Heard on Conference Calls: Q4 Earnings Season

Below are some of the most interesting quotes pulled from our Conference Call Recaps since the start of the Q4 earnings season:

Supply Chain/Inflation

- According to Apple CEO Tim Cook, the logistics environment “is very elevated in terms of the cost of moving things around. I would hope that at least a portion of that is transitory, but…the world has changed.”

- In regards to supply chain issues, Intel CEO Pat Gelsinger added, “As we predicted, these ecosystem constraints are expected to persist through 2022 and into 2023, with incremental improvements over this period.”

- Tesla CEO Elon Musk stated, “In 2022, [the] supply chain will continue to be the fundamental limiter of output across all factories. So, the chip shortage, while better than last year, is still an issue.”

- Although Johnson & Johnson reported solid results, multiple segments were negatively impacted by “raw material availability” and “supply chain constraints,” according to CFO Joseph Wolk.

- 3M CEO Mike Roman commented, “we’re going to see a volatile environment in the first half of 2022. Things should get better in the second half, but I would not expect a big snap back on stability of supply in 1Q of 2022.”

- Procter & Gamble CEO Jon Moeller pointed out that “Higher commodity and freight cost impacts combined were a 460 basis points hit to gross margins.”

- Moeller continued, “Transportation and labor markets remain tight, availability of materials remain stretched in some categories and in some markets, inflationary pressures are broad-based with little sign of near-term relief.”

COVID related

- The Netflix management team blamed “COVID overhang and macro-economic hardships in several parts of the world like LATAM” as a factor hindering growth.

- Intuitive Surgical reported that “COVID-19 has had, and will likely continue to have, an adverse impact on the company’s procedure volumes.”

- United Health CFO John Rex commented, “In the most recent weeks inpatient hospitalization levels for our members are similar to the January 2021 levels, even with national COVID case rates about 4x higher.”

Technological Development

- In terms of the metaverse, Microsoft CEO Satya Nadella commented, “And as the digital and physical worlds come together, we are seeing real enterprise metaverse usage, from smart factories to smart buildings to smart cities.”

- Nadella continued, “As every company becomes a digital company, they will need a distributed computing fabric to build, manage, secure and deploy applications anywhere.”

- American Express aims to stay at the “leading edge of technology and digital payment solutions to make American Express an essential part of our customers digital lives,” as per CEO Stephen Squeri.

- In November, Netflix unveiled its mobile gaming experience globally, which allows members to “discover and launch games from within the Netflix mobile app.”

- Tesla CEO Elon Musk believes that “over time, we think Full Self-Driving will become the most important source of profitability for Tesla”.

Broader Economy

- American Express is forecasting “higher than long-term aspirational levels of revenue growth” through 2023 due to elevated levels of consumer spending, according to the investor presentation.

- Union Pacific EVP Kenny Rocker stated that the company “will face continued challenges in our energy-related market.”

- In regards to the energy market, Baker Hughes CEO Lorenzo Simonelli added, “As we look ahead to 2022, we expect the pace of global economic growth to remain strong although slightly moderate compared to 2021. We believe the broader macro recovery should translate into rising energy demand for 2022 and relatively tight supplies for oil and natural gas.”

- Simonelli continued, “growth rates are likely to moderate from 2021 levels as central banks are expected to begin tightening monetary policy in order to reduce COVID-related stimulus plans and quell growing inflationary pressures.”

- Automatic Data Processing CFO Don McGuire commented, “a gradual ongoing recovery in labor force participation will support job growth in the first half of the year.”

- Boeing CEO David Calhoun referenced the international markets, stating, “Recovery continues broadening in Europe and South America [but] further lockdowns have stagnated recovery in China.”

In summary, management teams anticipate operating in a continued inflationary environment, but the supply chain constraints are expected to ease in the back half of 2022. Since COVID emerged, there has been an increased focus on digitization, which certain companies are attempting to capitalize on. In regards to the energy market, supply is expected to remain tight while demand strengthens, thus implying a higher price point for related commodities.

To stay up to date with Corporate America’s rhetoric, become an Institutional Subscriber today to get full access to our Conference Call Recaps. Click here to view a sample of the conference call recaps that you would be receiving on a daily basis during earnings season.

B.I.G. Tips – What Does Bearish Sentiment Imply for the S&P 500?

Bespoke’s Morning Lineup – 1/28/22 – No Support

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’m only rich because I know when I’m wrong.” – George Soros

Markets are flipping the script this morning as the pattern of futures overnight and into this morning has been the complete opposite of the pattern Wednesday night into Thursday morning. Whereas futures traded lower most of the night Wednesday and rallied into the open, overnight futures were positive but started to aggressively sell-off after Europe opened. Geopolitical events are a major issue weighing on sentiment as President Biden reportedly told Ukrainian President Zelensky that a Russian invasion was ‘virtually certain’ even as Zelensky has asked Biden to tone down the rhetoric and ‘ calm down the messaging’.

It may be Friday, but there are some important economic data on the calendar. The Employment Cost Index, Personal Income, and Personal Spending all just hit the taps while Michigan Confidence will hit the wires at 10:00. In terms of the reports already released, the Employment Cost Index rose slightly less than expected while Personal Income saw a smaller than expected increase and Personal Spending dropped right in line with forecasts (-0.6%).

As we have noted throughout the last several trading days, futures have done a terrible job at predicting market direction lately, so there’s a good chance that by the time the closing bell rings, things will look different than they do now.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The S&P 500 is currently down just over 10% from its recent record highs in what has been a relatively rapid deterioration in equity markets. In the span of just two weeks, the S&P 500 tracking ETF has given up both its 50-day and 200-day moving average (DMA), and neither level provided anything in the way of support. The next level to watch is the lows from last fall, and that level may not even hold through the end of the day.

While the 50 and 200-DMAs for SPY didn’t provide much in the way of support, on Wednesday’s first attempt to rally back above the 200-DMA, it acted as resistance. In Wednesday’s trading, the S&P 500 opened higher and briefly rallied above the 200-DMA but faded throughout the trading day. Just as the 200-DMA tends to provide support in an up-trending market, it tends to act as resistance during downtrends, so until SPY can rally back above its 200-DMA, the burden of proof is on the bulls.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

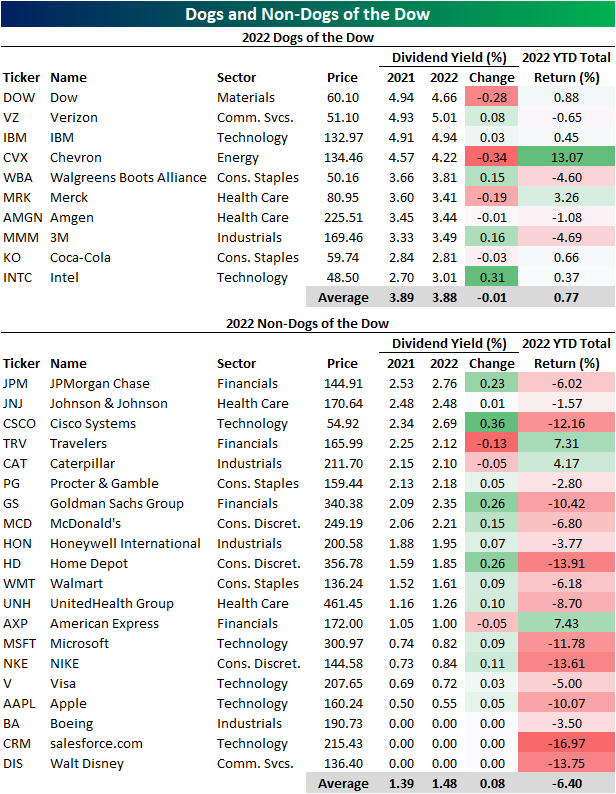

Dogs of the Dow Dominating

At the end of last year, we highlight the performance of the “Dogs of the Dow” in 2021. The Dogs of the Dow is a simple strategy that says to buy the ten highest yielding stocks in the Dow at the end of each year. In 2021, the Dogs underperformed, but so far in the new year, the complete opposite is true. As shown below, a little more than half of the Dogs are in the black year to date compared to only three (of twenty) non-dogs that are positive.

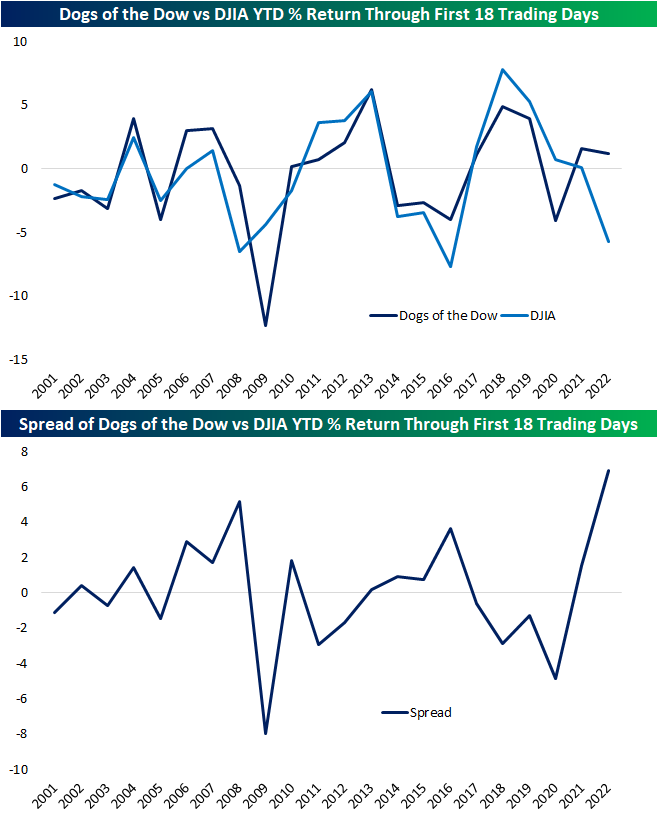

Taking a look at an index of the Dogs of the Dow going back to 2001, this year has marked the widest gap in returns between the Dogs and the broad Dow 30 through the first 18 trading days of the year. The only year that comes anywhere close to the gap in performance was 2008, and unlike this year, back then the Dogs were in the red at this point of the year. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – Wild Intraday Swings Continue

Daily Sector Snapshot — 1/27/22

The Bespoke 50 Growth Stocks – 1/27/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were ten changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

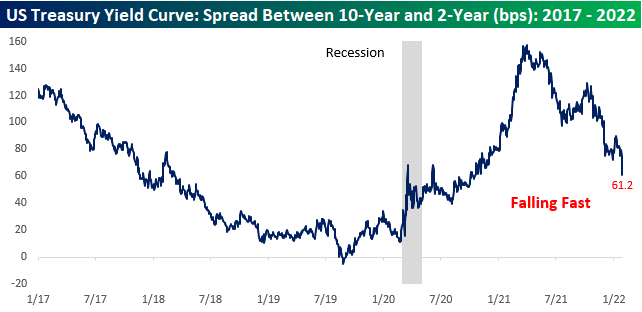

Yield Curve Goes Flat

Even as the FOMC is still adding to its balance sheet, hawkish commentary from Powell and company has caused massive moves in the fixed income market resulting in a massive flattening of the yield curve. Today alone, the spread between the yield on the 10-year and 2-year US Treasuries has narrowed by nearly 10 basis points (bps). Even more extreme, is the fact that over the last three months the curve has flattened by more than 50 bps from well over 100 bps to just over 60 bps.

Looking at the three-month rate of change in the yield curve, it hasn’t flattened this fast in at least five years. Last summer, we saw a similar but not as severe of a move.

Taking a longer-term look, flatter yield curves aren’t necessarily a negative economic signal, but there is an inverse relationship between the level of the yield curve and recession concerns i.e., the flatter the curve gets the more the market starts to price in the odds of a recession. As shown in the chart below, every recession since the late 1970s has followed an inversion of the curve.

In terms of the pace of flattening in the 2s10s curve, the current pace has been the swiftest since January 2015, and longer-term, there haven’t been a whole lot of periods where the curve flattened at a faster rate. Looking on the bright side, though, a rapid flattening of the yield curve by itself has not been a siren song for an impending recession. As shown in the chart below, there have been numerous times over the last 40 years where the curve steepened by as much (red line) or more than it has in the last three months and the economy was nowhere near a recession. Click here to view and sign up for Bespoke’s premium membership options.

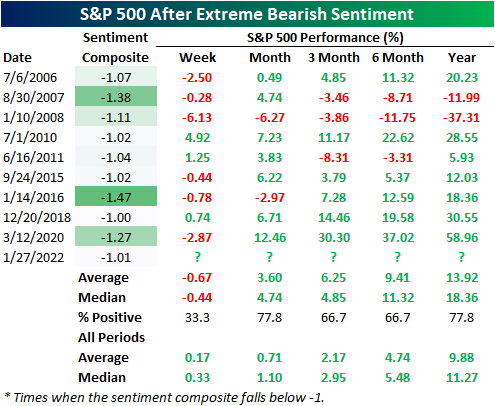

Extreme Bearish Sentiment

As equities continue to sell off, sentiment continues to tank in a broad sense. That being said, there was actually a higher share of respondents to the AAII survey reporting bullish sentiment this week. Coming off the lowest level since July 2020, bullish sentiment rose slightly and remains historically low at 23.1%.

Bearish sentiment, meanwhile, has surged 22.4 percentage points in the past month with more than half of respondents falling in the bearish camp this week. At 52.9%, it was the highest reading since the week of April 11, 2013. In other words, sentiment this week among survey respondents was more negative than even the COVID Crash. In all weeks since the start of the survey in 1987, there have only been 40 other weeks with as high if not higher of a reading.

Given the massive increase in bearish sentiment, the bull-bear spread has also outright collapsed. At -29.8, bears outnumber bulls by the widest margin again since April 2013.

Given bullish sentiment was actually higher as bears surged, the difference came from a big drop in neutral sentiment. Neutral sentiment fell by 8.4 percentage points to 23.9%. That is only the lowest neutral sentiment reading since the first week of September of last year, but it was the biggest week-over-week decline since November 2020.

The AAII survey was far from being alone in indicating bearish sentiment. The Investors Intelligence survey of newsletter writers saw the most bearish readings since the spring of 2020 and the NAAIM Exposure index also saw one of the more modest readings of the past year. Using all of these readings combined, we created our sentiment composite below to get a more general feel for sentiment across these indicators. This week, that composite fell below -1 meaning on average sentiment indicators are a full standard deviation below (or in a bearish direction) their normal reading. Of course, that was the first time such a reading has been observed since the COVID crash.

With data beginning in 2006, there have only been nine other times in which the sentiment composite has fallen below -1 for the first time in at least three months. In the table below, we show those instances and how the S&P 500 has performed going forward. Overall, that bearish sentiment proves to be correct in the next week as the S&P 500 has declined two-thirds of the time. One month to one year later, though, returns have been biased to the positive side with positive returns at least two-thirds of the time. Click here to view Bespoke’s premium membership options.