Chart of the Day – Powell Takes The Podium

Bespoke’s Morning Lineup – 7/28/21 – Three Down…

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Companies that get confused, that think their goal is revenue or stock price or something. You have to focus on the things that lead to those.” – Tim Cook

With three of the big five reporting earnings after the close yesterday, investors got through the night of earnings relatively unscathed. As we approach the opening bell, Alphabet (GOOGL) and Microsoft (MSFT) are both indicated higher while Apple (AAPL) is just modestly lower. The fact that all three of these stocks rallied sharply into earnings and none are down significantly post-earnings is a pretty encouraging outcome.

There’s not a lot of economic news to contend with this morning, but we will get an FOMC decision on interest rates at 2 PM eastern and a press conference from Chairman Powell at 2:30. Earnings data is still coming in hot and heavy, though, and will be that way right up through Friday morning. So far the results remain extremely strong, but stock price reactions, in aggregate, have been less impressive.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, the latest US and international COVID trends including our vaccination trackers, and much more.

As mentioned above, AAPL is trading 1% lower in reaction to last night’s earnings report. Some may look at that weakness as a sign that the best of times are behind the stock, but we always caution against reading too much into one day’s action. Including last night, AAPL has handily topped EPS and revenue forecasts in each of its last five earnings reports, yet the stock is now on pace to have a negative one-day reaction to earnings for the fourth straight quarter. Last July, AAPL surged 10.5% on the day after its earnings report, but following the last three reports, the stock declined 5.6%, 3.5%, and -0.1%, respectively. Despite this current streak of negative reactions to earnings, though, the stock has rallied 57% over that same time span. Nobody knows what the future holds, but one day does not always make a trend.

Daily Sector Snapshot — 7/27/21

Home Prices Soar to New Heights

May 2021 S&P CoreLogic Case-Shiller home price numbers were released today, and they showed a continued surge in home prices all around the country. The month-over-month gains of 2-3% are similar to what we used to see on a year-over-year basis prior to COVID, but now the year-over-year gains all stand in the teens and twenties. At the top of the list is Phoenix which saw home prices rise 3.75% from April to May and 25.86% from May 2020 to May 2021. Below is a table showing MoM and YoY gains for the twenty cities and the composite indices tracked by S&P CoreLogic Case-Shiller.

Home prices have surged nearly uniformly across the country since COVID first hit. As shown below, since February 2020, the composite indices are up 18-19%, while most cities are up between 14% and 21%. Chicago and New York have seen a slightly smaller jump in prices than the rest of the country. Miami, LA, Portland, Charlotte, Dallas, Tampa, Denver, San Francisco, and Boston are all up between 19-21% since COVID. Three cities stand out for even bigger price jumps. As shown, Phoenix, Seattle, and San Diego are up quite a bit more than the rest of the group with gains between 28-30%.

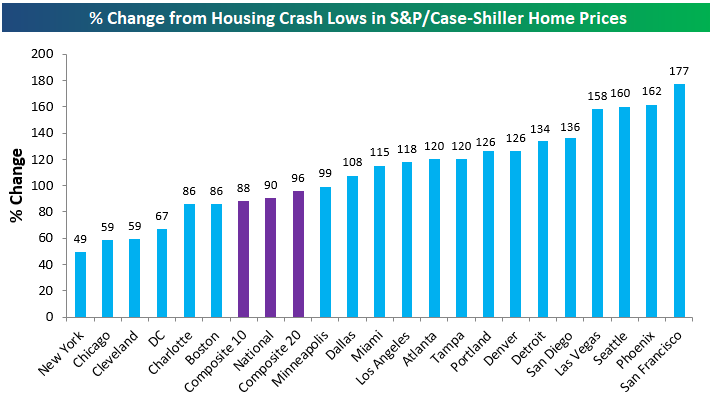

Below we show where home price levels are now versus their low-points after the mid-2000s housing bubble burst. Most lows for home prices were seen sometime between 2010 and 2012. As shown, the composite indices are now up 88-96% from their lows, while 13 of 20 cities are up more than 100% off of their lows. San Francisco is up the most at +177%, followed by Phoenix, Seattle, and Las Vegas (all up 150%+). At the other end of the spectrum, New York is up the least off its lows at +49%.

Notably, the post-COVID surge in home prices has left all but two cities above their prior all-time highs made during the mid-2000s housing bubble. Las Vegas and Chicago are the only two cities that have yet to eclipse their prior highs, but they’re now very close at just -1% and -3%, respectively. Miami, New York, and Washington DC are the three cities that have most recently made new highs.

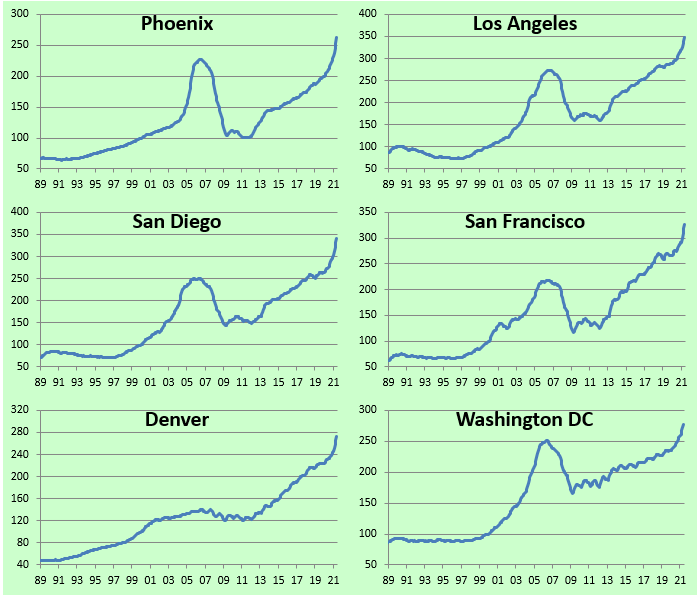

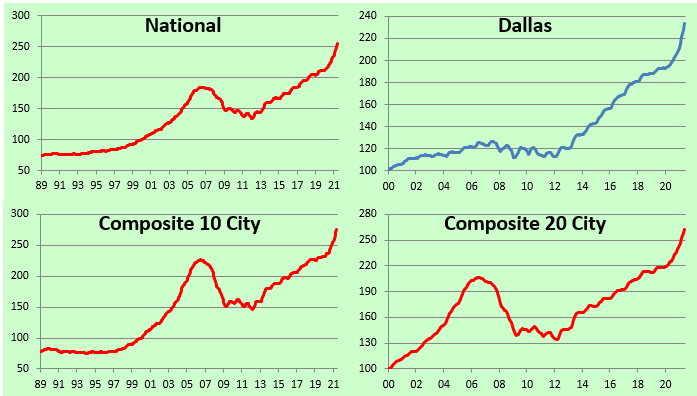

Below are charts showing historical levels of home prices across the S&P CoreLogic Case-Shiller indices. These really show how much prices have spiked post-COVID. Prices were already trending higher coming into the pandemic, but over the past 17 months, they look more like a rocket does at take-off than a passenger jet! Click here to view Bespoke’s premium membership options.

Source: S&P CoreLogic Case-Shiller

Bespoke Stock Scores — 7/27/21

Fifth District Manufacturing Flying

As we noted in our update of our Five Fed Manufacturing Composite featured in last night’s Closer, July regional Fed manufacturing indices have been showing broadly strong readings. The fifth and final Fed bank’s index released today out of, coincidentally enough, the fifth district added some fuel to the fire. The Richmond Fed’s composite reading was anticipating a 2 point decline from 22 last month. Instead, last month’s reading was revised higher by 4 points, and July saw another uptick to 27. That is the second-highest reading on record behind March 2008 when the composite came in a single point higher.

While the composite index as well as multiple other sub-indices like those for employment, prices, and inventories were at or just off of records, breadth in terms of the month-over-month changes was more mixed. Of the 17 sub-indices, 9 were higher, 1 was unchanged, and 6 were lower.

The area of the report to have seen the most significant deterioration in July was New Orders. The index fell 11 points to 25. Granted, that is coming off of a record high, and the July reading remained in the top 5% of all months. Order Backlogs also fell m/m although the decline was much smaller at only a single point. One interesting dynamic of the readings on Backlog of Orders is the difference between current conditions and expectations. Whereas the current conditions index is in the top 2% of all readings, the expectations component saw an 8 point decline and is now in the bottom decile of readings. Overall, while order growth decelerated, it is still running at a very strong clip.

As such, shipments were higher with that index rising 6 points to 21; the highest level since March. While shipments rose, there still appear to be significant disruptions to supply chains. Vendor Lead Times were unchanged in July just off of the record high from two months ago. While that reading has yet to see much improvement, the region’s businesses do seem optimistic that the lead times will improve but not necessarily return to normal down the road as expectations plummeted 12 points.

Given those supply chain disruptions, inventories continue to decline at record rates. The indices for both raw materials and finished goods fell to fresh record lows.

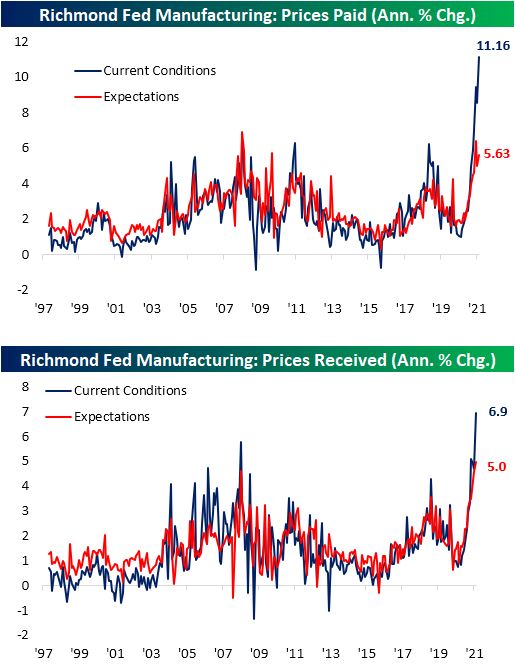

Meanwhile, unlike other regional Fed reports, prices paid have gotten little relief accelerating to an 11.16% annualized rate. Prices Received also rose to a record high of 6.9%.

In addition to input and final good prices, wages also came in at a record high alongside the index for Number of Employees. Forward-looking indicators point to continued strong labor demand going forward too as expectations for the Number of Employees also set a new record. Granted, that did not coincide with a record in the reading on wage expectations. In other words, higher pay has appeared to have enticed more workers but we are potentially hitting a limit on firms’ willingness (or ability) to pay higher wages. Additionally, alongside the higher wages and an increase in employment, there was an improvement in the Availability of Skills index which has been around record lows of late (meaning there has been a lack of candidates with necessary skills). Click here to view Bespoke’s premium membership options.

Chart of the Day: Hang Seng Two-Day Rout

Bespoke’s Morning Lineup – 7/27/21 – Now the Fun Starts

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Learn everyday, but especially from the experiences of others. It’s cheaper!” – John Bogle

Futures are indicated lower this morning as Chinese equities sink on continued fears of government crackdowns on that country’s tech sector. We’ve seen a bit of a bounce off the lows, though, as we get closer to the opening bell in the US. If that sounds familiar, it should since it was the exact same setup we had yesterday. While the issues in China are troubling for investments based in China, it should make US assets more attractive as capital flees that area of the world and looks for a safer home.

The week may have started off quietly yesterday, but the real fun begins today as there are not only a number of economic reports but some of the largest companies in the world will start releasing results. In the case of economic data, Durable Goods came in weaker than expected, but last month’s release was revised higher which somewhat netted this month’s weakness out. Later on today, we’ll get releases on Home Prices, Consumer Confidence, and the Richmond Fed Manufacturing sector.

On the earnings front, after the close, we’ll get reports from Alphabet (GOOGL), Apple (AAPL), and Microsoft (MSFT). On a combined basis, these three companies alone are expected to report combined revenues of about $175 billion! As if these three companies weren’t enough, we’ll also hear from Advanced Micro (AMD), Chubb (CB), Mondelez (MDLZ), Starbucks (SBUX), and Visa (V).

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, the latest US and international COVID trends including our vaccination trackers, and much more.

Yesterday was a big day for the crypto-currency markets, but Amazon’s denial that it would accept bitcoin payments by year-end has resulted in a giveback of some of those gains. Bitcoin’s rally yesterday also coincidentally (or not) stalled out right at the same levels it stalled out at in mid-June, so for people to feel more comfortable going forward, they’ll likely want to see prices trade and stay above $40,000.

In the case of ethereum it’s a similar story as the rally in ether stalled out right near $2,400 which is right where it stalled out earlier this month. The only difference between now and then is that while the last rally also failed at the 50-DMA, this time around, ether has still been able to hold above that level.