Mar 30, 2022

While the index turned lower today on weaker breadth, the recent rally for the S&P 500 has come on strong breadth resulting in the 10-day advance/decline line to surge to some of the highest readings on record. Monday and Tuesday saw 99th percentile readings in the 10-day A/D line and even after the decline today, the current reading remains in the 96th percentile. At Monday’s high, the 10-day AD line reached the most elevated level since October 2020. On a sector level, in the past week Financials, Health Care, Materials, Real Estate, and Tech also all saw 99th percentile readings in their own 10-day advance-decline lines.

In the matrix below, we show the average forward performance of the S&P 500 broken down by the percentile range that the index’s 10-day AD line is in. Generally, lower readings in the 10-day AD line have been followed by stronger returns whereas higher readings have been followed by weaker returns. That is, except for the most elevated readings. Readings in the upper decile have actually been followed by more consistently positive and stronger than normal average returns for the S&P 500. In other words, strong breadth is typically a more negative signal for the S&P 500 going forward, but an extremely strong breadth reading has actually been positive.

Mar 30, 2022

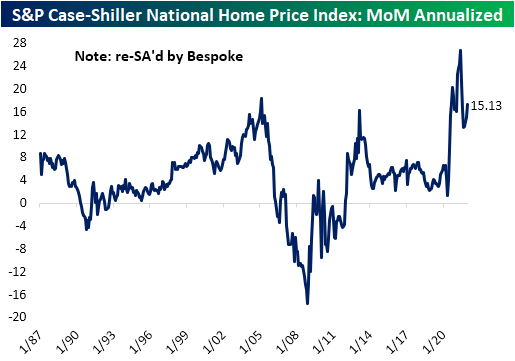

In last night’s Closer, we discussed recent trends in apartment and home prices. Case-Shiller data reported yesterday showed home price appreciation ramped back up in December and January with 15% annualized growth. That is a much slower pace compared to the 26% annualized appreciation back at the post-pandemic peak last spring but is still extremely high by any standard.

That appreciation has not been evenly felt across the country though. Since home prices inflected higher in the middle of 2020, four metros have been appreciated by more than 40% while Washington, Chicago, and Minneapolis are up at about half that price. In total, national home prices have risen almost 30% since the surge began or 18% annualized. It is worth noting that this data does not include the massive surge in mortgage rates that started at the end of last year which means that it is very unlikely that housing demand (and therefore home prices) can continue to run at such extreme levels given the huge hit to affordability brought on by higher rates.

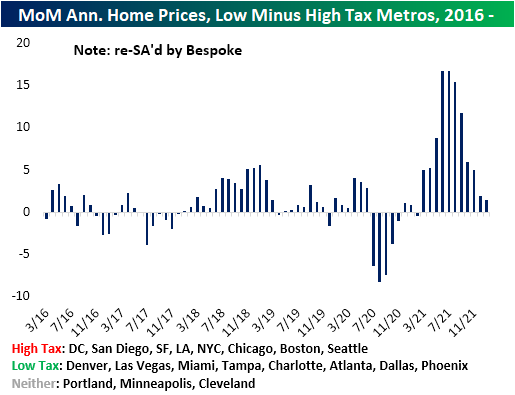

Taking a more granular look at various metros, the huge surge in home prices had been more pronounced in lower-tax states relative to higher-tax states. But that trend has been unwinding. Click here to view Bespoke’s premium membership options.

Mar 30, 2022

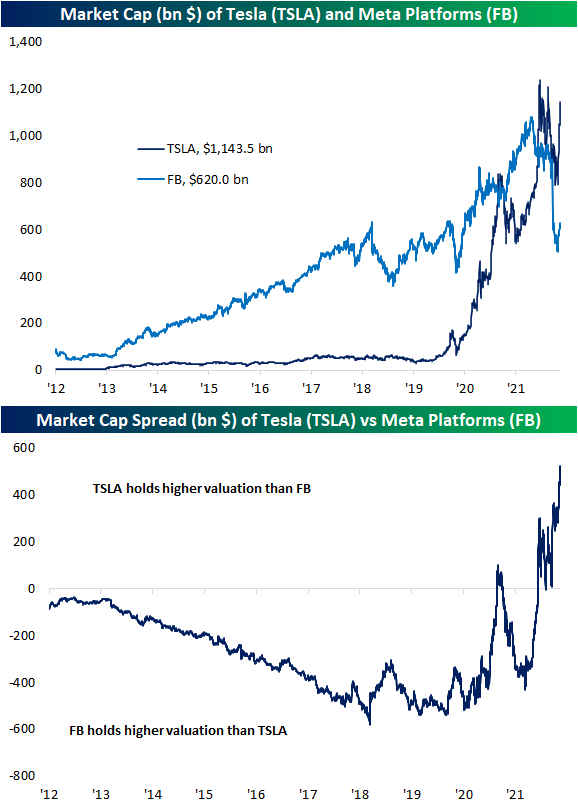

Along with the rest of the market, two of the largest stocks, Tesla (TSLA) and Meta Platforms (FB), have been on substantial rallies this month. In the case of TSLA, the stock is roughly 10% away from its 52-week high after rising ~45% since its late February low. Facebook/Meta Platforms, on the other hand, peaked back in September with a massive drop in response to the last earnings report in February being the pinnacle of those declines. Losses continued until it put in a low on March 14th. Since then, the stock has rallied 22% but that still leaves it down over 40% from its 52-week high.

As shown below, Facebook had a much larger market cap than Tesla throughout the 2010s, but the 2020s have seen Tesla take the lead in a big way. While both have been members of the “trillion dollar market cap” club at various points in time, only Tesla holds that distinction right now. At the moment, Tesla’s market cap sits at nearly $1.15 trillion, while Facebook is just above the $600 billion level.

Below we show the ratio of the market caps of TSLA and FB. As shown, the massive distancing of the two stocks’ market caps means the value of Tesla (TSLA) is closing in on being worth 2 whole Facebooks. Click here to view Bespoke’s premium membership options.

Mar 30, 2022

Mortgage rates continue to hone in on 5% as the reading on the national average of a 30-year fixed-rate mortgage via Bankrate.com hit 4.89% yesterday. That puts mortgage rates at the highest level since the spring of 2011. The extremely rapid 1.64 percentage point rise in rates over the past year also now stands as the largest year over year jump going back to at least the late 1990s per this data.

Given rates continue to climb, refinancing looks less attractive. The weekly reading on refinance applications from the Mortgage Bankers Association (MBA) has fallen over 14% two weeks in a row bringing the index to the weakest level since May 2019.

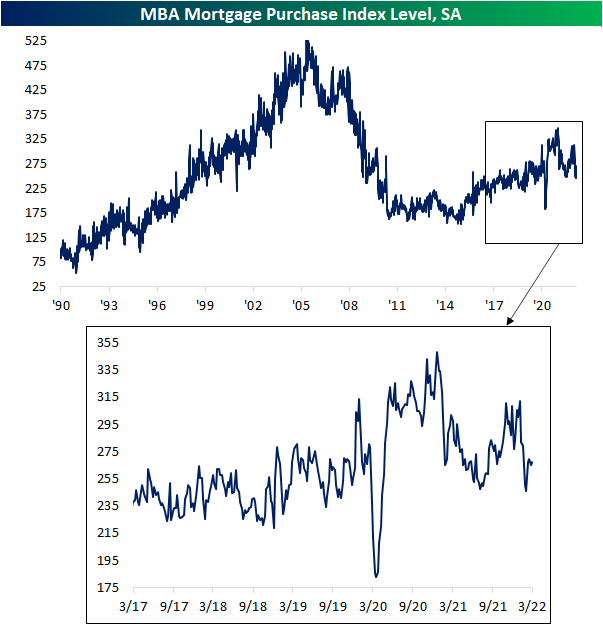

Purchase applications have also fallen to the low end of the post-pandemic range, though, there was a rebound this month with only last week seeing a decline followed by a minor uptick this week. While peaked, the current level of purchase applications is relatively healthy compared to other post-housing crisis years.

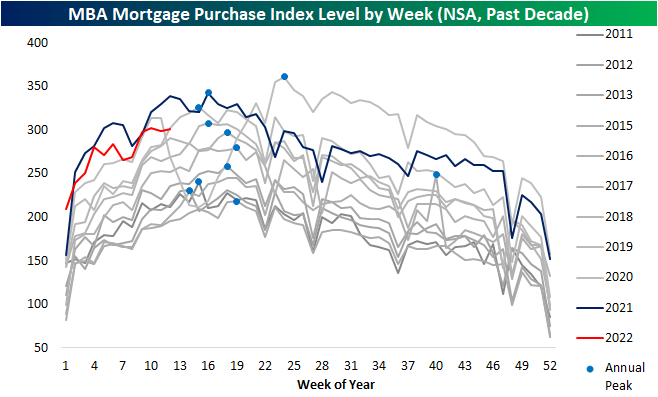

Taking a slightly different look at the data, in the chart below we show the non-seasonally adjusted purchase indices over the past decade. The first few months of the year tend to see purchases rise before hitting an annual peak (blue dots in chart below) sometime in mid-spring. Within the next several weeks, that seasonal peak is likely to be put in place. As mentioned above, while purchases are still running at the high end of the past decade, most of this year has run below last year’s pace, and that is likely to continue if not become more pronounced given the hit to affordability via higher rates and low inventories.

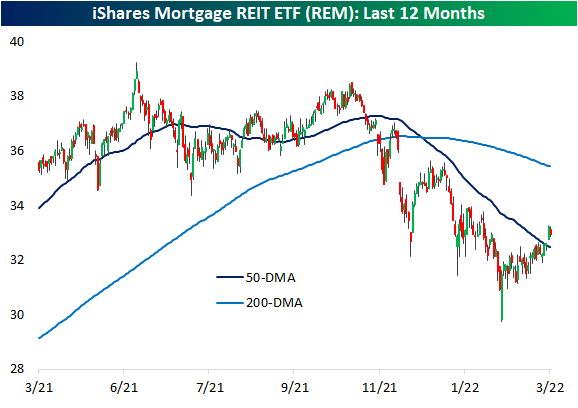

As for housing adjacent stocks, two ETFs have seen very different developments recently. As shown below, the iShares Home Construction ETF (ITB) set 52-week lows last week and with this week’s rebound it only hovers slightly above those levels. Mortgage REITs, proxied by the iShares Mortgage REIT ETF (REM), meanwhile, have actually been rallying off of 52-week lows set further back in February. That rally has broken the downtrend of the past several months and brought REM back above its 50-DMA. Click here to view Bespoke’s premium membership options.

Mar 29, 2022

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of price action across assets including some commentary on the 2s10s inversion. We then provide a recap of the 7 year note auction. We follow up with a dive into rental prices and home prices. We then take a look at consumer confidence data from the Conference Board and Morning Consult, before finishing with a look at today’s JOLTS figures.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!