It’s been one of the busier days in quite some time for economic data, and relative to expectations, it has been a mixed bag. Jobless Claims came in slightly higher than expected, Empire manufacturing was better than expected while Philly missed, Retail Sales were stronger than expected at the headline level, but a bit weaker underneath the surface, and Import and Export Prices both came in higher than expected. All in all, there was nothing here to put in doubt FOMC Chair Powell’s view Wednesday evening that the US economy remains on solid ground.

In terms of individual stock news, Walmart (WMT) concluded earnings season with an earnings beat and is trading higher, while JC Penney (JCP) had disappointing results and is down nearly 10%. Homebuilders are down across the board this morning after KB Home (KBH) lowered guidance last night and is trading down over 10% and dragging the rest of the group lower in the process.

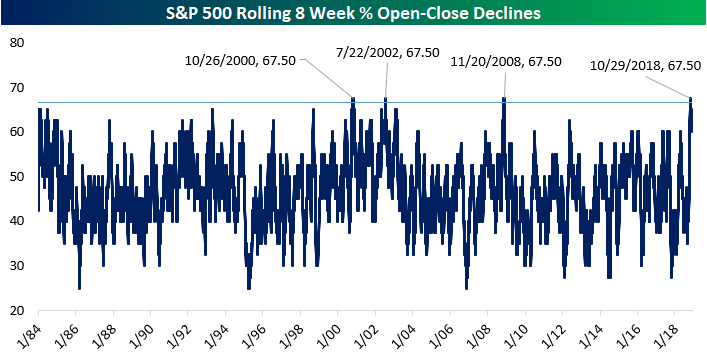

If it feels lately like the market does nothing but go down, well, that’s basically because it’s true. As noted in last night’s Closer report, over the 8 weeks ending October 29th, the percentage of open-close declines was the joint-highest for any period since 1984, with the start and finish of the 2000s bear market and the near depths of the financial crisis the only other periods when stocks declined intraday so frequently. Unfortunately, there’s not a lot to take away from the prior periods in terms of forward returns; one occurred early in a bear market, the other towards the end, and the third right in the middle. What this chart does confirm, though, is how lousy the recent market environment has been for anyone holding equities.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.