Bespoke’s Morning Lineup – 3/29/21 – Media Stocks in Focus

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“When you combine ignorance and leverage, you get some pretty interesting results.” – Warren Buffett

Media stocks are in focus this morning as the unwind of the Archegos hedge fund that began last week continues today. In today’s Morning Lineup, we provided a rundown of the situation and the key factors that will shape how things play out, so make sure to check that out (pg 4).

Futures are lower as financials that have been caught up in the liquidation look to open lower. Keep in mind also, that despite the weakness at the open, US equities saw major surges into the close on Friday.

Also in today’s report, check out updates on the latest market news and events from the US and around the world, including a summary of the Archegos hedge fund blow-up and its potential impact, profits in China, the rates market, the latest US and international COVID trends including our series of charts tracking vaccinations, and much more.

One bank being hit especially hard from the blow-up in the media stocks over the last week has been Nomura. Nomura has seen a lot in the last forty years. From the bursting of the Japanese stock bubble in 1989, the 1987 stock market crash, the failure of Long-Term Capital in the 1990s, and then the credit crisis just over 10 years ago, the bank has faced a number of crises. This morning, the Japanese bank disclosed that it faces $2 billion in losses tied to margin calls, and compared to those prior periods, $2 bln doesn’t have quite the shock value that it used to.

Don’t tell that to the stock though. Overnight, shares of Nomura fell more than 16%, which is the largest one-day decline the stock has experienced in at least 40 years.

Bespoke Brunch Reads: 3/28/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Policymaker Profiles

The Years of Work Behind Washington’s Best-Liked Man by Claudia Sahm (NYT)

An oral history of how a strait-laced Republican and former Wall Street executive has helped push the world’s most important central bank in a genuinely populist direction. [Link; soft paywall]

The Born Prophecy by Richard B. Schmitt (ABA Journal)

In the late-1990s, the nascent derivatives markets were starting to boom, and CFTC Chair Brooksley Born tried to set up prudential regulation. Her efforts were quashed by Clinton administration Treasury Secretary Bob Rubin, his top deputy Larry Summers, and Fed Chair Allan Greenspan. [Link]

Odd Marketing

Post Consumer Brands to repay shoppers for black-market Grape-Nuts purchases by Noah Manskar (NYP)

Consumers desperate for their fibrous favorite were willing to pay as much as $100 per box earlier this year, prompting parent company Post to offer to reimburse the biggest fans for their overpriced purchases. [Link; auto-playing video]

Read the Pentagon’s 20-Page Report on Its Own Meme by Matthew Gault (Vice)

An unimpressive effort to skewer Russian hackers spent three weeks filtering through an approval process at the Pentagon before winding up on the US Cyber Command’s Twitter feed. [Link]

Capex

A Van Fight Is Brewing by David Welch (Bloomberg)

Commercial vans typically travel less than 100 miles per day, so electric conversion of fleets that reduce operating costs thanks to fewer moving parts and fuel costs are compelling for operators…and that’s before considering big tax incentives. [Link; soft paywall]

Intel is spending $20 billion to build two new chip plants in Arizona by Kif Leswing (CNBC)

After losing huge ground to foreign competitors, Intel has decided to shift its strategy towards a more US-centric approach. The result is billions of capex on two Arizona factories. [Link]

Weird News

How Many Slaps Does it Take to Cook a Chicken? This YouTuber Built a Slapping Rig to Find Out by Alyse Stanley (Gizmodo)

Energy is fungible, so imparting kinetic force on a chicken should at least hypothetically be enough to raise its temperature to the point it is “cooked”. As it turns out, it’s not just a hypothetical possibility. [Link]

How to Kill a Zombie Fire by Matt Simon (Wired)

Peat fires can continue to burn long after they appear to be put out, and warming temperatures are making them more common. Luckily, new techniques are proving more effective in fighting these fires. [Link; soft paywall]

Gaming

RollerCoaster Tycoon: the best-optimised game of all time? by Matt Hrodey (PCGames)

Thanks to an expertise in a more fundamental language than the ones typically used to code graphics packages, RollerCoaster Tycoon’s original developer was able to pull off miraculous performance. [Link]

Infrastructure Week

Biden Team Prepares $3 Trillion in New Spending for the Economy by Jim Tankersley (NYT)

A two-part effort to revitalize physical infrastructure via investments in roads, bridges, telecommunications, housing, rail lines, ports, and green energy and human lives via job training, free community college, universal pre-kindergarten, subsidized childcare, and national paid leave is being floated by the Biden Administration. [Link; soft paywall]

Pandemic Spending

Pets and Pet Spending During the Pandemic: A Money Report by Paul Reynolds (Money)

Spending more time at home means spending more time with furry friends, leading to increases in value and affection of pets. Pandemic-enforced changes in behavior and increasing loneliness led to more purchases of pets, which were more commonly picked up from shelters or rescues than other sources. [Link]

Recast as ‘Stimmies,’ Federal Relief Checks Drive a Stock Buying Spree by Matt Phillips (NYT)

With $1400 economic impact payments rolling out the door, a legion of individual investors is looking to put their money to work in the stock market. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report Newsletter — 3/26/21

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Daily Sector Snapshot — 3/26/21

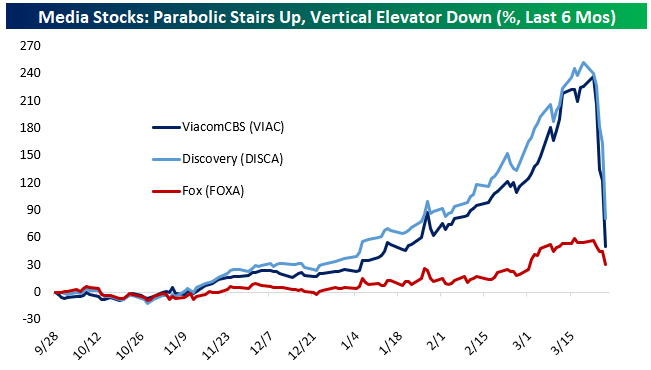

Media & Chinese Education Tech Carried Out On A Stretcher

This week we’ve seen a popular long blow up in a way that recalls the mess in GameStop (GME) earlier this year. As shown below, legacy media stocks like ViacomCBS (VIAC) and Discovery (DISCA) went parabolic since November. Fox (FOXA) also benefited, though to a much smaller degree. VIAC and DISCA both tripled in just a few months as hopes of a robust economic recovery boosting ad revenue and, more importantly, the potential for streaming riches similar to Disney (DIS) and its Disney+ platform helped fuel gains. But over the last four days, most of those gains have been incinerated. The catalyst appears to have been a secondary offering from VIAC a few days ago, with $1.7bn of shares sold into the $50bn market cap that existed at the time.

Since that secondary, the stock has been more than cut in half. There have also been rumors of a big, leveraged position by an unnamed fund having its portfolio seized and liquidated by its prime brokers. There have also been huge blocks of stock reported at dealers, with Goldman Sachs (GS) reportedly getting tapped to sell a block equivalent to more than 6% of VIAC’s free float and a second block equivalent to more than 12% of DISCA’s free float. In a reversal of the GME mess, VIAC has 18.5% of its float sold short, while DISCA’s short base is 29.7% of float. This particular blow-up is a win for shorts. Start a two-week free trial to Bespoke Institutional to access all of our analysis and market commentary.

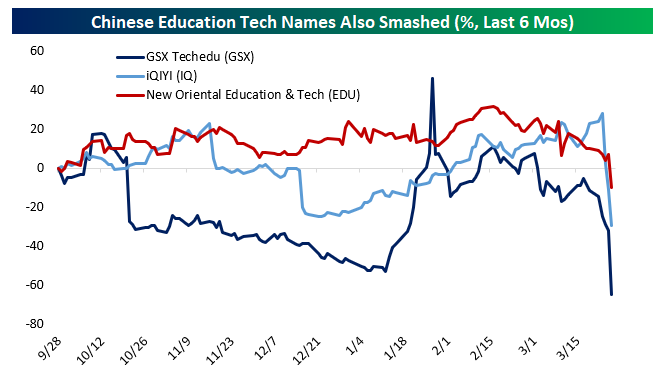

Another similar collapse has been playing out in Chinese education technology stocks listed in the US as ADRs. GSX Techedu (GSX) is down over 50% today, with a block offered by a dealer equivalent to almost 9% of the float. A similarly-sized block relative to float is also reportedly on offer in IQ. These names haven’t seen the same sort of parabolic gains as the media stocks above, but they’re a similar clustered theme that’s getting carried out to end the week.

ETFs Become Increasingly Active

In addition to providing a more liquid alternative to mutual funds, one of the big selling points of ETFs over the years has been the fact that since active management has been so bad on a collective basis, investors are better off settling for ‘market’ returns. This chart using data from Standard and Poors illustrates the point. Going back to 2001, there have only been six years where more than half of all domestic equity mutual funds outperformed the S&P 1500, and there has never been a year where even 60% of them outperformed. At the other extreme, you have years like 2011 and 2014 where less than 20% of funds outperformed.

Given the underperformance of active management over the years, it only makes sense that the vast majority of ETFs on the market have been passive in nature. There are also other factors like there being less of an ability to arbitrage that makes actively managed ETFs less feasible, but in any event, investor demand for passive index-tracking vehicles has been the main driver behind the explosive growth of ETFs.

In more recent years, though, actively managed ETFs have seen a surge in popularity. The chart below summarizes the year that each of the current ~400 actively managed ETFs that trade on US exchanges were launched. What clearly stands out is the fact that more than 30% of all actively managed ETFs were launched in 2020. Using data from ETF.com, we calculated that those 120 ETFs represent more than a third of all ETFs launched in the year.

For an investment vehicle that gained popularity because of its passive nature, the fact that actively managed ETFs have become so popular is noteworthy. Two factors behind their increased popularity stem from the success of the ARK funds, which have seen their assets under management swell to around $50 billion, and fees. Wall Street loves fees and because they offer more analysis behind security selection, actively managed ETFs can justify charging higher fees. For example, weighted based on Assets Under Management, ETFs have an average expense ratio of 0.19% per year. Within the actively managed ETF space, though, the weighted average expense ratio is nearly triple that at 0.54%. This new wave of actively managed ETFs can charge whatever fees they want, but ultimately, performance matters, and depending on how they perform over time will likely play a large role in how popular this area of the ETF space becomes. Start a two-week free trial to Bespoke Institutional to access all of our analysis and market commentary.

Bespoke’s Morning Lineup – 3/26/21 – Rates Remain Temperamental

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“‘Experience’ is what you got when you didn’t get what you wanted.” – Howard Marks

Futures are indicated mostly higher this morning, although Nasdaq futures have been under pressure as yields on the 10-year rise. It’s been a busy morning of economic data, but so far there have been no major outliers relative to expectations.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events from the US and around the world, including a discussion of Chinese Current Account, Japanese Inflation, German sentiment, the latest US and international COVID trends including our series of charts tracking vaccinations, and much more.

Within some of the major US indices, it’s a mixed picture with respect to their charts heading into the weekend.

The Russell 2000 broke below its 50-DMA moving average for the first time in over four months earlier this week, and while it bounced at support yesterday, it remains in a bit of limbo heading into today as it sits right between support below and its 50-DMA above.

The Nasdaq 100 has been having a much rougher go of it lately. With yields remaining temperamental, QQQ has been bouncing around in a range below its 50-DMA. Yesterday, it made a lower low relative to earlier in the week, so for now it remains in a tenuous position if you’re a bull on the index.

Lastly, while a number of other indices have been under pressure, the S&P 500 continues to chug along. Yesterday, SPY bounced right at support coinciding with its 50-DMA and uptrend. Bulls will want to see some follow-through after yesterday’s bounce, but if the weakness in the QQQ continues, it will be hard for SPY to maintain its immunity.

Bespoke’s Weekly Sector Snapshot — 3/25/21

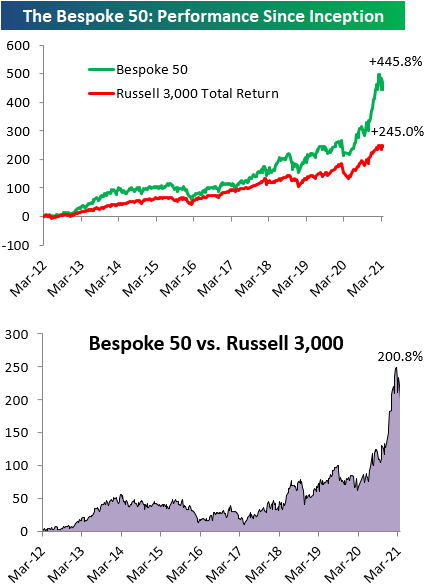

The Bespoke 50 Top Growth Stocks — 3/25/21

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” list is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” is up 445.8% excluding dividends, commissions, or fees. Over the same period, the Russell 3,000’s total return has been +245.0%. Always remember, though, that past performance is no guarantee of future returns. (Please read below for more info.) To view our “Bespoke 50” list of top growth stocks, please start a two-week trial to either Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, fees, or dividends are not included in the performance calculation. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities.

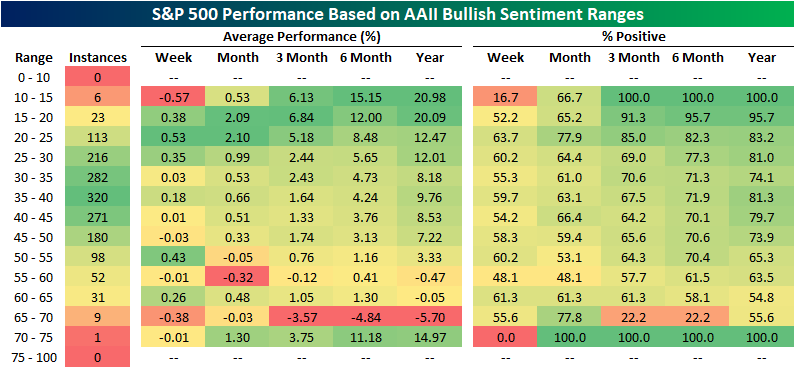

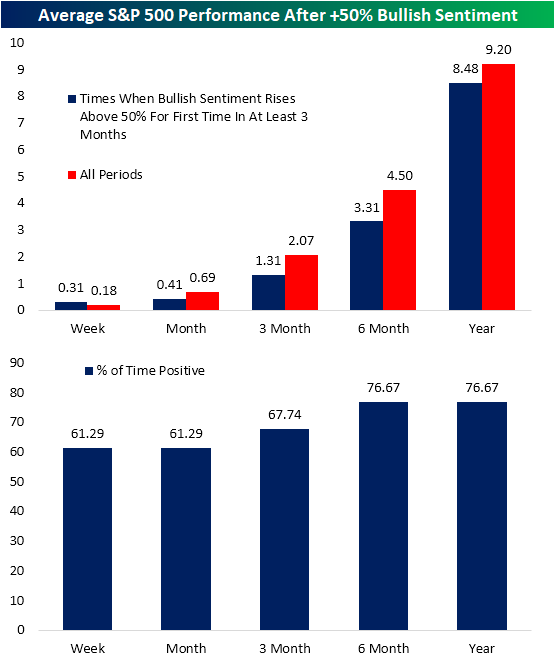

Bullish Sentiment Back Above 50% But Is That A Good Thing?

With the NASDAQ has put in a lower high and the Russell 2,000 touched the technical definition of a correction intraday today, sentiment has turned the other cheek. The AAII’s reading on bullish sentiment rose two percentage points moving back above 50% this week. Bullish sentiment is now at its highest level since the week of November 12th.

Since the AAII survey began in the late 1980s, there are plenty of instances (191 weeks) in which bullish sentiment has come in above 50%. As shown below, generally higher readings on bullish sentiment have resulted in weaker returns than when sentiment holds a more pessimistic outlook.

Given this, in the charts below we show the average performance of the S&P 500 in the weeks and months after bullish sentiment comes in above 50% for the first time in at least 3 months. Across those 31 past instances, while the index is frequently higher with positive returns better than three-quarters of the time six and twelve months later, the size of those gains are smaller than the norm. Only the one-week period has managed outperformance versus all periods with a 31 bps gain rather than the 18 bps gain for all other periods.

While a higher number of respondents reported as bullish, only 20.6% reported as bearish. That is the lowest level for bearish sentiment since December 2019 when it was only 0.1 percentage points lower than it is now. That is also the first time that less than a quarter of respondents have reported as bearish for three consecutive weeks since another three-week streak ending in the first week of 2020.

Given the high level in bullish sentiment and low level of bearish sentiment, the bull-bear spread rose back above 30 for the first time since the week of November 12th when it stood slightly higher at 30.97.

While both bullish and bearish sentiment are at notable levels, there was not a very large change in the percentage of respondents reporting as neutral. That reading rose only 1 percentage point to 28.5%. That leaves it right in the middle of its recent range. As recently as the first week of March this reading stood several percentage points higher at 34.4% whereas it is nearly equally as far away from its lows from early January.Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.