Surprise Headlines — 2022

As a thought experiment, the Bespoke team got together this week and brainstormed over what could be some of the most contrarian themes to emerge in 2022. Rather than going along with prevailing thought or consensus sentiment as we enter a new year, the made-up headlines below are a fun and lighthearted way of getting readers to think outside of the box. This is simply an attempt to provide a contrarian perspective, and these headlines are not – we repeat – are not – predictions or recommendations, but rather a way to hammer home the line from the famous 18th-century proverb that “the best-laid plans of mice and men often go awry.”

COVID pandemic becomes the COVID nuisance as CDC eyes new bug

After more than two full years in a pandemic environment, the SARS-Cov-2 virus is now viewed as nothing more than a common cold. The combination of vaccination, previous infections, and new treatments that inhibit the virus mean the United States has returned to pre-pandemic norms. Scientists at the CDC are now monitoring a new bird flu that is spreading across South America.

~~~

Americans celebrate sub-$3 gas just in time for July 4th weekend

Surging US shale patch drilling and an aggressive output slate from OPEC have sent crude prices tumbling into the $40s. With oil collapsing, American drivers are getting relief and inflation has slowed.

~~~

Fed fears unrealized as rates unchanged in 2022

Weaker than forecasted first half inflation led to patience in the middle of the year, while the slowdown in global growth and US employment kept feet off the breaks at the FOMC in the second half. With US growth slowing dramatically into 2023, it’s not clear when the central bank will tighten policy.

~~~

Little fish eat big sharks as investors ditch mega-caps in favor of small caps

Despite ongoing growth, multiple contraction for large tech names has left many to lag the explosive re-rating of small-cap stocks that are able to grow with the rest of the US economy. Small-cap strength recalls the early-2000s unwind of the last great tech bubble.

~~~

China back on the map as ADRs roar in spite of regulation

While Chinese authorities have made it harder for companies to list abroad amidst concerns over data security and social control, those that remain on US exchanges have had a stellar year. A return to growth in 2022 along with reduced concerns about outright bans on US listings has made Chinese ADRs one of the biggest winners this year.

~~~

Euro soars as post-COVID boom pushes ECB towards rate hikes

A newly-hawkish ECB concerned with surging economic growth and plunging unemployment has driven up the value of the euro relative to the dollar this year. Falling oil prices have also helped the energy import picture on the continent.

~~~

Move over sewer socialism, there’s a new left-wing development model in Latin America

The ongoing renewables build-out has sustained copper and lithium prices which are fueling a strong peso and rapid economic growth. After the election of Gabriel Boric late in 2021, Chilean assets were supposed to pay the price of a left-wing policy slate. But politics has proven indifferent to larger trends at work in the global economy.

~~~

Brazilian assets soar in spite of right-wing collapse

The re-election of former President Luiz Inácio Lula da Silva and defeat of right-wing incumbent Jair Bolsonaro has been a boon for Brazilian stocks as leftward tilt proved to be largely priced in ahead of the election.

~~~

Outflows doomed ARK Invest to a weak 2021, but strong 2022 performance has lured investors back

Investors soured on ARK Invest and its hyper-growth focus as billions flowed out of the ARK family of ETFs. But by the end of Q1 2022, those outflows reversed, and stock-picking performance has driven a dramatic recovery.

~~~

Chips collapse as normalcy lowers multiples amidst a pause in the global semis cycle

After semiconductor names could do no wrong in the wake of the COVID crisis, prices soared. Supply and demand have since normalized and inventories have surged, leading to the selloff that has played out this year.

~~~

Newer EV manufacturers pummeled by legacy brands as Ford and GM capture more market share

Tesla’s established production and the constant drumbeat of new electric vehicle releases from major Detroit OEMs has crushed the valuation and attention placed on newer entrants. Factory lines are humming and dealer lots are jammed with buyers not content to wait for the slow ramp-up at companies like Lucid, Rivian, or Lordstown.

~~~

Cable box is the comeback kid; streamers lose steam to traditional TV

Even with streaming experiencing rapid growth overall, the proliferation of services and options has many consumers returning to old-fashioned cable and the reliability it brings. Household formation has also attracted customers for broadband internet, fueling a surprise in the number of internet customers cable companies attract.

~~~

Buffett takes profits in Apple after valuation appears ‘lofty’ sending the stock lower

With iPhone growth slowing, Apple has re-rated from its 35x multiple to much more reasonable levels. The billions wiped off its market cap following the revelation that Buffett’s Berkshire Hathaway sold its entire position have compounded as the company struggles to answer metaverse innovation from competitors.

~~~

Meta stock soars after Zuck goes into hiding

In a marketing ploy seemingly lifted from young adult novel “Ready Player One,” Meta has successfully ginned up interest in its Metaverse platform with a dynamic competition for new users: a $10 million prize for whoever tracks down Mark Zuckerberg’s avatar first. Unlike its mega-cap tech peers, Meta’s stock has reached new heights in 2022 as its market cap approaches $2 trillion.

~~~

Democrats Ride Blue Wave to Bolster Majorities in House and Senate

After Covid burned out early in 2022 and oil prices dropped below $60 per barrel following a Q1 supply increase from OPEC+, increasingly confident consumers rewarded President Pelosi with firmer majorities in the House and Senate. Speaker Cortez and Majority Leader Sanders have pledged to hold a vote on Build Back Better before Thanksgiving.

~~~

Same old retailer, brand new optimism: how Bentonville’s finest is booming

Most of Wal-Mart’s business is still old-fashioned big-box retail, where results have been mixed this year. But tech-oriented partnerships designed to make the company more competitive with delivery and e-commerce apps are fueling growth and enthusiasm for one of the world’s largest companies.

~~~

All hail ride-hailing: UBER and LYFT soar as labor markets soften and riders return

With the fading burden of COVID, Americans are headed out for a night on the town, and they’re using ride-sharing to do it. The softening of labor markets with slower growth than expected is also making driver acquisition easier and improving take rates for the platform companies.

~~~

Forget Beeple and Bored Apes, collectors want Holden Caulfield and Gatsby

As interest has ebbed from NFTs, sneakers, and baseball cards, collectors are now flocking to rare first edition books with “fine” dust jackets. In the second half of 2022, first editions of 20th-century classics like Catcher in the Rye, To Kill a Mockingbird, and The Great Gatsby have shattered sales records.

~~~

Golden year for Gold

Still-low real rates have meant precious metals have turned in a big year. High inflation in 2021 didn’t help gold, but the reversal of planned rate hikes sent TIPS yields lower and boosted gold. Surging retail interest hasn’t hurt either.

~~~

Yen soars versus dollar amidst a booming Japanese export economy

As the dollar has dragged this year, the yen has gained, while Japanese exports have boomed. Normalizing natural gas prices and falling crude import bills have also served to flatter the Japanese balance of payments and added to the upward pressure on the yen that comes from a lower path of Fed hikes and flight in global risk appetite.

~~~

New Yorkers place bets on historic Jets/Giants Super Bowl

With both the New York Jets and New York Giants sitting atop their respective conferences as the 2022 season nears its end, a frenzy for 2023 Super Bowl tickets has emerged in the Big Apple.

(Okay, so maybe we’ve gone a little overboard with the Jets/Giants Super Bowl headline! That’s the biggest long shot of them all.)

Bespoke’s Morning Lineup – 12/31/21 – Like Shooting Fish in a Barrel (Sort of)

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Time sometimes passes quite quickly.” – Jimmy Page

With a decline into the close yesterday and modestly weaker futures this morning, US equities are limping into the close of 2021 after a strong year of gains. Maybe we would have all been better off if, like many countries in Asia and Europe, markets had decided to close today in observance of New Year’s Day tomorrow. Happy New Year!

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s been a pretty incredible run for the market this year. It may not sound impressive at first, but through the end of the day Thursday the S&P 500 traded higher on just under 57% of all trading days this year. To put that in perspective, in sports betting, it’s practically unheard of for any professional to have a consistent winning percentage of even 55%. Not only has the S&P 500 traded higher on nearly 57% of all trading days this year, but last year (2020) more than 57% of all trading days were positive, and the year before that (2019) the winning percentage was just over 59.5%!

With this year’s 56%+ winning percentage, the last three years rank as just the second time since 1945 that the S&P 500 was up on more than 55% of all trading days for three straight years. The only other similar streak was from 2004 to 2006 (55.56%, 55.95%, and 55.78%), but during that streak, not one of the three years was as consistent to the upside as any of the last three years. Outside of one of the most tumultuous five weeks in history back in early 2020, for most of the last three years, the market has been on cruise control. Hopefully, it doesn’t run into any speed traps in 2022.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Chart of the Day: Big Tech Balance Sheet Expansion

Small Caps vs Large Cap Spread When Yields Change

The recent underperformance of small caps has been partially attributed to rising current yields and assumed rate hikes in 2022. However, small caps have not historically always declined during periods when treasury yields have been on the rise. In fact, since 2000, the S&P 600 Small Cap Index has tended to outperform the S&P 500 during years when the 10-year yield rose. The first table below shows years when the 10-year yield increased, and for each year we also show the performance of the small-cap S&P 600 and the large-cap S&P 500. In the nine prior years where the 10-year yield increased, the S&P 600 outperformed the S&P 500 by an average of 6.0 percentage points (ppts) and a median of 3.6 over the course of the year with outperformance 70% of the time.

In the second table, we show years where the 10-year yield declined, and in those years small caps still outperformed but by a more modest 2.4 ppts (median: 0.2 ppts). This goes to show that not all small caps are negatively impacted by rates, but it is worth noting that the names in the S&P 600 tend to have positive earnings whereas the Russell 2000 has a larger number of unprofitable companies. The Fed has signaled multiple rate hikes in 2022, but based on historical trends it should not necessarily be interpreted as a negative headwind for small-cap stocks with positive earnings.

The worst year since 2000 for small caps relative to large caps was in 2019 when the group underperformed by 8.3 percentage points and in 2019, rates declined by 70 basis points. The best year for small caps on a relative basis was in 2000 when the 10-year yield dropped 148 bps and the S&P 600 outperformed the S&P 500 by 22.3 ppts. Click here to view Bespoke’s premium membership options.

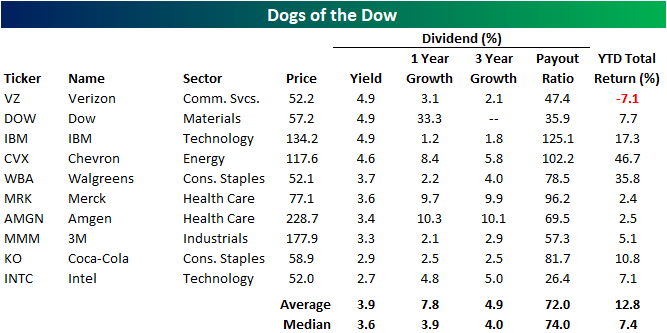

Dogs of Major Indices

The Dogs of the Dow is a popular hands-off investing strategy that says to simply buy the 10 stocks in the Dow Jones Industrial Average with the highest dividend yield at the end of each year. As we approach the end of 2021, below is a look at the ten Dow stocks that would currently make up the Dogs of the Dow for 2022. As shown, Verizon (VZ), Dow (DOW), and IBM top the list with dividend yields of 4.9%, while Coca-Cola (KO) and Intel (INTC) have the lowest yields of the Dogs at just under 3%. On average, the 10 Dogs have a yield of 3.9%, and they’re only up 12.8% so far in 2021. Notably, every member of this list has increased or maintained their dividend over the last three years.

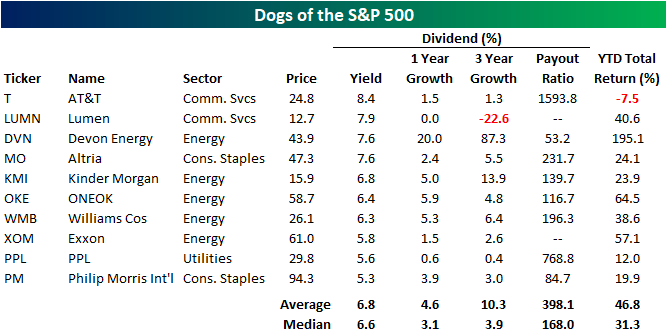

We thought it would be interesting to find the 10 “Dogs” of the S&P 500 and Nasdaq 100 as well. The table below shows the 10 highest yielding stocks in the S&P 500 at the moment. These ten stocks have an average dividend yield of 6.8%, and two of the ten are tobacco companies Altria (MO) and Philip Morris International (PM). It is worth noting that most of the members on this list have paid out more in dividends than they have taken in on a net income basis over the last twelve months, which seriously puts into question the sustainability of the dividend. And aside from AT&T (T) which is down 7.5% YTD, these stocks haven’t exactly been “dogs” when it comes to share-price performance recently. On a total return basis, these ten stocks have averaged a sizeable gain of 46.8% so far in 2021.

Below is a look at the ten highest yielding stocks in the Nasdaq 100 at the moment. While Nasdaq 100 names aren’t typically thought of as attractive dividend payers, these ten stocks have an average yield of 3.2% at least. That’s not much less than the average yield of 3.9% for the ten Dogs of the Dow. Kraft Heinz (KHC) is at the top of the list with a yield of 4.5%, but this stock has seen its dividend growth actually decrease over the last three years, and its payout ratio is pretty high at 85.1%. Four more names have yields between 3 and 4% — Gilead (GILD), Walgreens (WBA), American Electric (AEP), and Amgen (AMGN). Broadcom (AVGO) has the lowest yield of the 10 Nasdaq 100 Dogs, but it has increased its dividend by 23.6% over the last three years and by 10.8% over the last twelve months. Click here to learn about Bespoke’s premium research services where you can get more in-depth reports and analysis of markets.

Bespoke’s Weekly Sector Snapshot — 12/30/21

Breadth Disconnects

As we mentioned in today’s Sector Snapshot and yesterday’s Chart of the Day, breadth for the S&P 500 has ripped higher recently. In the charts below, we show the price and cumulative advance/decline (AD) lines for each of the eleven sectors and the S&P 500. The cumulative advance/decline line measures the daily number of advancers minus decliners within a sector or index over a given time frame. Bulls want to see this reading make new highs when the index or sector’s price makes new highs. Right now, every sector but Communication Services and Energy is seeing new highs in the cumulative AD line. Three sectors have seen their cumulative AD line make new highs this week even though the index’s price has not yet made a new high — Consumer Discretionary, Financials, and Industrials. That’s a hugely positive divergence. Click here to view Bespoke’s premium membership options.

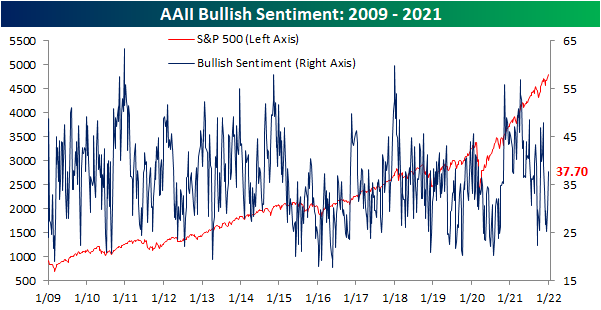

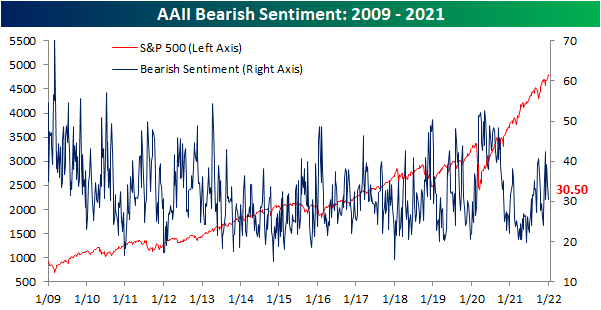

Bulls Bounce Back

Only two weeks ago, bullish sentiment according to the AAII had collapsed to some of the weakest readings of the post-pandemic period. Over the past two weeks, sentiment has gradually recovered with a significant pick up in this final week of the year. Now at 37.7%, bullish sentiment gained 8.1 percentage points this week for the largest increase since October. While recovered, the actual level of bullish sentiment is far from notable essentially in line with the historical average of 38%.

The increase in bullish sentiment over the past two weeks largely borrowed from bears. Bearish sentiment fell 3.4 percentage points in the most recent week following a 5.4 percentage point drop last week. Now at 30.5%, the share of respondents reporting as bearish is right in line with the historical average.

Given the inverse moves of the two readings, the bull-bear spread is now back into positive territory after five weeks of negative readings. At 7.2, the spread is not particularly elevated and only 0.2 points away from the historical average of 7.4.

Not all of the gains to bullish sentiment have come from former pessimists. The share of respondents reporting neutral sentiment has also unwound this week falling from 36.6% to 31.8%. That is the lowest reading since the first week of the month when exactly 31% of respondents reported neutral sentiment. Click here to view Bespoke’s premium membership options.

The Bespoke 50 Growth Stocks – 12/30/21

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were nine changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

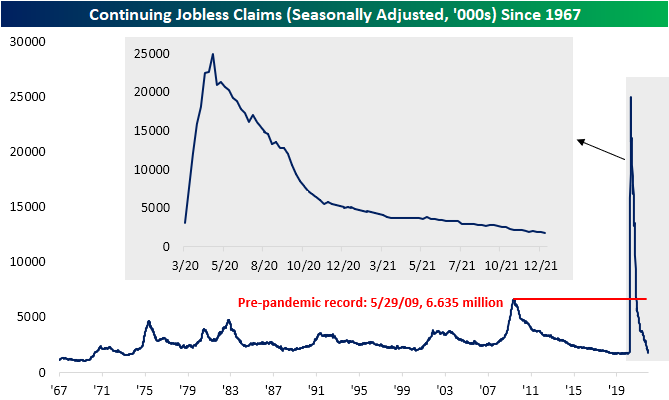

Sub-200K Claims Come Back

After holding above 200K the past two weeks, seasonally adjusted initial jobless claims dropped back below that level coming in at 198K. That compares to expectations of an unchanged reading from the revised level of 206K. While lower, claims remain above the multi-decade low of 188K from the first week of December.

On an unadjusted basis, claims were slightly higher rising by a little over 1K to 256.15K. With the continued unwinding of the program, PUA claims fell below 1K for the first time. Over the past few months, we have been noting the change in seasonal trends for initial claims. Historically, the final quarter has been marked by a period of rising claims whereas the opposite has generally been true in Q4 2021. The current week of the year, in particular, has seen claims rise over 90% of the time since 1967; ranking second behind the 27th week of the year (typically the last week of June/first week of July) as the week of the year that NSA claims most consistently increase on a week over week basis. While the rise in claims this week could have been expected, the uptick was much lower than normal as the current week of the year has averaged an increase of almost 50K. In other words, the trend in claims to close out 2021 has diverged from the normal trend.

Continuing claims saw a substantial drop this week with the adjusted number falling by 140K. That was the largest one-week decline since mid-October and the lowest level since the first week of March 2020.

Adding in all programs delays the data an extra week making the most recent reading as of the week of December 10th. That week saw regular state claims rise by over 93K to 1.828 million. Albeit higher, that was still below the levels from two weeks prior. Other programs similarly saw higher readings, but the Extended Benefits program provided a boost to the aggregate read on claims after being cut by 45.7%. At only 67.5K versus 124.3K, this program has now seen the lowest reading since July 2020. As expected headed into year-end, this is another point showing pandemic era programs continue to account for increasingly insignificant portions of jobless claims. Click here to view Bespoke’s premium membership options.