Dec 13, 2018

Futures have been all over the place this morning on headlines coming out of China (what else is new) and the latest ECB rate decision. In the US, jobless claims are due out shortly, and investors are hoping the recent string of increases reverses. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/13/18

With all the wild swings we have seen, the US equity market has essentially been trapped in a box over the last several weeks, albeit a relatively large one ranging from 2,600 to 2,800. Until stocks break out of that range in either direction, it’s hard to read these day to day moves as anything more than noise. Right now, the S&P 500 is trading a lot closer to the bottom end of that range than the lower end, so at this point, there’s less room for error.

Perhaps one clue of which way the market will break is to watch the semis. They led the broader market lower, and they too have been pretty much boxed into a range for the last several weeks. Like the S&P 500, the semis are also trading a lot closer to the bottom end of the range than the top.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 12, 2018

For the second day in a row, US equities are poised to open higher on positive trade headlines regarding the US and China. Hopefully today these gains can hold. The dollar is down, once again failing to break out higher from the top of its recent range, while interest rates are starting to firm up a bit with 1-2 bps of yield gains across the curve and a bias towards steepening. Crude oil is up a healthy 1.8% with gasoline rallying as well. Since OPEC announced output curbs last week, things have been mixed but generally positive for Texas Tea, with products basically staying on top of the raw oil price

Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/12/18

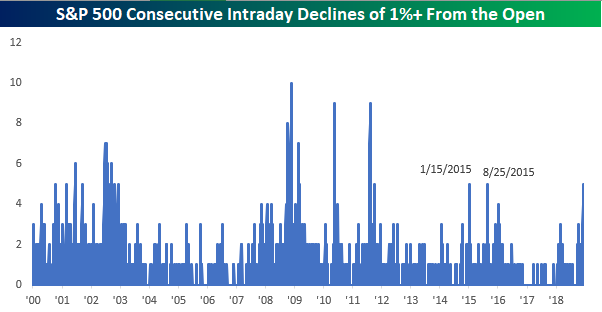

As mentioned above, the S&P 500 has had trouble lately holding onto gains. In fact, yesterday was the fifth straight trading day that the S&P 500 traded down 1% or more from its opening level at some point in the trading day. That doesn’t tend to happen often, and the last time we saw a similar string of consecutive intraday selloffs from the open was back in August 2015 when China devalued. We’re still far from really extreme levels in this streak, though. Back during the financial crisis, we saw ten straight days of similar intraday selloffs. Let’s hope we don’t get to that point.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 11, 2018

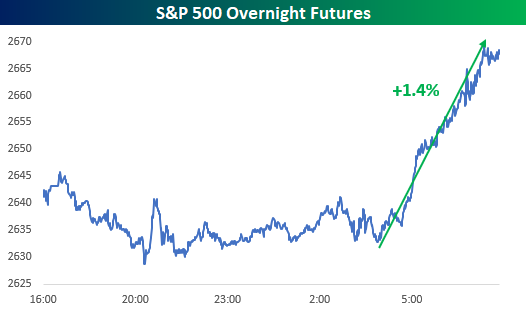

How many times can equity futures around the world rise and fall on the same headlines? We’re learning that lesson in real time these days, as US futures are rallying today on reports that China will cut tariffs on imported US autos from 40% down to 15% and that officials from both countries continue to negotiate despite the arrest of Huawei’s CFO in Canada. Believe it or not, futures were lower for most of the overnight session before getting a real boost right around 4 AM.

Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/11/18

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 10, 2018

Things aren’t as bad as they were when futures first opened Sunday evening, and US equities are now looking to kick off the week on a modestly positive note this morning. After the S&P 500 and Nasdaq just had their worst week in over six months while the Russell 2000 had its biggest decline since January 2016, one could say that we were at least due for some gains. Keep in mind too that all that weakness last week came in the span of just four days too! Global equities are mostly in the red as Asian markets traded down over 1%, and European markets are down just modestly as they, like US futures are off their lows. Treasuries are selling off slightly this morning as the 10y3m curve steepens slightly but remains at an exceptionally flat level of less than 50 bps. Meanwhile, crude oil saw a quick 1.5% sell-off at right around 4:30 New York time which was blamed on continued worries that the US/China trade war will sap demand.

Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/10/18

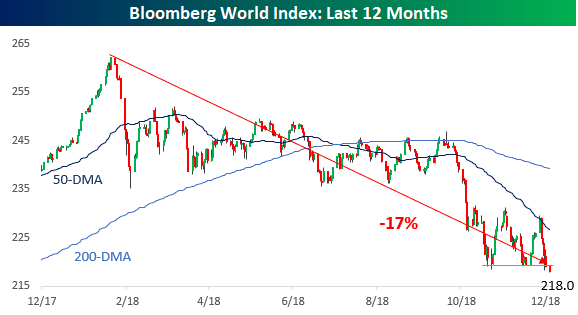

We’ve discussed numerous times how many international equity benchmarks are already in their own bear markets, but because the US has held up considerably better than global peers and its overall weighting in the global equity pie is so large, it has been able to keep global equities as a whole outside of bear market territory…for now. This morning, global equities are moving one step closer to bear status as the Bloomberg World equity index appears to be breaking below support. The index is now down 17% from its highs earlier in the year, so a few more days like we saw last week, and global equities will have lost one-fifth of their total market value.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 7, 2018

Treasuries continue to catch a bid this morning as investors don’t want to stick their necks out on the risk curve ahead of today’s jobs report. Given all the volatility in markets and other events swirling around recently, it seems as though this morning’s report has taken a backseat, and let’s hope that it is uneventful enough to stay that way! In a speech at a housing conference in DC yesterday, FOMC Chair Powell continues to see the economy humming along and described the labor market as “very strong.” The market is only hoping that it’s not too strong. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/7/18

Yesterday’s ‘moral victory’ rebound for US equities was impressive and most so in the Nasdaq which actually finished the day in the green. The index still has a lot to prove from a technical perspective, and the first task at hand is to break the string of lower highs. The most recent of those was at 7,490, which is just below the 200-day moving average. What is encouraging, though, is the fact that the index did make a higher low yesterday and could be in the later stages of an inverse head and shoulders pattern. We don’t put a lot of weight into these formations, but many do, so it’s important to at least be cognizant of it.

Also positive is the fact that the Nasdaq’s leading group for much of this year-Software & Services- has also shown signs of stabilizing. After last week’s higher high just above the 50 and 200-DMAs, the group managed to make a higher low in yesterday’s trading. That’s definitely worth watching.

Finally, while not related to the Nasdaq specifically, homebuilder stocks also look to be carving out a bottom. The group has also managed to make a higher high and two higher lows in the last few weeks. In addition to that, the fact that PulteGroup (PHM) just announced a dividend increase indicates at least some level of confidence on the part of one company in the group. We would note that back in the early stages of the housing crisis, the last homebuilder dividend increase was all the way back in August 2006.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Dec 6, 2018

At least US stocks couldn’t go down yesterday. Equities are looking to open the day sharply lower on new concerns regarding the US-China relationship. Not helping matters is the fact that the latest round of US economic data that released this morning was disappointing as ADP Private Payrolls came in weaker than expected while Jobless Claims were a little higher than expected. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and detailed analysis and commentary:

Bespoke Morning Lineup – 12/6/18

The last thing you want to see the day after a 3%+ decline in the S&P 500 is another 1%+ decline at the open the following day, but that’s what today’s open is shaping up to be. In looking at the chart of the S&P 500 below, the fact that we were unable to hold above 2,800 for a third time on Monday is certainly a disappointment, but this latest swoon to the downside hasn’t violated any important levels as of yet. Even with today’s implied open, we still won’t be making any sort of lower low. That doesn’t mean things will not get worse going forward, but we just wanted to provide some perspective of where things stand now. As always, we’ll be watching some of our key internal indicators for any further clues.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.