Bespoke Brunch Reads: 1/16/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Politics

Flush With Cash, California Has Problems That Are No Quick Fix by Christopher Palmeri, Romy Varghese, and Laura Curtis (Bloomberg)

California has a budget surplus of nearly $50bn, California has lots of money to throw at a range of priorities which are steadily mounting, including homelessness and climate vulnerability. But lager problems, like a falling population and drought. [Link; soft paywall]

Women Legislators and Economic Performance by Thushyanthan Baskaran, Sonia R. Bhalotra, Brian K. Min, and Yogesh Uppal (SSRN)

The authors find areas that elect women to state legislative assemblies enjoy higher economic growth, with lower criminality and corruption, higher effectiveness, and lower political opportunism than their male counterparts. [Link]

Scarcity

A Simple Plan to Solve All of America’s Problems by Derek Thompson (The Atlantic)

Many of the economic problems of the last two years can be traced back to a failure to create abundance, which is easily attainable given American technology and productivity, but has not been the focus of policymaking or investment. [Link; soft paywall]

Supply-Chain Issues Leave New Homes Without Garage Doors and Gutters by Nicole Friedman (WSJ)

The ever-rising number of uncompleted homes is being driven by bottlenecks for a relatively small and inexpensive number of components which are preventing final completions of mostly-constructed new units. [Link; paywall]

COVID

Coronavirus Can Persist for Months After Traversing Body by Jason Gale (Bloomberg)

A new study reviewing autopsy results for 44 patients who died after contracting the virus reveals how serious infections can let the virus in to every one of the body’s organ systems. [Link; auto-playing video, soft paywall]

Cannabis compounds stopped COVID virus from infecting human cells in lab study by Kanoko Matsuyama (Fortune)

A new study shows that two different compounds fund in hemp may prevent COVID from entering in to human cells, making them a potential treatment for the disease. [Link; soft paywall]

Multiple Sclerosis

Longitudinal analysis reveals high prevalence of Epstein-Barr virus associated with multiple sclerosis by Bjornevik et al (Science)

A landmark study of US military personnel identifies the Epstein-Barr virus (which causes mononucleosis) as an extremely likely cause of multiple sclerosis. The study shows a 32-fold increase in risk of developing MS after infection with Esptein-Barr. [Link; paywall]

Trucks

Tesla Cybertruck Is Delayed Again, This Time Indefinitely by Nick Yekikian (Edmunds)

After being announced in 2019, Tesla expected its pickup truck to start deliveries by the end of 2021. But now the company has removed references to 2022 deliveries from its site, and nobody knows when the actual release will come. [Link]

Extreme RVs Grow Bigger, Bolder With Younger Consumers by Hannah Elliott (Bloomberg)

Glamping, meet tramping: adventure-seeking younger car buyers are leaving civilization and buying increasingly large and well-equipped vehicles to do it. [Link; soft paywall]

Fads

These TikTok Stars Made More Money Than Many of America’s Top CEOs by Josephy Pisani and Theo Francis (WSJ)

The highest-paid personalities on Tik Tok earn tens of millions per year, making them much better-paid than most large publicly traded companies. [Link; paywall]

Wordle Is a Love Story by Daniel Victor (NYT)

A once-a-day word guessing game has exploded in popularity, turning an idle side project for a Brooklyn software engineer into an obsession for hundreds of thousands of users. If you’d like to try your luck, you can play the game here. [Link; soft paywall]

Investors are paying millions for virtual land in the metaverse by Chris DiLella and Andrea Day (CNBC)

Real estate in the metaverse is selling for millions as investors eagerly anticipate a gold rush of users into virtual environments. [Link]

Economics

Don’t Extrapolate From This Fake Business Cycle by Dario Perkins (TS Lombard)

An argument that the data on the current economy is totally unique, with convincing arguments as to why the pandemic era is not a good indicator of longer-term economic trends or trajectories. [Link]

Climate Change

The 100th Meridian, Where the Great Plains Begin, May Be Shifting by Kevin Krajick (Columbia Climate Society)

The barrier between the humid, fertile east and the arid, dry west has historically run north-south along the 100th meridian. But desertification and climate change may be starting to shift that divide to the east, changing crop yields and drying out the plains. [Link]

Network Effects

Why Apple’s iMessage Is Winning: Teens Dread the Green Text Bubble by Tim Higgins (WSJ)

Younger mobile users fear being branded with the green bubble, illustrating the extremely strong network effects of the iMessage and broader iOS ecosystem Apple controls. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report Newsletter – 1/14/22 – The Fed Versus Growth

This week’s Bespoke Report newsletter is now available for members.

In The Bespoke Report this week we discuss the huge rotation out of growth and in to value stocks, preview earnings season, discuss the “buy-the-dip” mentality from US markets, review valuations, discuss the drivers of emerging markets outperformance, highlight the divergence between stock prices and analyst estimates by sector, review economic data from the US and around the world this week, and more.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 1/14/22

B.I.G. Tips – Retail Sales On the Path to Reality

Bespoke’s Morning Lineup – 1/14/22 – And They’re Off

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When you expect things to happen – strangely enough – they do happen.” – J.P. Morgan

If you were hoping for a quick bounceback following yesterday’s decline, think again. While futures were higher overnight, all of those prior gains have evaporated. Tech is leading the way lower once again, but Financials aren’t providing any support as investors have generally been selling JP Morgan (JPM), Wells Fargo (WFC), Citigroup (C), and Blackrock (BLK) following their reports. The only one of those four that’s higher this morning is WFC, while JPM and C are both down over 4%. As noted in our Earnings Season Preview yesterday, the major financials typically react negatively to their Q4 reports, so far this earnings season doesn’t appear to be an exception.

It may be Friday, but it’s a relatively busy day for economic data to close out the week with Retail Sales, Import and Export Prices, Industrial Production, Capacity Utilization, Business Inventories, and Michigan Confidence all on the calendar. Retail Sales just hit the tape and came in much weaker than expected.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Yesterday was a gut punch for the technology sector. Take semiconductors, for example. Boosted by a strong earnings report from Taiwan Semiconductor (TSM), the Philadelphia Semiconductor Index (SOX) traded more than 2% higher in early trading but then reversed lower finishing right near its low of the day and down more than 2% from Wednesday’s close. That marked the first time the index was up 2%+ intraday but finished the day down more than 2% from its prior day close since April 2020.

In the entire history of the SOX dating back to the mid-1990s, there have only been 42 prior occurrences where it was up 2%+ intraday but finished the day down 2%+, and only three of those occurred in the post-Global Financial Crisis period. As shown in the chart below, the majority of the prior occurrences came during the unwind of the dot-com bubble from March 2000 through October 2002. What makes yesterday’s reversal unique is that even after the decline, the SOX is still just 6.3% below its 52-week high. The average distance from their respective 52-week highs of the other 42 occurrences was over 40%, and there wasn’t a single time where the SOX was as close to a 52-week high as it is now. The only other occurrence where the SOX was even within 10% of a 52-week high was on 3/14/00.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke 50 Growth Stocks — 1/13/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were twelve changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Weekly Sector Snapshot — 1/13/22

Chart of the Day: International Revelations

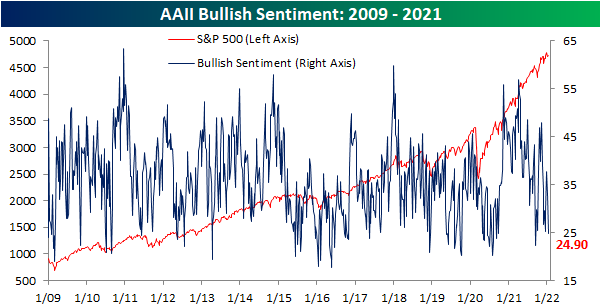

Bulls Back Off

The past week has seen the S&P 500 pull back to retest its 50-DMA which has put a dampener on investor sentiment. This week’s AAII survey showed that less than a quarter of respondents reported bullish sentiment. That is down from 32.8% last week and the lowest since 9/16.

Bearish sentiment picked up most of the difference rising five percentage points to 38.3%. This brings bearish sentiment to a fairly elevated level relative to its historical average of 30.56%, though, it is still within a standard deviation of that reading. While higher, this week’s increase was actually only the biggest uptick and highest level of bearish sentiment since the week of 12/16.

Given those moves in bullish and bearish sentiment, the bull-bear spread has fallen deeper into negative territory. At -13.4, the spread is now at the lowest level since mid-December.

Whereas bearish sentiment jumped 5 percentage points this week, neutral sentiment has gained 5 percentage points after the back-to-back increases over the past two weeks. Neutral sentiment now stands at 36.8% which is the highest level since 12/9.

As for other sentiment readings, both the Investors Intelligence survey and NAAIM Exposure index took more bearish tones in the most recent week. As a result, our Sentiment Composite, which combines the bull-bear spreads of the AAII and Investors Intelligence surveys with the NAAIM exposure index’s reading, has fallen back below zero meaning overall sentiment is broadly bearish, but not to a degree in which it is outside the range of recent readings. Click here to view Bespoke’s premium membership options.

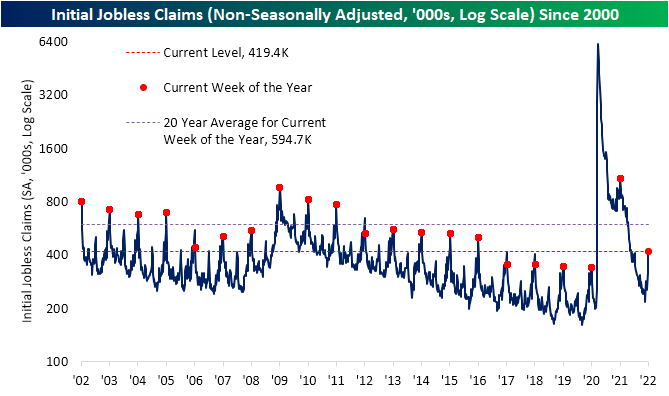

Seasonal Peak in Claims

After hitting multi-decade lows at the beginning of December, initial jobless claims have been on the rise with the most significant increase in that time occurring in the latest week. The seasonally adjusted reading increased by 23K to 230K this week which is the highest level since the week of November 12th. While there has not been much improvement in claims in the past month, current levels are still right around those from just before the pandemic. On a longer-term basis, these readings are also some of the strongest since the early 1970s.

On a non-seasonally adjusted (NSA) basis, the current week of the year typically marks a seasonal peak in claims. In fact, the current week of the year has historically seen claims rise 85.2% of the time week over week. As such, NSA claims surged over 100K this week from 315.8K to 419.4K. In spite of that seasonal headwind alongside the additional issue of rising COVID cases—which we cannot parse out how much each factor is contributing to the rise in claims—that was actually slightly below the average weekly change of 111.6K for the current week of the year. Of course, the current level of claims is a major improvement from where things stood this time last year, but it is still decently above levels from comparable weeks of the few years prior to the pandemic. Assuming this week marks the seasonal high as it has in the past, claims will now have tailwinds combating any COVID headwinds in the coming months.

Although initial claims were somewhat disappointing this week, seasonally adjusted continuing claims were very strong coming in at the lowest level since the week of 6/1/73. Claims by this measure are delayed an extra week to initial claims, but the most recent reading for the last week of 2021 showed only 1.559 million claims. The 194K week over week decline was the largest since mid-October when the reading fell by 241K. Click here to view Bespoke’s premium membership options.