The Bespoke Report — 8/20/21

This week’s Bespoke Report newsletter is now available for members.

Before we get started with a preview of our weekly market recap, below we highlight recent performance across a wide range of ETFs representing various asset classes, national equity markets, and US sectors or indices.

- Global equities had a rough week although US stocks saw a decent rally into the close on Friday.

- Small-caps and mid-caps were down the most this week, while Energy, Financials, and Materials fell sharply as well. On the flip side, we saw nice gains in Health Care, Utilities, and Consumer Staples.

- We’ve seen steep declines in countries like Australia, Brazil, Canada, and China this week and this quarter, and international equities are underperforming the US in 2021 by a significant amount.

- The Bitcoin and Ethereum Trusts have surged in Q3, with GBTC up 32.7% and ETHE up 38%. ETHE is back up nearly 100% on the year after the bounce it has had.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 8/20/21

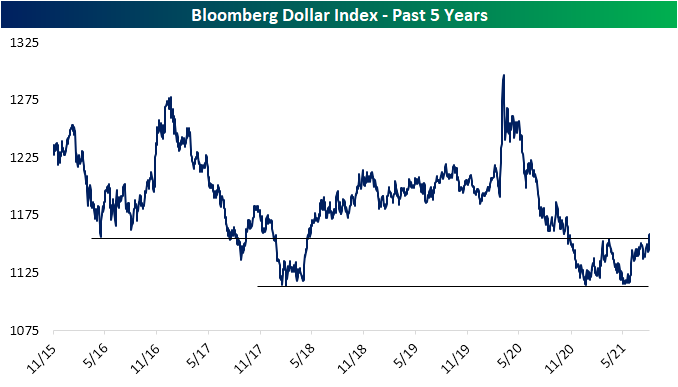

US Dollar Breaks Out

After roughly two months of declines, at the end of May the US dollar (proxied by Bloomberg’s dollar index) found support around the lows from the first week of the year. Since then, the dollar has rallied 4.13%, moving back above its moving averages in the process which have also acted as support ever since. This week alone the dollar has gained 1.4%, and that upward move brings the dollar to the highest levels since early November and the early spring highs when the index stopped short of its 200-DMA.

Taking a step back to look at the past five years, those lows that were reached earlier this spring and at the start of the year can actually be traced all the way back to early 2018 lows. Similarly, the recent highs that were taken out this week are around the same levels as the early 2016 lows. With the dollar now having broken out, it is no longer at the low end of that five-year range. Click here to view Bespoke’s premium membership options.

Fewer Stocks Above Moving Averages

At the moment, of the S&P indices based on market cap, only the S&P 500 is currently above its 50-DMA. Meanwhile, the S&P Mid-Cap 400 is trying to move back above and the small-cap S&P 600 is around 3.5% below its 50-day and moving lower. As for the individual stocks of these indices, it is more or less the same story. The S&P 500 has the strongest percentage of stocks above their 50-DMAs at 56.44%. That is down though from a high of 68.91% at the end of last week. Mid and small caps are even weaker with only 36.5% of the S&P 400 above and less than 30% of the S&P 600 above. While this week saw legs lower in the percentage of stocks above their 50-DMAs for each of these indices, we would also note that recent readings are also well below very strong levels that had been observed from late last year through this past spring.

The same goes for the percentage of stocks above their 200-DMAs. For each of these market cap indices, readings around 90% were commonplace for most of the past year, that is, until the past few months and more specifically the past week. Roughly three-quarters of S&P 500 stocks closed above their 200-DMAs yesterday which is the lowest level since early November. Again, that also applies to mid and small caps which have even smaller shares of stocks above their 200-day moving averages at 65.99% and 60.17%, respectively. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 8/20/21 – Small-Caps Break Below 200-DMA

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I always believe that prices move first and fundamentals come second.” – Paul Tudor Jones

US equity futures are in the red again this morning with SPY down 40 basis points in pre-market trading. We’re beginning to sense a pattern here…

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Also, make sure to check out our Daily Sector Snapshot.

As shown below, large-cap index ETFs like DIA, QQQ, and SPY are quickly nearing their 50-day moving averages after declines from record highs this week. The Russell Mid-Cap ETF (IWR) already broke below its 50-DMA earlier in the week, and of course, the Russell 2,000 Small-Cap ETF (IWM) has been below its 50-DMA for the last month or so.

Small-caps have been incredibly weak this summer relative to the rest of the market. After yesterday’s drop, the Russell 2,000 is now down 9.65% from its record high made on the Ides of March. It will only take another slight move lower to leave the index in official “correction” territory (a 10% drop).

Yesterday’s weakness also caused the Russell 2,000 to break below support at its long-term 200-day moving average.

The close below the 200-DMA ended a streak of 226 consecutive closes above the 200-DMA for the Russell. The just-ended streak is the 11th longest on record dating back to 1978 when the index began.

So what’s next now that this technical breakdown has occurred for small-caps? Find out by reading today’s Morning Lineup. Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Bespoke’s Weekly Sector Snapshot — 8/19/21

The Bespoke 50 Top Growth Stocks — 8/19/21

Chart of the Day – What Do Individual Investors Know That The Market Doesn’t?

One of the Best Weeks of the Year for Claims

Initial jobless claims hit another pandemic low this week dropping to 348K from last week’s 2K upwardly revised reading of 377K. That was also 16K below expectations and the first better than expected print in six weeks. While recent releases have disappointed relative to forecasts, this week did mark the fourth week in a row that claims have dropped. That is the longest stretch of consecutive declines since a six-week streak ending on June 4th.

On a non-seasonally adjusted basis, initial claims fell to 308.57K which is again the lowest level since the start of the pandemic. Meanwhile, pandemic unemployment assistance claims ticked up to 109.38K from 103.85K the previous week. The main state driving that increase was Ohio which saw claims more than double. Maryland, Oregon, and California were the other states to have seen the biggest increase in PUA claims. Those increases also come even as the program is slated to end in just two weeks on September 4th.

As for the decline in claims for unadjusted regular state programs, we would caution against reading too deep into the number on account of strong seasonal tailwinds. As shown below, the current week of the year (33rd) is tied at second for the week of the year that most often sees claims decline. As shown in the second chart below, there has only been one year, last year, in which claims were higher week over week in the 33rd week of the year.

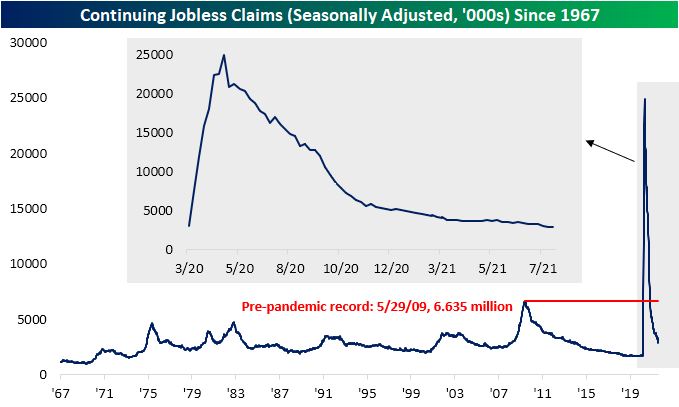

Seasonally adjusted continuing claims missed expectations by 20K this week, but at 2.82 million, this week’s reading still marked a third consecutive decline. As such, claims are still at the lowest level of the pandemic and are closing in on coming within one million from the March 2020 levels.

While the most recent reading on continuing claims was lower, purely looking at regular state claims does not show the full picture. Including all other programs creates some additional lag meaning the most recent data is through the last week of July. Through that week, total claims fell below 12 million for the first time of the pandemic, totaling 11.76 million. Driving that decline were 79.9K and 66.08K declines in regular state and PEUC programs. The biggest decline came from the extended benefits program, though. That program saw claims get more than cut in half after a significant uptick the previous week. Throughout the month of July, claim counts for the extended benefits program were particularly volatile. They started off the month with a sub-100K reading of 98.4K, then rose all the way up to 343.5K, dropped to 239.6K, then rose again to 398.8K before falling back down to 177.9K in the week of July 30th. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 8/19/21

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A trader, in addition to studying basic conditions, remembering market precedents and keeping in mind the psychology of the outside public as well as the limitations of his brokers, must also know himself and provide against his own weaknesses.” – Edwin Lefèvre, Reminiscences of a Stock Operator

US equity futures are currently down pretty significantly (-0.80%) after major indices fell more than 1% yesterday. The declines are being led by the Energy sector, which has already fallen more than 6% over the last week.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Also, make sure to check out our Daily Sector Snapshot.

Breadth had made a bit of a turnaround earlier this month, but the last week has been brutal with investors really selling the cyclical sectors that are dependent on a strong economy. While the cap-weighted S&P 500 is less than 2% from all-time highs, the average stock in the S&P 1500 index (made up of large-caps, mid-caps, and small-caps) is 15.8% from its 52-week high. As shown below, the average Energy stock in the S&P 1500 is more than 30% from its 52-week high, while Communication Services stocks are down an average of 21.4% from their highs. The defensive Utilities sector has held up the best with the average stock just 6.1% from its 52-week high.

It’s been a choppy summer for stocks even though things look positive at the index level. As shown below, over the last three months, the cap-weighted S&P 1500 is up 5.9%, but the average stock in the index is actually down 0.65% over the same time frame.

Want to see more charts and analysis ahead of today’s open? Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.