Chart of the Day – Economic Data Consistently Positive

Another Record in Gun Background Checks

It seems to happen every month these days, so it shouldn’t come as much of a surprise that FBI background checks for the purchase of firearms hit a new record in March, rising by more than a million to 4,691,738. It used to be that background checks followed a relatively steady saw-tooth seasonal pattern where, as shown in the chart below, they would fall throughout the first half of the year, bottom out in mid-Summer, and then steadily rise throughout the second half of the year. That seasonal trend became less consistent in the early part of the last decade and has completely broken down in the last two years. Now, it seems that the monthly number of background checks goes in one direction – up!

Despite rising to new record highs, the pace of growth in background checks has started to slow down a bit. March’s growth rate was 25.4%, and while that is still an extremely rapid rate of increase, it’s at the low end of the range from the last year where the y/y change in checks peaked out at 79.2% last July in the midst of the nationwide protests around the country. Click here to view Bespoke’s premium membership options for our best research available.

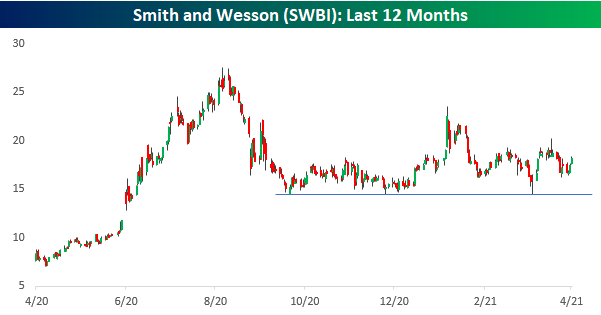

Just as the stock market and the economy don’t always move in lockstep with each other, the stocks of gun manufacturers don’t necessarily follow the path of gun background checks/sales. The charts below show the performance of the two largest publicly traded gun manufacturers over the last year – Sturm Ruger (RGR) and Smith and Wesson (SWBI). While background checks are at all-time highs, the prices of both stocks have corrected significantly from their highs last summer. After declines of 30%+ from peak to trough for both stocks, they have essentially been rangebound now for six months. However, while both stocks have been dead money, they haven’t broken down. In both cases, they have repeatedly bounced at support (~$60 for RGR and ~$15 for SWBI). As long as those levels continue to hold, they may be loaded with more than just blanks.

A Semi Snap Back

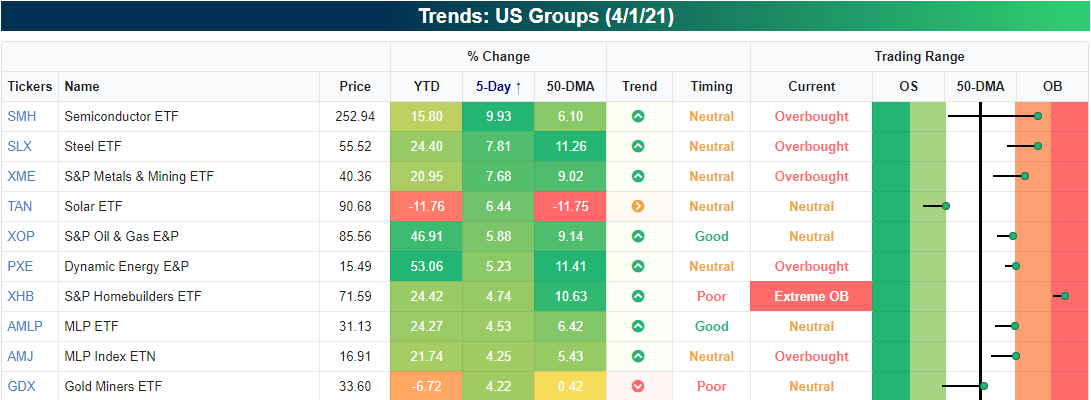

Headed into the long weekend, the Semiconductors (SMH) had been on a very impressive run over the prior five days. As shown in the snapshot of the US Groups screen in our Trend Analyzer, the group was the top performer (up just under 10%) in the five days ending last Thursday. That move brought it from well below its 50-DMA to deep into overbought territory.

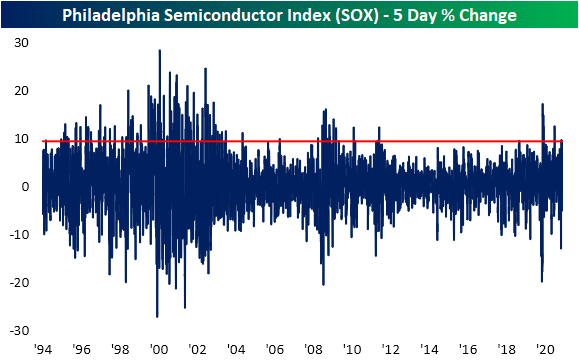

While the Semiconductor ETF (SMH) is up again today, it is still over 1% below its highs from mid-February. Meanwhile, the Philadelphia Semiconductor Index (SOX) has already broken out to a new record intraday high this morning.

Today’s gain for the SOX adds to a 9.5% gain for the index last week. As shown in the chart below, that 9.5% rally is historically large, especially relative to the past several years. In fact, the five-day gain through Thursday’s close stands in the top 5% of all five-day runs for the index. While there was another occurrence as recently as the five days ending March 15th, moves of this size have been fairly uncommon in the past decade. Prior to the most recent and March occurrences, the only other recent instances were in November and the spring of last year. Prior to 2020, the past decade only saw a small handful of other instances of rallies in the 95th percentile or better. Conversely, the volatility of the Financial Crisis and the late 1990s and early 2000s led to more frequent clusters of top 5% moves.

In the charts below, we show the performance of the semiconductor index following rallies that rank in the top 5% of all 5-day changes without another occurrence in the prior two weeks. The results show that there’s typically a near-term cool-down period after such a sharp one-week rally. One and two weeks later have both tended to underperform the norm (by 42 bps and 90 bps respectively), averaging declines with positive returns less than half the time. While there has been some near-term weakness, one month and a quarter out have both tended towards outperformance. Click here to view Bespoke’s premium membership options for our best research available.

March 2021 Headlines

Bespoke’s Morning Lineup – Market Gets Its Turn to React

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“If the end doesn’t justify the means, what does?” – Robert Moses

After one of those rare instances where an economic report was released on a day when the equity market was closed, the stock market is finally getting its opportunity to react to Friday’s stronger-than-expected employment report. While most major equity indices around the world remain closed for the Easter holiday, US futures are higher across the board to the tune of roughly 0.5%. The one exception is small-caps where the gains at the open will likely be well over 1%.

Read today’s Morning Lineup for a recap of all the major market news and events including the latest US and international COVID trends as well as our series of charts tracking vaccinations, and much more.

Heading into the new week, we wanted to provide a quick snapshot of each S&P 500 sector’s price chart over the last 12 months. Two things about the charts immediately stand out to us. First, all eleven sectors are comfortably above their 50-DMAs which is a sign of healthy breadth across the market spectrum. Secondly, even though every sector is above its 50-DMA and the S&P 500 hit a record high on Thursday, the only sector that also traded at a 52-week high was Real Estate, which accounts for less than 2.5% of the entire index. To us this is a reflection of the healthy rotation we continue to see where when one sector starts to lag, others are there to quickly pick up the slack. In fact, there are currently no sectors that are even 10% from a 52-week high and only two (Energy and Utilities) that are down more than 5% from their respective 52-week highs.

Bespoke Brunch Reads: 4/4/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Archegos

One of World’s Greatest Hidden Fortunes Is Wiped Out in Days by Katherine Burton and Tom Maloney (Yahoo! Finance)

The family office of a disciple of legendary growth investor Julian Robertson ran a stock portfolio with tens of billions into the ground in the course of just a few short days. [Link]

Credit Suisse Bid for Tidy Archegos Fix Ends With Banks Brawling by Sridhar Natarajan and Donal Griffin (Bloomberg)

As Archegos’ portfolio was melting down, its prime brokers tried to stick together, but several banks started liquidating blocks of stock instead of holding the line, driving the entire group to sell at the worst possible time. [Link; soft paywall]

Demographics

U.S. Church Membership Falls Below Majority for First Time by Jeffrey M. Jones (Gallup)

For the first time in the history of Gallup’s polling, less than half of Americans report that they are a member of a church, synagogue, or mosque. More than three-quarters did at the end of World War 2, and more than two-thirds did in the mid-2000s. [Link]

Older Millennials Are Closing the Wealth Gap With Their Parents by Rachel Louise Ensign (WSJ)

Recent years have seen the wealth gap between younger Americans and their Baby Boomer parents decline after running dramatically behind for years following the global financial crisis. [Link; paywall]

Strong Economy

America’s Imports Are Stuck on Ships Floating Just Off Los Angeles by Kara Dapena and Dylan Moriarty (WSJ)

While the Ever Given got all the attention in the Suez, the bigger traffic jam is arguably found closer to American shores as dozens of ships wait for LA/Long Beach port capacity to free up. [Link; paywall]

Tilman Fertitta says he’s been surprised by strength of his restaurants and casinos in March by Kevin Stankiewicz (CNBC)

The CEO of the holding company which owns brands like Joe’s Crab Shack, Morton’s Steakhouse, and Golden Nugget casinos reports people “are going out in huge numbers now” or even “blowing numbers away”. [Link]

Pandemic Fails

Johnson & Johnson’s vaccine is delayed by a U.S. factory mixup. by Sharon LaFraniere and Noah Weiland (NYT)

A confusion over which ingredients were going where led an employee of a subcontractor to use AstraZeneca ingredients in a batch of Johnson & Johnson vaccines, ruining as many as 15mm doses of the one-shot vaccine. [Link; soft paywall]

The Pandemic’s Wrongest Man by Derek Thompson (The Atlantic)

At every turn, gadfly Alex Berenson has mislead, confused, and just generally been wrong in his widely-followed analysis of the COVID epidemic; this is at least a start on exhaustively cataloging his litany of errors. [Link]

Investing

ARK Innovation ETF’s Approach is Ill-Timed for a Major Twist by Robby Greenwald (Morningstar)

While cost-competitive, ARK Invest’s ETFs are dependent on portfolio manager Cathie Wood and at risk of extreme concentration, while holding very large exposures relative to the size of the companies it invests in that could create major liquidity stress. [Link]

Industry Analysis

Methane pollution soars in US as shale drilling resumes by Justin Jacobs (FT)

With oil prices up after COVID, shale drillers are back in business and with them are methane emissions, a potent greenhouse gas which is released as oil is fracked. [Link; paywall]

How HUD and NAHB Created the U.S. Housing Crisis by James A. Schmitz Jr., Arilton Teixeira, and Mark L. J. Wright (Minneapolis Fed Working Paper Slides)

A compelling argument that protectionist efforts by the traditional homebuilding industry to prevent market share gains for much cheaper manufactured housing has had innumerable pernicious effects on the broader US economy. [Link; 80 page PDF]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report Newsletter – 4/1/21

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Bespoke’s Weekly Sector Snapshot — 4/1/21

Bespoke Market Calendar — April 2021

Please click the image below to view our April 2021 market calendar. This calendar includes the S&P 500’s average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases. Start a two-week free trial to one of Bespoke’s three research levels.

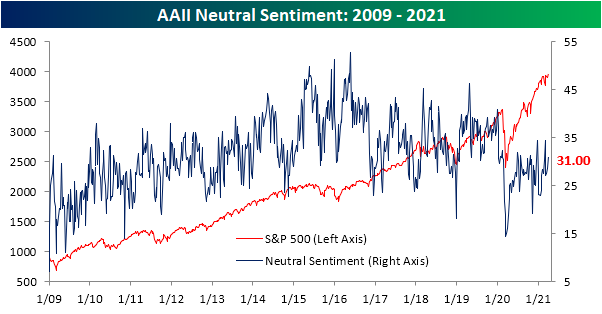

Sentiment Goes the Other Way of Price

The S&P 500 has risen around 2.5% to new record highs and crossing the 4,000 milestone in the past week. Despite this, optimism took a slight step back this week. The Investors Intelligence survey of newsletter writers released yesterday saw a lower share of respondents report as bullish; down from 57.4% last week to a three-week low of 54.4%. After coming in at the highest level in three months last week, the AAII’s sentiment survey also saw fewer respondents reporting as bullish. Last week, over half of respondents reported as bullish for the first time since November. Today, that reading has fallen to 45.8%. Despite the less optimistic tone, the 5.1 percentage point decline was the largest single-week drop in bullish sentiment since only the first week of March and the current level still stands in the top decile of the past five years. It is also over 7 percentage points higher than the historical average of 38%.

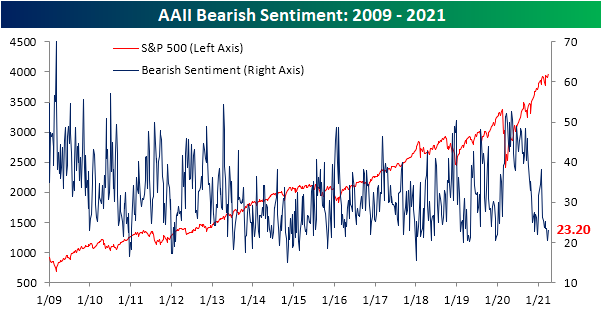

As bullish sentiment came in at a multi-month high last week, bearish sentiment fell to the lowest levels since December 2019. Bearish sentiment likewise saw a reversal this week as it rose 2.6 percentage points to 23.2%. Mirroring bullish sentiment, albeit off the low, the current level of bearish sentiment is still in the bottom 10% of readings of the past five years.

Those inverse moves in bullish and bearish sentiment have resulted in the bull-bear spread falling 2.7 points to 22.6. While that indicates a less optimistic tone than last week, the current reading shows that sentiment continues to largely favor the bulls. In fact, even after pulling back, the current reading sits in the top 5% of all weeks of the past 5 years.

While fewer respondents reported as bullish this week, not all of those jumped ship to the bearish camp. Neutral sentiment picked up the difference rising 2.5 points to 31%. That is the first reading of over 30% and the highest since the first week of March when it had risen to 34.4%. While that is an elevated level relative to the past year in which sentiment has become more polarized between bullishness and bearishness, the current level of neutral sentiment is actually just below the historical average of 31.41%. Click here to view Bespoke’s premium membership options for our best research available.