Meet the New Boss, Even Stronger Than the Old Boss

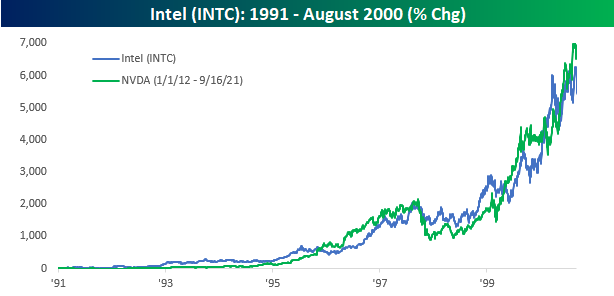

Back in the late 1990s, almost everyone had a similar story. They either had ‘this friend’ or knew someone who without a lot of financial background took a flier on a stock called Intel (INTC), held it for years, and became a millionaire in the process. Granted, these stories don’t seem as impressive nowadays with some people turning thousands into millions in a much shorter period of time, but at the time, the run in INTC was something dreams were made of. Looking just at the stock’s performance beginning in 1991 and through its peak in August 2000, INTC rallied nearly 6,300%. That’s a ten-bagger times six!

Despite semiconductors only becoming a bigger part of the economy in the most recent bull cycle, INTC has been a laggard relative to other semis over the last ten years. Hands down, the star of this cycle has been Nvidia (NVDA), and if we compare the performance of INTC from 1991 through the end of 2000 to NVDA now, there are a number of similarities. The first chart compares INTC’s performance in the 1990s through its August 2000 high to NVDA’s performance starting in 2012 and covering the same amount of time. As shown, both stocks followed very similar paths. Whereas INTC was up 6,300%, NVDA was up over 6,700%.

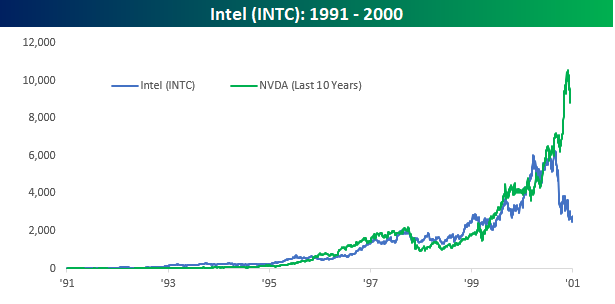

The last four months of 2000 were rough on INTC, though. From September through December 2000, INTC shares fell nearly 60%, cutting the nearly 6,300% advance down to 2,780%. Unlike INTC, though, NVDA has kept running. At its most recent high on 11/19, NVDA’s rally since the start of 2012 was 10,000% – or a hundred bagger! Since that peak, NVDA shares have pulled back just over 15%, taking its total gain down to ‘just’ 8,610%.

Not only were the last four months of 2000 painful for INTC, but the declines didn’t end there. 2001 and 2002 were also painful years for the stock, and by the time it bottomed in January 2003, INTC was down 79% from its August 2000 peak. Even after that low, INTC didn’t make much headway and actually made a lower low during the depths of the financial crisis, and it wasn’t until 2018 that INTC finally took out its highs from 2000. Just because INTC crashed and burned from its peak during the dot-com bubble after its epic run hardly means that this era’s star from the semiconductor sector will follow a similar path, and it’s not a bet we would make. However, the odds of any stock rallying more than 10,000% in the span of ten years are low enough, but the odds of one trading at over 60 times earnings that is already up 10,000% in ten years continuing that pace in the years ahead are even slimmer. Click here to view Bespoke’s premium membership options.

Inflation Concerns Surging

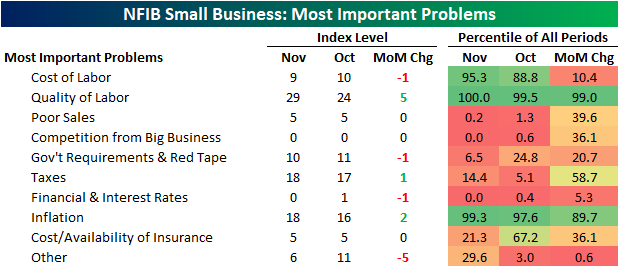

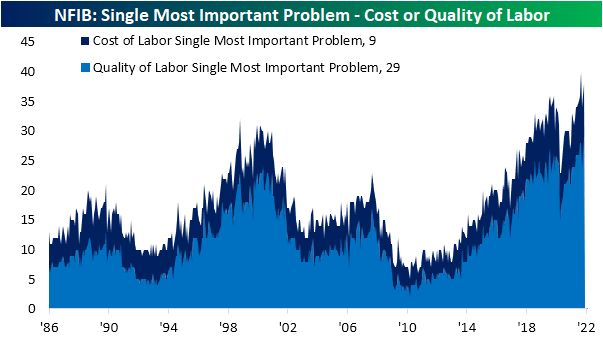

Small business sentiment picked up slightly in November with the NFIB’s monthly reading rising 0.2 points as expected. As for what businesses reported to be their biggest problems, as we noted in today’s Morning Lineup, labor concerns remain top of mind. A combined 38% of respondents reported either cost or quality of labor as their biggest issue. The former of which actually improved in November while the latter surged 5 percentage points. That was one of the largest one-month upticks to date and leaves it at a record high. Meanwhile, there have been been a couple of other indices hitting record lows: competition from big businesses and financial conditions and interest rates. Poor sales also came in the bottom 1% of readings.

While the largest share of companies see cost or quality of labor as a concern and the combined reading was higher versus October, that was still below the peak of 40% set in September.

Panning across the other problems, other than labor, inflation is the other key issue for small businesses. The percentage of respondents reporting inflation as their biggest issue has surged in recent months gaining another two percentage points to 18% in November. As shown below, the only other time in which as high of a share of respondents saw inflation as the biggest issue was in 2008. While there is not enough information to distinguish what the exact problems are, “other” also plummeted in November after a brief spike higher in October.

Pivoting back to inflation, the massive jump in November means it tied taxes as the second most important problem for small businesses. In the chart below, we show the rankings of those two series as well as the quality of labor (which is currently the most important problem) over the history of the survey. The surge in inflation’s importance is unprecedented in this data save for 2008 when it was briefly the most important problem. Click here to view Bespoke’s premium membership options.

![]()

Meme Stock Breakdown

There have been plenty of market happenings and themes in 2021 but perhaps one of the more intriguing ones was the recurring bouts of meme stock mania. The first of these was the massive short squeeze in shares of GameStop (GME) in the first month of the year which pulled other highly shorted names higher along with it. One of those other stocks was AMC Entertainment (AMC) which would later become the poster child for another string of outperformance of heavily shorted names. In the time since then, these stocks have generally trended sideways maintaining huge gains on the year, but they are also well off their highs. And in the past few days, these stocks have fallen below support and below the past several months’ ranges.

Checking up on highly shorted stocks, last Thursday the latest short interest data through the end of November was released. As shown below, of the Russell 3,000 stocks, Prelude Therapeutics (PRLD) currently has the highest level of short interest with 85.67% of shares sold short. Couchbase (BASE) is the only other stock with over half of shares shorted. BASE is a very new stock, though, debuting in July, after the GME and AMC short squeezes. The same can be said for stocks like Xometry (XMTR), Torrid (CURV), and Verve Therapeutics (VERV). For the most part, the stocks that are currently the most heavily shorted are down dramatically on the year and since the short squeeze peaks/meme stock manias of earlier this year (1/26 for GME and 6/2 for AMC). The only one of the top 20 most heavily shorted stocks that is up year to date is Gogo (GOGO) with a 33.44% gain.

Notably, those aforementioned meme stocks no longer find themselves high up on the list of the most heavily shorted stocks. In fact, of all Russell 3,000 members with 10% of float sold short, GME ranks as the 396th most heavily shorted today whereas it was by far the most shorted at the start of the year when 144.34% of shares were sold short. Given that decline, it is the stock that has seen the largest drop in short interest year to date. Dillard’s (DDS), BigCommerce (BIGC), and Ligand Pharma (LGND) have also seen drops of more than 50 percentage points in short interest as a % of float. While there have been some huge declines in short interest, not all are necessarily a result of a short squeeze. For example, Acutus Medical (AFIB) and American Well (AMWL) have both seen a consistent grind lower this year that have left them with single-digit prices and year-to-date declines of 89% and 75%, respectively.

Turning to the opposite end of the spectrum, in the table below we show the stocks that have seen short interest rise the most since the start of the year. PRLD is at the top of the list with a 67.46 percentage point increase. The next highest is Skillz (SKLZ) which has risen 37.82 percentage points. For the most part, these stocks that have seen short interest climb the most are down big on the year. There are a handful of exceptions though with Citi Trends (CTRN), AerSale (ASLE), Fisker (FSR), Big 5 Sporting Goods (BGFV), and Independence Realty Trust (IRT) having seen double digit percentage point jumps in short interest following big gains upwards of nearly 90% this year. Click here to view Bespoke’s premium membership options.

Bespoke Stock Scores — 12/14/21

Chart of the Day: Investors Flock to Safety

Bespoke’s Morning Lineup – 12/14/21 – PP-High

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Theory is splendid but until put into practice, it is valueless.” – James Cash Penney

Futures are lower across the board this morning, but the only index that is down of any significance at this point is the Nasdaq. The big report of the morning was November PPI and at the headline level, it came in stronger than expected rising 0.8% versus forecasts for an increase of 0.5%. Ex food and energy, producer prices were also higher than expected rising 0.7% compared to forecasts for an increase of 0.4%. As one might expect, the initial reaction in futures was weaker equities and higher yields.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Both the Nasdaq 100 and the S&P 500 have been treading water as both indices are at the same levels now that they were at more than a month ago. For QQQ, the high water line is currently at just over $400 a share. It briefly broached that level in mid-November for two days but could not hold those levels before pulling all the way back to its 50-day moving average. Last week, QQQ approached the $400 level again before selling off yesterday. For SPY, resistance has been even more pronounced at the $470 level. It has now tested that level three separate times since early November but has run out of momentum each time. There’s nothing wrong with equities treading water after big upside rallies, but hopefully, they have the strength to stay afloat.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 12/13/21

Chart of the Day: Economic Sentiment Weakens

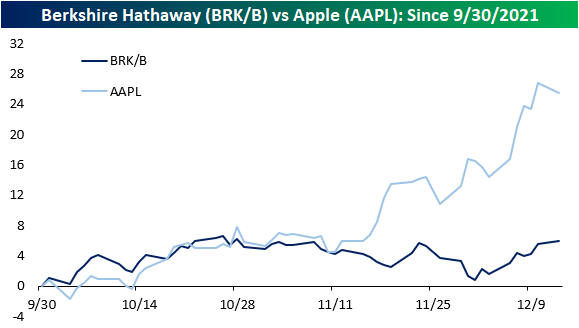

Berkshire’s Apple (AAPL) Weighting Swells to Nearly 50%

The Oracle of Omaha is known for weathering storms and emerging stronger after market pullbacks. In March of last year, we highlighted the fact that Buffett’s portfolio was seeing declines in line with the broader market, and the legendary investor seemed just as hurt as other market participants. Even though Buffett’s strategy of “be greedy only when others are fearful” has historically been a successful one, he did not aggressively buy the COVID-related dip, and the company now has record amounts of cash stockpiled on its balance sheet.

Although Berkshire Hathaway (BRK/B) has almost $150 billion in cash, the company’s portfolio has still performed strongly. Below is a look at Berkshire’s 20 largest equity holdings as of today based on reported holdings at the end of Q3. (This doesn’t take into account changes that may have occurred since the end of Q3 since Berkshire doesn’t have to report holdings again until early 2022.) Berkshire’s position in Apple (AAPL) has swelled to nearly 50% after the stock’s 28.5% gain so far this quarter! Berkshire’s next largest holding all the way down at 13.3% is Bank of America (BAC), which is up 3.4% QTD. American Express (AXP) and Coca-Cola (KO) rank 3rd and 4th with weightings of 7.5% and 6.9%, respectively. Only a handful of other companies have weightings above 1%: Kraft Heinz (KHC), Moody’s (MCO), Verizon (VZ), US Bancorp (USB), DaVita (DVA), Bank of NY Mellon (BK), General Motors (GM), and Chevron (CVX).

Quarter-to-date, Berkshire’s portfolio (as it stood on 9/30/21) would be up 13.9%, and that’s due largely to Apple’s 28.5% gain so far in Q4. Seven of Berkshire’s twenty largest holdings are in the red so far this quarter, with Charter (CHTR) down the most at 17.2%.

AAPL now makes up almost half of the overall Berkshire equity portfolio (and a quarter of the company’s market cap), which means that Berkshire Hathaway should be correlated to the performance of AAPL. Although the two equities have a semi-strong relationship over the last year with a correlation coefficient of 0.46, the correlation in Q4 has dramatically decreased. Since 9/30, the correlation coefficient is only 0.12, which implies only a very small correlation. Whereas AAPL has traded over 28.5% higher in Q4, BRK/B has only appreciated by about 6.5%. While AAPL shareholders have been rewarded so far in Q4, the stock of one of AAPL’s largest holders has lagged the S&P 500. Click here to view Bespoke’s premium membership options.

Strange Bedfellows: Technology, Energy, and Consumer Staples Lead

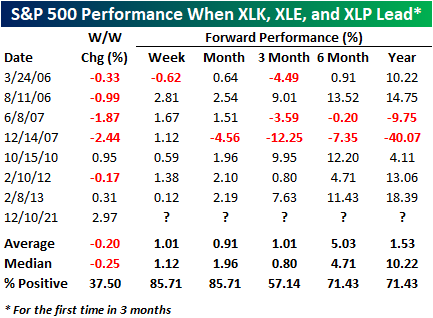

Technology (XLK), Energy (XLE), and Consumer Staples (XLP) tend to trade quite differently from each other for a variety of reasons. The Consumer Staples sector tends to be more defensive in nature as spending on the ‘essentials’ tends to hold up better in times of uncertainty than spending on more cyclical goods. XLE is largely levered to the price of energy commodities but also acts as an inflation hedge. Technology, meanwhile, tends to do best in a bullish tape as investors gravitate towards sectors with the brightest growth prospects. Because these sectors have different exposures, it is uncommon to see weeks like last week where these three sectors top the leaderboard for a given week. In fact, this has only occurred 9 times since the start of 2000, and two of those occurrences were in back-to-back weeks at the end of 2007.

In the table below, we show each of the prior weeks that Technology (XLK), Energy (XLE), and Consumer Staples (XLP) were the three top-performing sectors (without a prior occurrence in the last three months) along with the S&P 500’s performance over the last following week, month, three months, six months, and one year. In more than half of the prior eight occurrences, the equity market was lower during weeks when this occurred, and in the two prior weeks where the S&P 500 was higher, it was up less than 1%. In other words, there has never been a week like the last one where the S&P 500 was up close to 3% and these three sectors topped the leaderboard. After the eight prior occurrences, the S&P 500 was consistently higher one week and one month later with positive returns six out of seven times. Moving further out, though, the consistency of positive returns was less. In fact, three months later, the S&P 500 was only higher four out of seven times, while six and twelve months later it was higher five out of seven times.

Somewhat ominously, the worst forward returns came after the occurrence almost exactly fourteen years ago in December 2007 when the S&P 500 went on to decline 40% in the following year. One difference between that period and last week, though, was that instead of those three sectors leading the market in a week where the S&P 500 was up over 2%, in that week the S&P 500 was down over 2%. Click here to view Bespoke’s premium membership options.