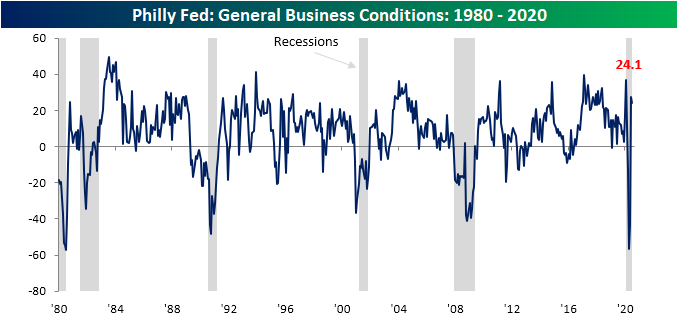

Philly Fed Continues to Rebound

Following up on yesterday’s New York Fed reading on the manufacturing sector, this morning we got the manufacturing numbers from the neighboring Philadelphia Federal Reserve bank region. Similar to the Empire Fed’s reading for six months out, the Philly Fed’s index for General Business Conditions pulled back a bit in July falling to 24.1 from 27.5 in June. In absolute terms, that was the least volatile one month swing in the index since November of last year. Additionally, although it indicates a slower rate of improvement in July than June, it still indicates that the region’s manufacturing sector expanded for a second consecutive month after three months of contractionary activity.

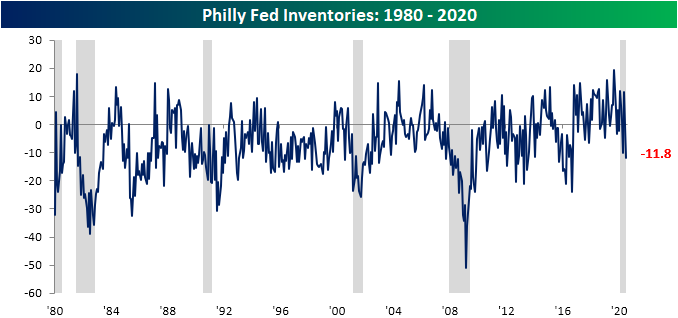

Although the headline number fell in July, the internals paint a much more positive picture. Almost every category is now showing an expansionary reading with the exception of Inventories and Delivery Times, though both of those in contraction is not necessarily negative. Granted negative readings of these two, as well as a sizeable drop in Shipments, did contribute to the weakness in the July headline number.

This month’s release indicated solid overall demand with New Orders surging to 23 from 16.7 last month. Unfilled Orders also rose; moving back into expansion territory after four months of contraction. Meanwhile, Shipments were down 10 points to 15.3, but that is still a firmly expansionary reading.

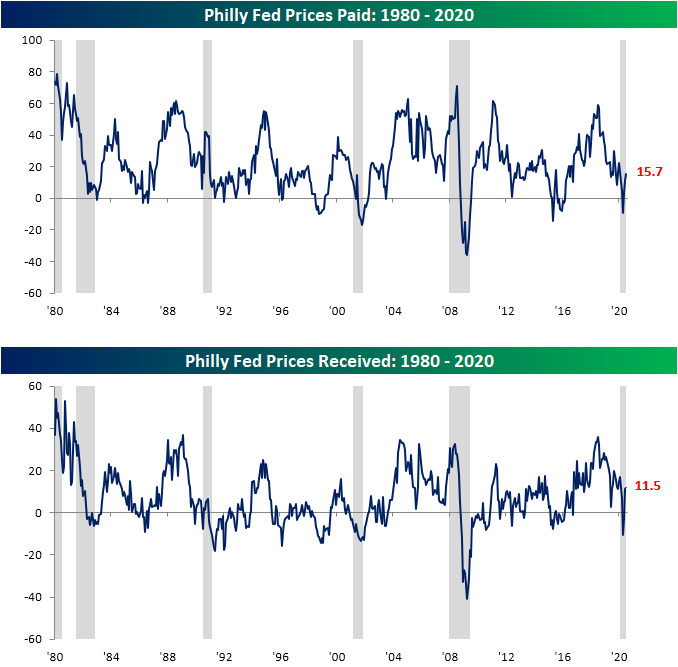

In addition to the strong levels of those indices, respondents reaffirmed the strength in demand by reporting higher prices for the second month in a row in terms of both prices received and paid.

As previously mentioned, both Delivery Times and Inventories showed contractionary readings this month, but that again is not necessarily a bad thing. The Philly Fed’s index on delivery times has fluctuated between positive and negative readings in recent months while other Federal Reserve regions have seen their equivalent readings surge to extremely elevated readings (albeit lower more recently) pointing to supply chain disruptions and longer lead times. The tip into negative territory for the Philly Fed’s index of Delivery Times indicates shorter delivery times and potentially some further normalization in supply chains. Additionally, the index for Inventories fell to its lowest level since September of 2016. That indicates large inventory drawdowns which reasonably can be evaluated as a result of a pick up in demand given the increase in other areas of the survey.

As with yesterday’s Empire Fed report, one of the major highlights of this month’s Philly Fed report was the massive increase in readings on employment. The index for Number of Employees and Average Workweek were the categories to see the biggest increases in this month’s survey returning to positive territory. For these two respective indices, this month’s gains were also some of the largest of all reports since the beginning of the survey. In fact, for both indices, there have only been two months with higher monthly increases. For both indices, one of those months was this past May’s report. As for the other month, the other larger monthly gain for the index for Number of Employees was May of 1975 and for Average Workweek it was June of 1970. These huge jumps also bring both indices into the upper 90th percentiles of all readings. In other words, Philly area manufacturers seem to have not only brought people back to work but also are returning to longer workweeks. Click here to view Bespoke’s premium membership options for our best research available.

B.I.G. Tips – Retail Revival Remains

After months of being cooped up in their homes, Americans were once again out and spending in June. Retail Sales for the month of June were expected to rise by a strong 5%, but the actual reading came in much stronger at 7.5% on the headline reading and modestly less than that ex Autos and ex Autos and Gas. In addition to June’s strong headline number, May’s reading was also revised higher at the headline level but moved lower after taking out the impacts of Autos and Gas.

It’s no doubt been a whirlwind four months for retail sales. After the two worst monthly reports in March and April, May and June have followed up with record m/m increases. As shown in the chart, even though June’s reading of 7.5% seems like a pretty big step down from May’s record reading, it was still the second strongest m/m change in the history of the report.

For anyone with more than a passing interest in how the COVID outbreak is impacting the economy, our monthly update on retail sales is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!

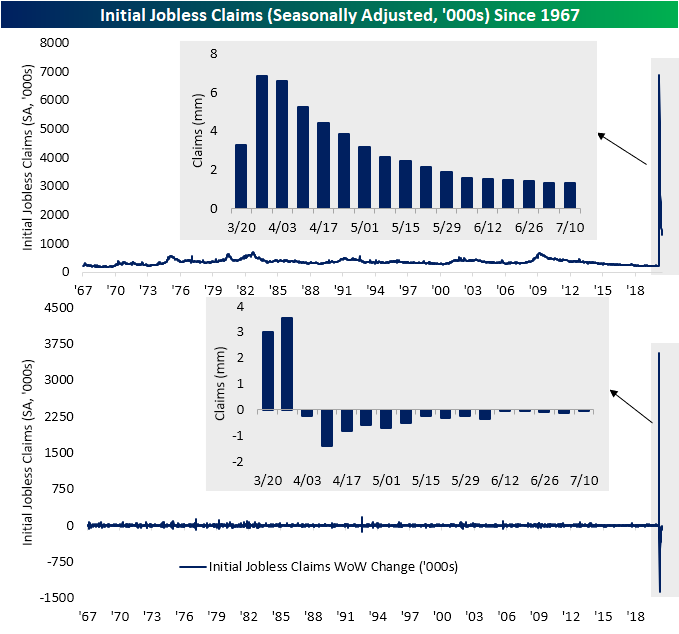

Muddled Jobless Claims

The Department of Labor released weekly jobless claims this morning and the results were mixed. For initial claims, they remain stubbornly above 1 million at 1.3 million. That was above expectations of 1.25 million but was still another decrease week over week, making it a record fifteenth streak week with lower jobless claims on a seasonally adjusted basis. This week was also yet another example of how even though claims are improving, the pace of improvement has slowed dramatically. In fact, claims only fell 10K this week. That is the smallest decline of these past 15 weeks.

Although the seasonally adjusted number showed a small improvement, actual reported claims on a non-seasonally adjusted basis actually rose from 1.395 million to 1.503 million. That was the highest reading since the first week of June. Additionally, that increase was the first time that jobless claims (NSA) rose since the last week of March, snapping a record streak of 13 consecutive weeks with lower claims.

Given continuing claims are lagged an additional week, they would not reflect that uptick as that reading continued to fall. Seasonally adjusted continuing jobless claims now total 17.34 million which is the lowest since the second week of April.

Looking at claims on a state by state basis, the main drivers of higher NSA claims this week have been some of the states with the largest increases in COVID cases like California, Georgia, and Florida. In the case of Florida, it saw a massive increase in first time jobless filings, nearly doubling from 66,941 last week to 129,408 this week. Meanwhile, Texas is bucking that trend with one of the largest improvements in claims despite higher case counts. As for continuing claims in the week ending July 4th, Florida, California, Georgia, Pennsylvania, and Texas, have all seen the largest increases in continuing claims. New York, North Carolina, and Texas on the other hand have seen the biggest declines. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: High Frequency Indicators Tracking Stocks

Bespoke’s Morning Lineup – 7/16/20 – Data Dump

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

We just got a big slug of economic data, and overall the results were positive. After an enormous bounce in retail sales for May, June’s reading came in much better than expected once again. The Philly Fed Manufacturing report was also better than expected but fell slightly from June’s reading. The one fly in the ointment was Initial Jobless Claims. While this week’s reading declined for a record 15th straight week, it did miss expectations. Continuing Claims, however, managed to come in slightly below forecasts. All in all, this data looked positive at the top line.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, the latest earnings reports, global economic data, trends related to the COVID-19 outbreak, and much more.

In the whole ‘game’ of quarterly earnings, the general strategy for companies is that whatever earnings you report, just make sure it’s better than expected. Companies that beat estimates tend to see better share price reactions while companies that miss EPS forecasts tend to see adverse reactions to their stock prices. That’s the general pattern, but there are always exceptions, especially among the major brokers.

Take Goldman Sachs (GS), for example. Yesterday the company reported quarterly EPS $6.26 per share, which was $2.35 above the consensus expectation of $3.91, or an EPS beat of over 60%. Looking through our Earnings Explorer tool, yesterday’s report from GS was the third-largest EPS beat for the stock since at least 2001. Given the magnitude of the beat, how much do you think GS was up yesterday? 5%? 10%? How about 1.4%. That’s right. The third-largest EPS beat for the company in practically 20 years resulted in a gain for the stock of just 1.4%!

Looking through the Earnings Explorer at Goldman’s largest EPS beats shows an interesting trend. Including yesterday, on the earnings reaction day of the ten largest EPS beats for GS, the stock’s average change was a decline of 0.1% (median: +0.2%) with gains only six times. Even more interesting is the fact that the company’s two largest EPS beats in April 2009 and April 2011 were met with selling.

We also looked at Goldman’s stock price reaction following the nine times it has missed EPS forecasts (or reported inline EPS). Of the nine occurrences since 2001, the stock’s average one-day reaction to earnings was a gain of 0.7% (median: +0.2%). On an average basis, at least, Goldman has derived no benefit to its stock from reporting blowout numbers.

Daily Sector Snapshot — 7/15/20

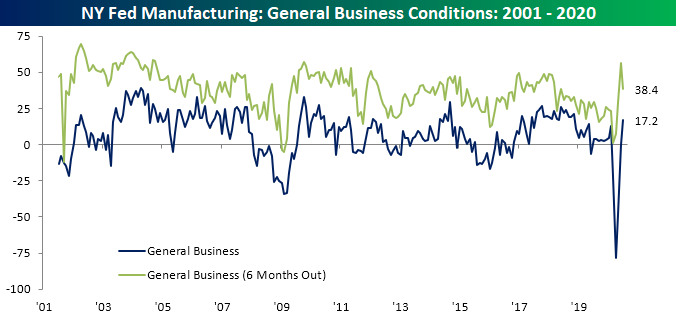

First Expansionary Empire Fed Since February

The New York Federal Reserve released its July reading on the manufacturing sector this morning and for the first time since February, the headline index indicated that activity rose month-over-month in the region. Not only was it the first expansionary reading (those above 0), but at +17.2, it was also the highest level of the index since November 2018 when it stood at +21.1. This month also marked a third consecutive monthly increase.

Although the index for present conditions is showing some of the strongest levels of the past couple of years with another uptick in July, optimism for the next six months pulled back. The index for general business conditions six months in the future fell to 38.4 from a multi-year high of 56.5 in June. That 18.1 point decline was the largest since March’s 21.7 point decline and the ninth-largest decline of all months.

While the pickup in activity was not as large as last month, for multiple individual categories the gains were still in the 90th percentile or better of all periods. Conversely, the declines in the indices for expectations for General Business Conditions, New Orders, and Shipments were all in the bottom decile of all readings. This month’s report also marked a turn for a few components as they changed from contractionary to expansionary. This was the case for the indices for General Business Conditions, New Orders, and Number of Employees. Now more than half are expansionary.

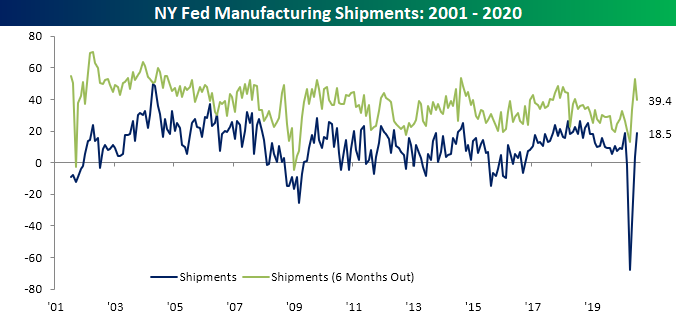

The two indices that rose the most this month were those for New Orders and Shipments. For the index for New Orders, it was the first non-contractionary reading since February, and for Shipments, it marked back to back readings above 0.

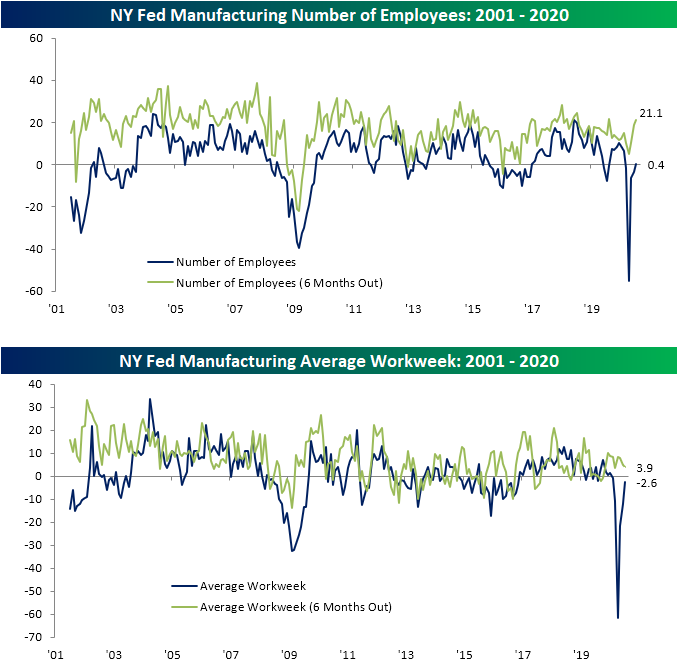

One major positive of this month’s report was the reading on employment. After four straight months of a greater share of manufacturers reporting decreases in employment, July marked an equal share of companies reporting an increase in employment as a decrease (21.9%). Additionally, the reading for future expectations rose to its highest level since August of last year indicating companies are at least expecting to increase hiring in the near future. Although employment was stabilized, average workweek did continue to fall, albeit, not by as much as previous months. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

B.I.G. Tips – Nasdaq Hot Streak Continues

Chart of The Day: Next Up for Earnings: Netflix (NFLX)

The Most Volatile Stocks on Earnings

Bespoke’s Earnings Explorer tool is all an investor needs to navigate what is usually a messy period each quarter — earnings season. The Earnings Explorer tool provides a full calendar of upcoming reports along with detailed historical earnings information for individual stocks that ties the data up into a nice bow that you can use to make informed decisions. You can use the tool to search for historical reports and summary data for individual stocks, or use our screening page to find stocks that typically beat or miss estimates, raise or lower guidance, or trade higher or lower in reaction to earnings. It’s also a great way to track macro earnings trends to see how strong or weak reports have been coming in lately as well as how strong or weak share price reactions to earnings have been. We urge you to try out our Earnings Explorer if you have never used it. You can do so with a two-week free trial to Bespoke Institutional.

Below is a chart included on our Earnings Explorer page that shows the number of earnings reports by day over the upcoming month. As shown, the next three weeks will consistently see dozens of reports per day.

At the start of each earnings season, we provide a few lists of important stocks set to report in the coming weeks. Below is a list of the 35 largest stocks set to report over the next month. For each stock, we include its current consensus analyst EPS and sales estimate along with its historical EPS beat rate and its average one-day share price change on its earnings reaction day (on an absolute basis). This lets you see how volatile a stock typically is in reaction to its earnings report.

Of the 35 largest stocks set to report, Apple (AAPL), Facebook (FB), Johnson & Johnson (JNJ), Mastercard (MA), Cisco (CSCO), and AbbVie (ABBV) have topped analyst EPS estimates the most often at 89% of the time or more. In terms of share price volatility, stocks like Netflix (NFLX), Tesla (TSLA), and Amazon (AMZN) typically experience a one-day move of more than 8% (in either direction) on their earnings reaction days. On the flip side, stocks like JNJ, Verizon (VZ), Exxon Mobil (XOM), and Chevron (CVX) typically see a one-day change of less than 2% on their earnings reaction days.

On an average basis, the 35 largest stocks set to report over the next month are much less volatile on their earnings reaction days than all stocks set to report. Whereas all stocks set to report over the next month have historically seen their share prices average a one-day move of +/-5.57%, the average one-day move of the 35 largest stocks in reaction to earnings is just +/-3.84%. In terms of beat rates, the largest stocks typically exceed EPS estimates at a much higher rate than average as well (75% vs. 61.5%).

Moving on, below is our list of the 35 stocks set to report over the next month that typically see the biggest moves in reaction to earnings. To make the list, the stock must have at least five years worth of quarterly earnings reports. Each of the stocks listed below typically moves at least 11% up or down on its earnings reaction day (the first trading day following its earnings report). The Container Store (TCS) is the most volatile stock on earnings with an average one-day change of +/-16.8% after it reports. TCS is scheduled to report after the close on Tuesday, July 28th.

The next most volatile stocks in reaction to earnings which all average one-day moves of more than 15% are Enphase Energy (ENPH), Groupon (GRPN), and Infinera (INFN). While GRPN and INFN are both down 20%+ YTD, ENPH is up 113.9% on the year, which means expectations for its upcoming report on 7/30 will be sky-high.

Other notables on the list of most volatile stocks in reaction to earnings include Wayfair (W), Yelp (YELP), LendingTree (TREE), Chegg (CHGG), Twitter (TWTR), Netflix (NFLX), Etsy (ETSY), and Grubhub (GRUB).

As shown in the table, Netflix (NFLX) is by far the largest stock on the list with a market cap of $230 billion. The next largest stock on the list — Twitter — has a market cap that’s just a tenth of NFLX. Even though it’s now an established blue-chip S&P 500 company, NFLX still typically sees huge moves when it reports its quarterly numbers. We’ll get to see how the stock reacts to its Q2 2020 report soon as NFLX is set to report Thursday after the close. Earnings definitely do not usually give shareholders a chance to “Netflix and chill.” We urge you to try out our Earnings Explorer tool today! It’s a must-have during earnings season. One of the benefits of the tool is it allows you to create a custom earnings release calendar for just the stocks that you follow most closely. You’ll never be blindsided by an earnings report again. Simply start a two-week free trial to Bespoke Institutional to gain access to our Earnings Explorer tool now.