Inflation Issues For Small Businesses

In addition to getting a gauge on small business optimism, the NFIB’s monthly survey of small businesses also asks respondents about the biggest issue they face operating their businesses. On a combined basis, the biggest concern among small businesses is taxes or government red tape. Combined, these two issues were reported as the biggest problem for 35% of surveyed firms with taxes being the main culprit after rising 3 percentage points month over month. Right on the heels of government-related concerns, labor concerns loom large. 34% of respondents said that cost or quality of labor pose the biggest issue their business face with costs accounting for 8%, unchanged from last month, while the quality of labor jumped from 24% to 26%. For the latter, that is in the top 1% of all readings hitting the highest level since November 2019. If there is any positive to pull out of what Main Street views as the biggest problems, it is the lack of companies citing poor sales. Just 5% of respondents saw this as the biggest issue; down 13 percentage points versus last year, and it is now at the lowest level since September 2018. On the downside, the number of firms reporting problematic inflation has risen rapidly going from 2% at the end of 2020 to 8% today. Such an elevated reading has not been observed since April 2012. Click here to view Bespoke’s premium membership options for our best research available.

Daily Sector Snapshot — 6/8/21

Chart of the Day: Small Business Outlook Takes a Nosedive

Small Businesses Can’t Find Workers And Are Raising Prices

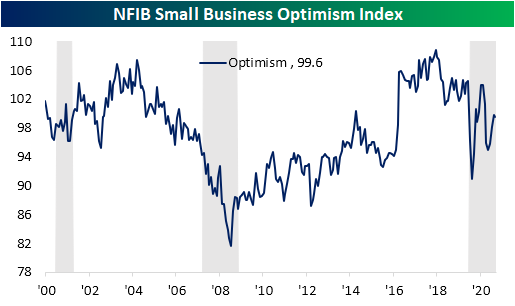

The NFIB released its monthly reading on the sentiment of small businesses this morning. In the past, we have noted how the results of this survey are often correlated with political happenings. As such, the index dropped in the wake of the election but found a bottom in January. Since then, it has remained weaker than during the Trump years, albeit it has also improved almost every month this year. That is except for the most recent month. May snapped a three-month winning streak with a slight decline from 99.8 to 99.6.

With the headline number slightly lower, breadth in the May report was fairly mixed. Of the ten inputs to the optimism index, half were higher, two went unchanged, and three were lower versus April’s readings. Three of those indices that moved higher—Plans to Increase Employment, Current Inventory, and Job Openings Hard to Fill—set new records. While it is not an input to the headline reading, the index for Higher Prices also rose to a new record high. Overall, the survey implied generally strong conditions with a few areas of concern: labor market tightness and inflation.

The report showed solid realized sales as the index of Actual Sales Changes rose 4 points to 7. That marks a return to pre-pandemic levels. On net, a higher share of businesses also expects sales to continue to improve, although only at 3, the index is still at the low end of its historical range. In spite of the higher actual sales, a higher share of businesses are reporting worse bottom-line results versus the prior three months as the index for Actual Earnings Changes fell to -11.

In an attempt to make up for those weaker margins, a record share of businesses also are reporting that prices are higher than three months ago. A net of 40% of respondents reported that they are raising average selling prices; a record high in the data dating back to 1986. The NFIB noted that price hikes were most common for wholesalers (65% reported higher prices vs. 2% lower) and manufacturers (47% reported higher prices and 1% reported lower). That is consistent with other data of the past few months showing prices are flying higher. Likely as a result of all of this in addition to other labor concerns (more on that below), the Outlook for General Business Conditions fell to -26, the lowest level since 2012 and in the bottom 1% of all months. Additionally, the share of businesses reporting now as a good time to expand ticked lower.

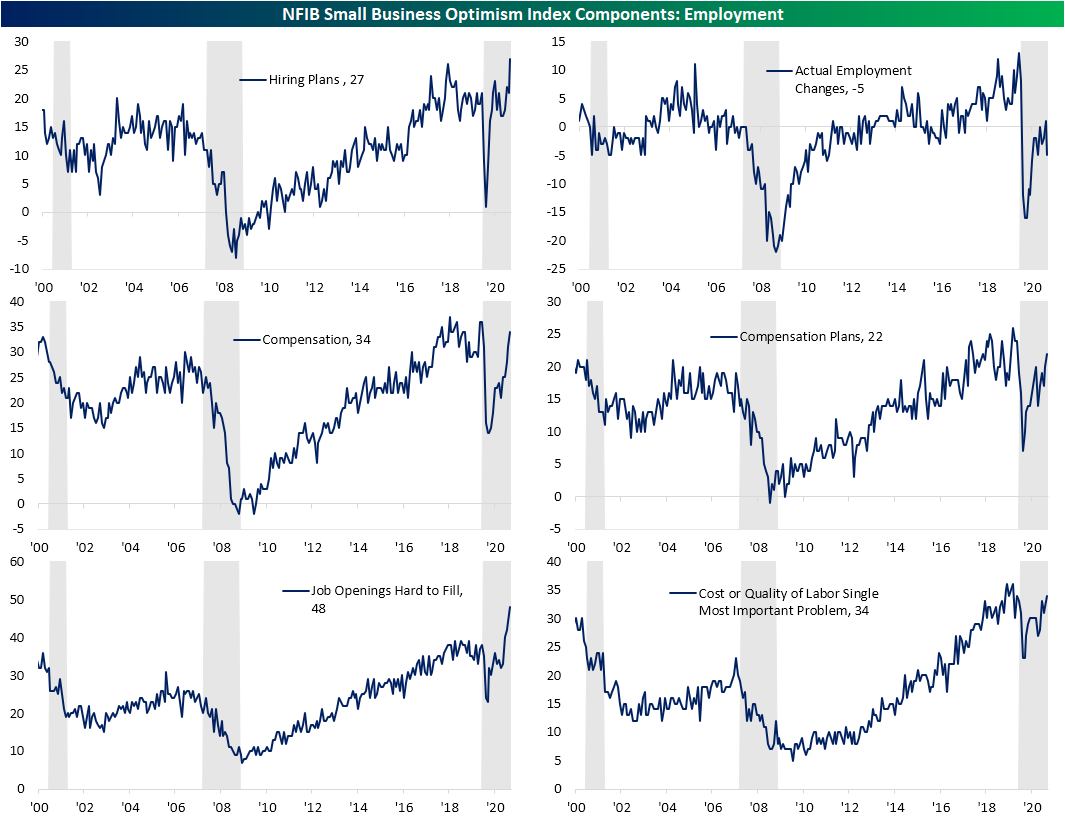

One major area of strength, at least in terms of demand, is employment. A net 27% of respondents reported that they plan to create new jobs within the next three months; surpassing the prior record high from August 2018 by a full point. But even though businesses are putting the offers out there, on net fewer businesses reported an actual employment change. In fact, that index fell sharply by 6 points; a move that ranks in the bottom 2% of all monthly changes. Additionally, a record share of businesses reporting job openings as hard to fill as 34% of businesses report their biggest problem to be either the cost or quality of labor. That is indicating significant labor market tightness. As a result, more businesses are or are planning to raise compensation with those indices at the highest levels of the past year and consistent with readings from 2017 up through the onset of the pandemic. Those higher costs are likely one reason for the weaker reading in actual earnings changes and higher selling prices previously mentioned.

As for the other side of the production function, capital expenditures are not being raised in any sort of significant way nor are plans to increase expenditures. Potentially to get ahead of the strong demand and labor supply mismatch, businesses are raising inventory levels with a record share of businesses reporting that current inventory levels are “too low”. Rising to 8, that index took out the joint high of 7 from last month and December. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke Stock Scores — 6/8/21

Brazil Boils

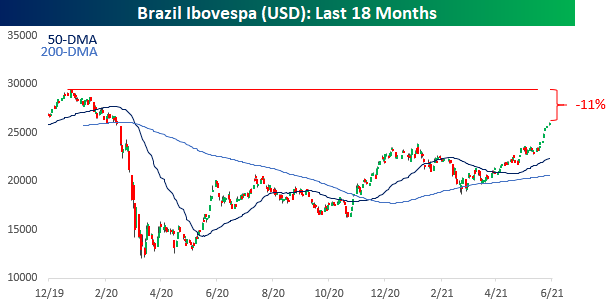

It’s been a hot time for stocks in Brazil over the last several days. The country’s benchmark Ibovespa index broke out above its highs from early this year completing a cup and handle formation and hasn’t looked back since. Yesterday was the index’s eighth straight day of gains during which the index has rallied more than 6%. This morning, the country is in the spotlight again as Berkshire Hathaway (BRK.b) has agreed to buy a $500 million stake in Nu Pagamentos SA, valuing the company at $30 billion. You may have never heard of Nu Pagamentos, but it is a privately held company that does business under the name Nubank, which is the largest fintech company in Latin America.

With the recent weakness in the dollar, the rally in Brazilian equities has been even stronger for US-based investors. During the same eight-day winning streak, the Ibovespa is up over 12% is USD. As shown in the chart below, though, while dollar weakness has flattered returns for Brazilian equities from a US-based investor’s perspective in the short-term, it’s been the opposite pattern over the longer term. While the Ibovespa is well above its early 2020 highs in local currency terms, on a dollar-adjusted basis, it’s still down 11%. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – Charts We’re Watching

Bespoke’s Morning Lineup – 6/8/21 – Six or Twelve

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“You can only do so many things great, and you should cast aside everything else.” – Tim Cook

Depending on whether you look at closing or intraday levels, the S&P 500 closed out yesterday within six or twelve points of a record high. This morning, equity futures are up relative to Monday’s close, and the way things are going now, that closing high from a month and a day ago will be topped at the open.

The economic calendar is light today. NFIB Small Business Optimism for May was released earlier, and while economists were expecting a modest bounce from April’s level, the actual reading showed a modest decline (99.6 vs 101.0 consensus estimate and 99.8 in April). A key theme from this month’s report was the fact that almost half of all small businesses said they have been unable to fill open positions. As an example, 93% of small business owners hiring or trying to hire reported that they received few or no qualified applications. We’re also likely to see a reinforcement of this trend later this morning when the JOLTS survey shows another likely record number of job openings despite the fact that job creation has been less impressive than forecasts.

Read today’s Morning Lineup for a recap of all the major market news and events including a discussion of the Biogen Alzheimer’s treatment, a recap of activity and economic data overnight, and the latest US and international COVID trends including our vaccination trackers, and much more.

Yesterday marked the beginning of the annual Worldwide Developers Conference (WWDC) from Apple (AAPL). While the company has been holding this event for over 30 years, its popularity really exploded following the launch of the iPhone in 2007. The conference first sold out in 2008 after Steve Jobs announced in October 2007 that Apple would open the iPhone up for developers to write software. The WWDC has historically been a noteworthy event for people involved in the development of Apple products, but it hasn’t historically been a great period for the stock.

The table below shows the performance of AAPL stock leading up to and during every prior WWDC in the iPhone era and since the conference first sold out in 2008. This year marks only the fourth time in the last 14 years where AAPL’s stock was down YTD heading into the conference. During the conference, though, performance has been on the weak side averaging a decline of 1.43% (median: -1.15%) with positive returns only four out of 13 times.

Daily Sector Snapshot — 6/7/21

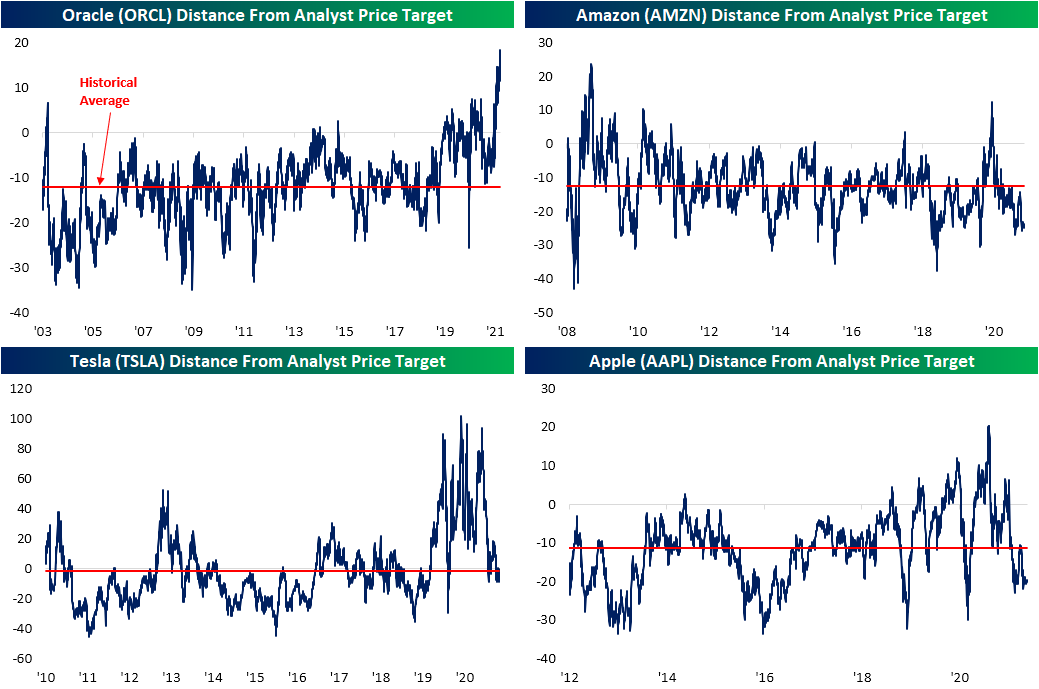

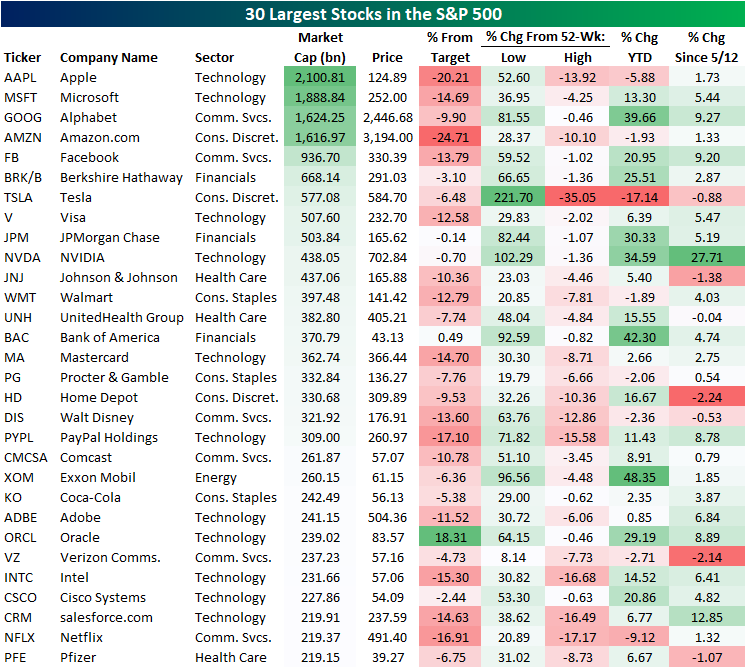

Orcale (ORCL) Surges Above Price Targets

Thus far in 2021, most of the 30 largest S&P 500 stocks are in the green on a year-to-date basis with a few notable exceptions. The largest company with a $2.1 trillion market cap, Apple (AAPL), has fallen 5.88% year-to-date and is down nearly 14% from its 52-week high. Of the 30 largest stocks, the only two other stocks that are down by more year-to-date and are also further below their 52-week highs are Netflix (NFLX) and Tesla (TSLA). TSLA has been particularly hard hit with a 17% loss so far in 2021 which brings it down 35% from its high. Conversely, Alphabet (GOOG), JPMorgan Chase (JPM), NVIDIA (NVDA), Bank of America (BAC), and Oracle (ORCL) are some of the stocks that are closest to new highs (around 1% away) and are up around 30% or better YTD. Unsurprisingly for an Energy sector stock, the best performer this year has been Exxon Mobil (XOM) which is closing in on a 50% gain YTD.

After setting new record highs right around a month ago, the S&P 500 pulled back to its 50-DMA which it found support at on May 12th. The subsequent rally since then has seen the index make a run back up to those record highs which it has been hovering around in recent days. Since its May 12th low, by far the two best-performing stocks in the 30 largest stocks have been NVIDIA (NVDA) which has gained 27.71%, and salesforce.com (CRM) which has risen a smaller, but still impressive, 12.85%; both companies reported triple plays in late May which partially played a role in that strength. While far from a leader, AAPL is also up in that time as is the rest of the trillion-dollar market cap club.

Another interesting thing to note of the stocks in the table above is their distances from their analyst price targets. There are a handful like JPMorgan Chase (JPM), NVIDIA (NVDA), and Bank of America (BAC) that are currently within 1% of their consensus price targets. After their strong runs this year, though, the median distance from a target for the full list is approximately 10% below. BAC is actually slightly above its target, and not many others can say that. In fact, the only other name of the largest stocks currently trading above its analyst price target is Oracle (ORCL), and it’s doing so in a big way. As shown above, ORCL is currently over 18% above its target. Going back through the history of the data for the stock, no other period since 2003 has seen ORCL trade as elevated above its target as it does now. For ORCL to get back below its average price target, either its share price would need to fall or analysts would need to significantly increase their price targets.

Looking at the other end of the spectrum, Amazon (AMZN) and Apple (AAPL) are the two names furthest below their price targets. For each of these stocks, trading that far below the analyst price target has been relatively uncommon over the past several years. For these two stocks to get back to where they normally sit relative to analyst price targets, either the stocks need to rise or analysts need to lower their price targets. For these two mega-cap behemoths, we think the latter is more likely.

While it does not stand out from the list of the other largest stocks as it only trades 6.5% below its target, TSLA is also notable. Over the past two years, the stock has continuously left its targets in the dust on average sitting 26% above. In July of last year, TSLA’s price even doubled the target price. But with the stock’s weakness this year, its distance from its price target is much closer in line with the historical average. Click here to view Bespoke’s premium membership options.