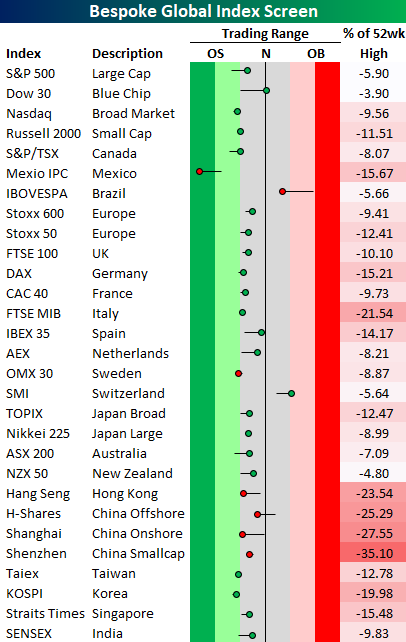

Although higher on the week, US equities finished Friday with a thud leaving the S&P 500 well below its 50-day moving average and down just under 6% from its recent highs. While equities remain in a bit of a funk, they have plenty of company. As shown in the graphic below, of the 29 major global indices highlighted in our Global Index screen, all but two (Brazil and Switzerland) are below their 50-day moving average, and the average distance from recent 52-week highs is over 13%. It may be bad here, but it could be worse. Like the US, most indices aren’t quite oversold, but they are also below their 50-DMAs, so it’s a little bit of a holding pattern in search of a catalyst.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Nov 9, 2018

Equity futures and commodities were weak heading into the 8:30 PPI report and picked up steam to the downside after a much stronger than expected PPI report for the month of October (0.6% vs 0.2%). In fact, it was the strongest report relative to expectations since the initial release of the January 2017 report last February.

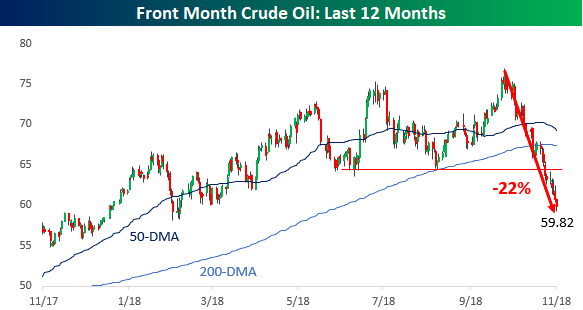

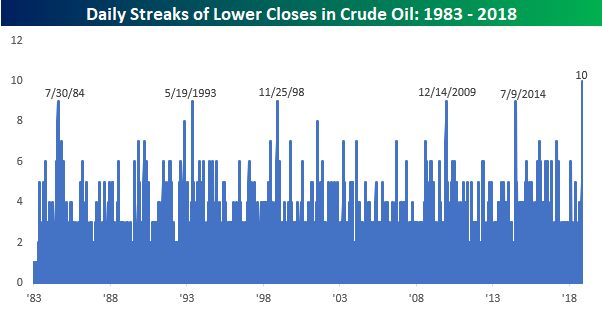

As mentioned above, WTI crude is trading below $60 today and headed deeper into bear market territory with a decline of 22% from the recent peak. As the chart below illustrates, it’s been practically a straight drop lower for crude oil. Recent trading, in fact, has been so one-sided that crude is on pace for its 10th straight day of declines. That’s the longest streak of consecutive declines, not in the last five, ten, or twenty years, but at least 35 years! Going back to 1983, there has never been a streak of more than 9 straight days where crude oil traded down on the day. While increased supplies are putting downward pressure on prices, is this the type of chart you see when the economy is overheating?

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Nov 8, 2018

Markets are extremely quiet this morning following Wednesday’s fireworks. There’s still been a number of big earnings reports from the likes of Qualcomm (QCOM), News Corp (NWSA), and Square (SQ) to name a few. Jobless claims came in at 214K, which was right around expectations of 213K. At 2 PM we will hear from the FOMC where traders are hoping that the statement will imply a slightly less hawkish tone.

Also, we just released the latest episode of our Bespokecast featuring Patrick Wyman, who hosts the popular podcast Tides of History. Make sure to check it out. It’s a bit different from some of our prior episodes, but you’ll definitely like it!

Bespokecast Episode 27 featuring Patrick Wyman

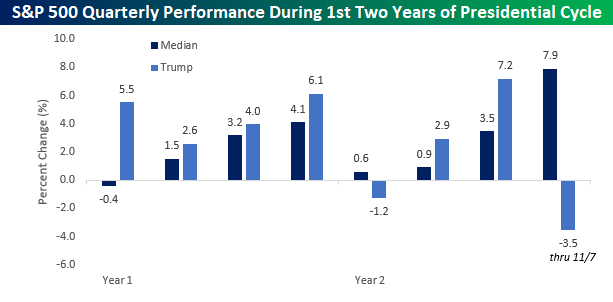

With all the talk about market performance around and after midterm election years, we wanted to provide a quick comparison of the S&P 500’s quarterly performance during the first two years of President Trump’s tenure to the media quarterly returns of the S&P 500 during the first two years of the four-year Presidential cycle. Looking at the chart, while there have been a number of quarters where returns have been similar under Trump to the historical norm, as one might expect, there have also been some wide disparities. This quarter, for example, the S&P 500 is down 3.5% in a quarter where it has historically rallied 7.9%

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.