Sep 28, 2018

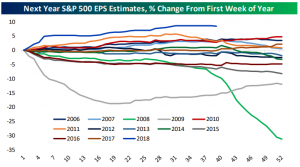

While the economy is on good footing and the overall backdrop is reasonably positive for stocks, there’s reason to be a bit cautious. EPS estimates have been rising sharply this year relative to history, and that process may be completing. While it’s not certain that the bar being set by analysts is too high, stocks have gotten a tailwind from stronger earnings estimates all year; if that process goes into reverse, equity market gains would require higher valuation. While possible, this late in the economic cycle and given higher interest rates, it would be prudent to not rush to expectations of the same climb in valuations that we saw earlier in this bull market.

We’ve just published our latest weekly Bespoke Report newsletter, which is available to subscribers across all three of our membership levels. Sign up here to read the report.

To get up to speed on our thoughts regarding the market’s direction going forward, choose any membership option and access this week’s full Bespoke Report newsletter after signing up! You won’t be disappointed. Some of the topics discussed in this week’s report include:

- Why chaos in the headlines doesn’t mean chaos for stocks

- US economy update

- Check in Europe: Italian chaos, slow inflation, but firm credit growth

- Recent global trade and industrial production volumes

- Breakouts in APAC equity indices and some improvements in EM

- Weak earnings reactions since the end of the last earnings season

- Chinese economic data recap

- Review of the Fed rate hike this week and current FOMC thinking

- Improving credit spreads despite high debt-to-GDP levels

- Focus on homebuilders: versus housing data and valuations

- Model Growth Portfolio update

Sep 21, 2018

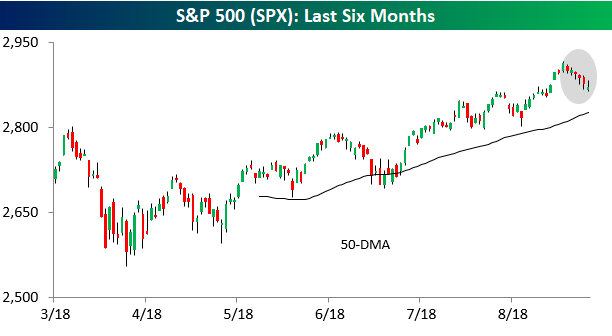

School has been back in session for less than a month now, but the S&P 500 already had its first test of the semester and came out passing with flying colors. After breaking out to new highs at the end of August, the S&P 500 pulled back in early September and found support right at its prior highs from January. After holding that level, the S&P 500 has now traded higher on eight of the last ten trading days, rallying to higher highs. It doesn’t get much more textbook than that!

Heading into the week,the DJIA was the only major US index that had yet to take out its January high, but that changed this week as the index closed out the week with four straight days of gains. While most other indices ran into resistance on their first attempts to take out their highs from January, the DJIA just buzzed right through it.

We’ve just published our latest weekly Bespoke Report newsletter, which is available to subscribers across all three of our membership levels. Sign up here to read the report.

To get up to speed on our thoughts regarding the market’s direction going forward, choose any membership option and access this week’s full Bespoke Report newsletter after signing up! You won’t be disappointed. Some of the topics discussed in this week’s report include:

- Index and sector breadth checkup

- US economy update

- What major indicators say about the odds of a recession

- How recent earnings report stack up

- An ‘Industrious’ rally

- Commodities and the Materials sector

- Mutual fund and ETF flows

- High yield spreads

- Rotational forces

- Model Growth Portfolio update

Sep 7, 2018

The End of Summer Hangover. The end of Labor Day weekend, when schools are back in session and summer starts to wind down, is always a tough time of year. After a summer of nice weather, swimming, hiking, outdoor sports, and hopefully even a vacation, Tuesday morning after the three-day Labor Day weekend can be rough. This year was no exception, and it was reflected in the performance of US and global equity markets.

Take a look at the chart below. For six straight trading days now, the S&P 500 had a lower intraday high and lower intraday low than the prior day’s levels. That type of consistent selling with zero in the way of buying doesn’t happen very often. To find the most recent occurrence, you have to go all the way back to May 2012, and since 1982, it has only occurred eight other times.

We’ve just published our latest weekly Bespoke Report newsletter, which is available to subscribers across all three of our membership levels. Sign up here to read the report.

To get up to speed on our thoughts regarding the market’s direction going forward, choose any membership option and access this week’s full Bespoke Report newsletter after signing up! You won’t be disappointed. Some of the topics discussed in this week’s report include:

- Buyers Strike

- International/Domestic Dichotomy

- FAANGed Up

- Bear Market in Emerging Markets

- Economic Review

- Years Like 2018

- Back to School Review

Aug 24, 2018

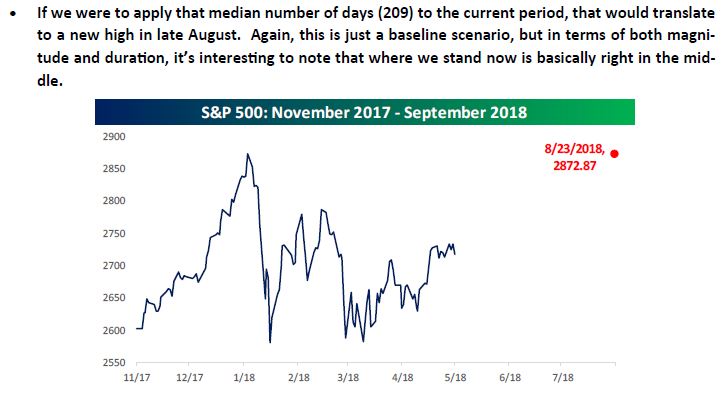

In our Bespoke Report dated 5/25/18, we provided the following chart and comments in our discussion of market corrections modeling that the S&P 500 would close at an all-time high again on 8/23/18. With the S&P 500 finally closing at an all-time high on Friday, we ended up being off by a day, but we’ll take it!

We’ve just published our latest weekly Bespoke Report newsletter, which is available to subscribers across all three of our membership levels. Sign up here to read the report.

To get up to speed on our thoughts regarding the market’s direction going forward, choose any membership option and access this week’s full Bespoke Report newsletter after signing up! You won’t be disappointed. Some of the topics discussed in this week’s report include:

- Comparison between now and 2000

- Housing starts to roll over

- The US economy and the global slowdown

- Decade-low readings in the yield curve

- Some attractive Financial sector stocks

- Market performance leading up to the mid-terms

- High yield breaks through a key level

- Sector breadth

- An exceptionally consistent Spring and Summer

- US vs ROW for the rest of year

- New highs- what now?

- Dividend Model Portfolio Update