Sentiment Surge

Over the past couple of weeks, the S&P 500 has reversed higher, and the index is now only a few basis points away from the September 2nd closing high. With the rally, sentiment has taken a sharp turn towards optimism. The AAII reading on bullish sentiment rose for a second week in a row, climbing 9 percentage points to 46.9%. That is the highest reading on bullish sentiment since the week of July 1.

While this week’s increase was large, it comes on top of a double-digit rise last week. In total, bullish sentiment has climbed 21.4 percentage points in the past two weeks alone. That is the first time since November of last year that bullish sentiment has risen by at least 20 percentage points in two weeks. Going through the history of the survey, there have only been 17 other periods in which there were similar moves without another occurrence in at least six months. Overall, these instances have consistently seen the S&P 500 move higher in the following weeks and months with larger than normal average and median gains. That is except for one year out in which performance has been slightly worse than the norm.

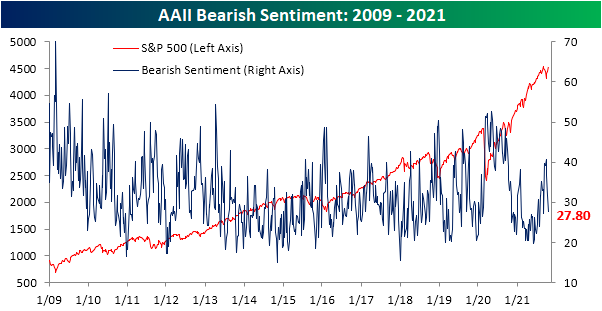

With the big jump in bullish sentiment recently, bearish sentiment has pulled back to 27.8%. That is the lowest reading since September 9th and the third week in a row in which bearish sentiment has moved lower.

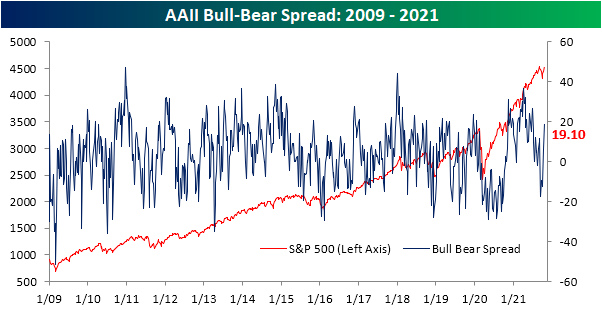

With inverse moves to bullish and bearish sentiment, the bull-bear spread stayed in positive territory for the second week in a row as bulls outnumber bears by the widest margin since the first week of July.

Big gains to bulls also borrowed heavily from neutral sentiment as that reading fell from 30.3% to 25.4%. Similar to bearish sentiment, that is the lowest reading since early last month.

As for some other readings on sentiment, the NAAIM Exposure index measuring investment managers’ exposure to US equities has also made a significant move higher this week. Readings in this index range from -200 to 200 where (-)200 would indicate responding managers are leveraged long (short), (-)100 would be fully invested long (short), and a reading of zero would be market neutral. At the end of last month, the reading fell to a low of 55 which was the weakest level since May. While the past two weeks only saw modest improvements, this week there was a surge all the way up to 98. The 33.6 point increase ranks as the fifth-largest week over week moves on record in the index dating back to 2006. Click here to view Bespoke’s premium membership options.

PUA Claims Negligible

Initial jobless claims made another move lower this week with the seasonally adjusted number falling by more than expected to 290K from an upwardly revised reading of 296K last week. That sets another record low for the pandemic era with claims now 34K above levels from March 14th of last year (the last reading before claims began to print in the millions).

On a non-seasonally adjusted basis, claims were again lower as is normal for the current week of the year. Historically, this point of the year is when claims tend to rise into year’s end, but the current week of the year provides a brief period of respite. Since 1967, the current week of the year has only seen claims rise week over week under a quarter of the time. While this week saw some seasonal tailwinds, PUA claims are increasingly a negligible factor as any backlogs are essentially worked off. Initial PUA claims came in at just 2K this week.

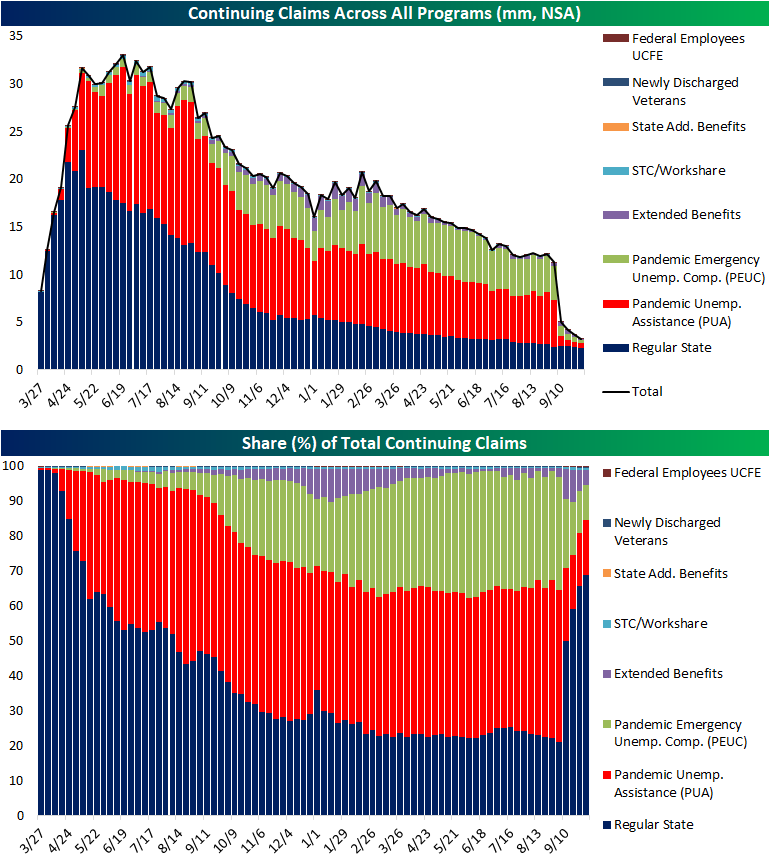

Continuing claims also set another pandemic low falling below 2.5 million.

The most recent data including all programs is through the week of October 1, and again there has been a substantial drop off in total claims thanks to the end of pandemic era programs. Total unadjusted continuing claims fell to 3.29 million down from 3.66 million the prior week. As could be expected, PUA, PEUC, and Extended Benefits programs were the main contributors to those declines leading regular state claims to once again account for a dominant share of total claims. Click here to view Bespoke’s premium membership options.

Chart of the Day: Earnings Update As Q3 Reporting Hits Higher Gears

B.I.G. Tips – Charts We’re Watching – 10/21/21

The Bespoke 50 Growth Stocks – 10/21/21

Bespoke’s Morning Lineup – 10/21/21 – Claims on Deck

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The problem is that a lot of big companies, process becomes a substitute for thinking. You’re encouraged to behave like a little gear in a complex machine. Frankly, it allows you to keep people who aren’t that smart, who aren’t that creative.” – Elon Musk

After a six-day rally of over 4%, the S&P 500 is indicated to open lower this morning along with the other major averages. The big drag on sentiment this morning is the 10-year yield which has spiked by about 4 bps in the last two hours taking yields to the highest level since May. Along with a busy slate of earnings, there are a number of economic indicators on the calendar that have the potential to swing things in the hours ahead. Jobless claims and the Philly Fed will be released at 8:30 AM while Leading Indicators and Existing Home Sales will hit the tape at 10 AM.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

With bitcoin hitting a new high this week, we wanted to update the comparison between ‘digital gold’ (bitcoin) and physical gold over the last year. Like bitcoin’s actual price, the ratio of bitcoin to gold also hit a new high this week topping the prior record high of 36.2 from April and finishing off yesterday at 37 ounces of gold to one bitcoin. That represents more than a six-fold increase in just the last year!

While bitcoin has been on a tear relative to gold, priced in terms of ether, it has underperformed over the last year. Last October, one bitcoin was worth more than 30 ether, but over the next six months that ratio rapidly compressed falling to as low as 12.3 this May. Ever since then, bitcoin and ether have been moving closer in tandem with each other as the ratio has been contained to a range between 12 and 18.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 10/20/21

Bespoke Baskets Update – October 2021

Road and Rail Soar Above Air Freight

One major economic trend of the past several months has been supply chain constraints including logistics issues. Now in the throes of earnings season, earnings of companies related to supply chains and logistics (whether that be people or parcels) are beginning to roll in with four such names reporting in the past day alone: Kansas City Southern (KSU), United Airlines (UAL), Marten Transport (MRTN), and Knight-Swift Transportation (KNX). In the table below, we show all the S&P 1500 Transportation Industry stocks that have reported since late September. Most of these stocks have beaten estimates on the top and bottom line with a few exceptions. While it is the one furthest in the rearview now, FedEx (FDX) was perhaps the worst of these missing EPS estimates and lowering guidance. KNX, on the other hand, reported a triple play this morning; one of the first companies to do so thus far in earnings season.

Two more transportation names, CSX (CSX) and Landstar System (LSTR), are also set to report earnings after the closing bell today, and over a dozen other names will follow up in the next week alone. These names could potentially be interesting areas to look for anecdotes regarding broader supply chain issues pressuring the economy, but turning to the stock price reactions, Saia (SAIA) has averaged the largest single-day gain on earnings averaging a 2.5% move across its 60 past earnings reports. Old Dominion (ODFL), Echo Global Logistics (ECHO), Hub Group (HUBG), and XPO Logistics (XPO) are the only others that have averaged greater than 1% gains in reaction to earnings. C.H. Robinson (CHRW) and Avis Budget (CAR), on the other hand, have historically averaged the worst reactions to earnings of this industry.

While there are still plenty of companies within the industry left to report providing plenty of catalysts for moves, since the closing low on September 30th, the transports have seen solid performance with an 8.79% gain through today. That move has not only lifted the industry above its 50 and 200-DMAs but it has also broken the downtrend that has been in place since the spring. Currently, the group is still down 6.1% from its 52-week high. Click here to view Bespoke’s premium membership options.