Dec 21, 2018

The week that is. As for the market decline, it’s another story as to when that will end, but no matter how you slice it, stocks are trading at extremely oversold levels similar to short-term declines we saw in early 2016, August 2015, August 2011, and before that 2008. Today, equity futures are slightly higher, but is anyone going to put any trust in them at this point? We just had a big release of economic data and for the most part, the reports came in roughly in line to below expectations, but nothing was that far off the mark. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/21/18

We have two quick charts to highlight this morning. The first is the rolling 5-day change in the S&P 500 over the last ten years. As of yesterday’s close, the S&P 500 was down 6.9% over the prior five trading days. How does that stack up to the past? You may be surprised to see that back in February we actually had a sharper drop over five days. Overall, there have only been six other periods in the last ten years where the S&P 500 fell this much or more over such a short period. What’s unique about the most recent period relative to earlier this year is that the period of selling was much quicker back then. The current period has seen a lot more consistency in terms of selling, similar to 2011.

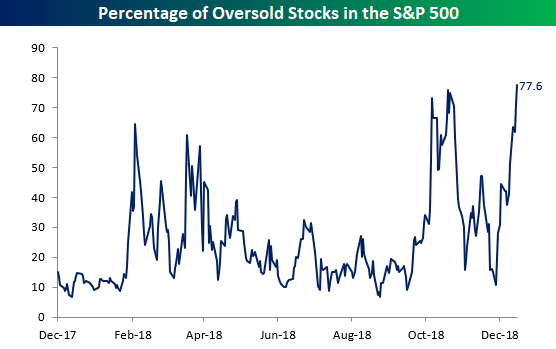

The next chart shows the percentage of oversold stocks in the S&P 500 (trading more than one standard deviation below their 50-day moving average). The current level of 77.6% is now the highest level in well over a year. In fact, you have to go back to January of 2016 to find a higher reading.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 20, 2018

Equity futures are trading modestly lower this morning, and based on the market’s inability to hold on to any early gains anyway, maybe it’s a good thing that we’re starting out a little weaker. In case you missed it yesterday, the S&P 500’s negative reversal from an intraday gain of 1.5% to a decline of over 1.5% on the day was pretty monumental. The last time it happened was in February 2009! In economic news, Jobless Claims and the Philly Fed Manufacturing index both missed expectations with the Philly index hitting its lowest level since August 2016. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/20/18

Here’s a doozy for you and something not many would have expected back in January. Over the last 12 months, long-term Treasuries are now outperforming equities! The chart below is from the second page of today’s Morning Lineup, and it shows the relative strength of the S&P 500 versus long-term treasuries over the last year. When the line is rising, it indicates equities are outperforming and vice versa for a falling line. After outperforming Treasuries by a wide margin as recently as September, all of that outperformance has now been erased and equities are now underperforming!

Looking more at the short-term picture, in the table below we show all Fed days since 1994 where the S&P 500 declined 1%+. On the day after 1%+ down Fed Days for the S&P, the index saw an average next-day gain of 0.10% (median +0.50%), and an average next-week gain of 1.14% (median 0.73%). Following all other Fed Days, the S&P has averaged declines over the next day and week, so usually, we see a modest bounce after big down Fed Days.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 19, 2018

US stocks are looking to start the day higher but given the inability of the market to hold onto gains in recent days, no rally, not even in December, is safe these days. Obviously, the main draw for today will be the FOMC rate decision early this afternoon. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/19/18

In the past, we have referred to Fed Ex as a bellwether for the state of the US and global economy, so it was only fitting that the day before the “most important” Fed decision of the year, the company reported Q3 earnings. Unfortunately, the stock is trading down sharply on the results, and if it finishes today where it is trading in the pre-market, it will be FDX’s worst earnings reaction day in over five years based on the data from our Earnings Screener.

After listening to the company’s conference call last night, FDX’s view on the state of the global economy is not particularly positive and should give pause to anyone who thinks the global economy is just humming along fine. Below we have included a number of key quotes from the call. Reading through the commentary, it’s clear that while the US economy remains solid, global trends are weakening at an increasing state. The key quote is the last one, where FDX management pins the blame for economic weakness on “bad political choices.” Not just in the US, but around the world. The question Fed policymakers must contend with is, how long the US can continue to keep itself insulated from global trends.

“Some of the largest economies in Europe are experiencing weakness.”

“World trade slowed in Q3 to just 3.5% compared to 5.3% in Q3 2017. Leading indicators point to positive, but even slower trade growth near-term.”

“Economic growth in the UK has slowed sharply since July.”

“The peak for global economic growth now appears to be behind us.”

“China’s economy has weakened due, in part, to trade disputes.”

“Our international business, especially in Europe, weakened significantly”

“FedEx is experiencing strong growth in the US, where the economy remains solid.”trade will continue to grow.”

“I’ll just conclude by saying most of the issues that we’re dealing with today are induced by bad political choices, making a bad decision about a new tax, creating a tremendously difficult situation with Brexit, the immigration crisis in Germany, the mercantilism and state-owned enterprise initiatives in China, the tariffs that the United States put in unilaterally. So, you just go down the list, and they’re all things that have created macroeconomic slowdowns. The good news is, with a change in policy, they could turn it around pretty quick, too. So fundamentally, we think trade will continue to grow.”

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 18, 2018

US stocks are looking to start the day higher in what bulls are hoping is a turnaround Tuesday. After two straight daily declines of nearly 2%, you would expect at least some sort of bounce. After all, stocks can’t go down every day, can they? Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/18/18

Heading into today, the S&P 500 is now down 7.8% for the month of December. If the month were to end today, it would go down as the worst month for the S&P 500 since May 2010, so clearly, these kinds of declines are not typical of bull markets. Furthermore, for the month of December declines of this magnitude are practically unheard of. The last time the S&P 500 had a weaker MTD December performance through the close on 12/17 was in 1931!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 17, 2018

After the fourth down week in the last five, US equities are looking lower once again this morning and the magnitude of the implied decline is getting worse as the opening bell nears. Even though it’s only Monday, the focus is already on Wednesday’s FOMC meeting, even more so now that Stanley Druckenmiller and former Fed Official Kevin Warsh have urged Powell and Company to pause its tightening ‘blitz’ in a WSJ op-ed.

Today, we’ll get reads on Empire Manufacturing and Homebuilder sentiment for the month of December. Last month’s homebuilder sentiment report showed the largest decline since February 2014, so that will be an important release to watch for signs of a bounceback or further deterioration. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/17/18

Plain and simple, the first half of December has been awful. Normally one of the strongest months of the year, the S&P 500 has dropped over 5% so far this month putting it on pace to be one of the worst Decembers in the post WWII period. Looking back over the last 25 years or so, it hasn’t been uncommon to see weakness in the first half of December but not declines of 5%+! Going back to 1945, there have only been two other months where the S&P 500 was down 5% or more through the close on 12/14 – 1980 (-8.03%) and 2002 (-5.00%).

So is it time to cancel Christmas? The chart below shows the performance of the S&P 500 in the period covering the close on 12/14 through the close on Christmas Eve. Since 1945, the S&P 500 has seen an average gain of 0.82% (median: 0.70%) during this period with positive returns 63% of the time. And how about the two prior years highlighted above where the S&P was down over 5%? In 1980, stocks really rallied leading up to Christmas with a gain of 5.15%, while in 2002, the rebound was a more muted 0.34% (at least it stopped going down).

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 14, 2018

The phrase of the day around the world heading into 8:30 was weak economic data, as a bevy of weaker than expected economic data points flooded the headlines. The just-released November Retail Sales report, however, tried to buck that trend as it not only came in higher than expected, but last month’s report was also revised higher! There’s still more to come, though, with Industrial Production and Capacity Utilization at 9:15 and Flash PMI from Markit at 9:45, so hopefully that trend can continue (but not too strong!). Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/14/18

Back in late September when the S&P 500 peaked and started to correct, growth stocks were hit hard reversing their trend of outperformance from earlier in the year. The culprit? Concerns over tighter FOMC policy. By mid-November, the S&P 500 Growth Index had given up about half of its YTD outperformance relative to the S&P 500 Value since the start of the year. Over the last three to four weeks, though, growth stocks have regained some steam with a strong three weeks of relative outperformance. This latest leg lower for the group has come as concerns over broader economic growth have increased causing the market to rethink expectations for the pace of rate hikes going forward.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.