The Closer — Fed Ahead, PPI Relief, Wheat Inventories, Empire Ouchie — 3/15/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight by taking a look at producer prices. We then move to US inventory data, followed by demand insights. We finish with a look into the rise in inventories compared to the pace of new orders.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/15/22

Bespoke Stock Scores — 3/15/22

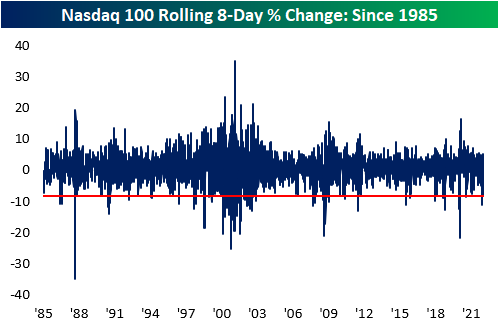

Nasdaq 100 Down Over 1% In Six of Eight Sessions

With volatility becoming an aspect of daily life for investors, the Nasdaq 100 has traded down by over one percent in six of the eight last sessions, resulting in a total drawdown of 8.4% during that span. Although the index is in the green for today (at least for now), the pattern of continuous selling is notable. The last time there were six 1%+ declines in the span of eight trading days (with no other occurrences in the last month) was on January 25th of this year. As you can see from the chart below, a large percentage of the prior occurrences since the index was launched (1985) are clustered between the years 2000 and 2002 (8 occurrences). Overall, these events tend to occur during periods of drawdowns (2000 to 2002 was a long drawdown) but occasionally mark a bottom as the sellers become washed out.

Forward performance following these occurrences is generally mixed, but the period of time with the largest cluster of occurrences (2000 – 2002) also experienced consistent continued weakness. Overall, forward returns were greater than that of all periods for almost every period we looked at (apart from three months),. However, positivity rates are lower across the board compared to normal trading environments, apart from the next week. In 72.2% of occurrences, the market turned higher the following week, resulting in a median return that is eight times higher than the median of all periods.

As you can see from the chart below, we have experienced far worse 8-day drawdowns than the current period, but it is worth noting that this 8-day drawdown is in the 98th percentile of all periods since 1985.Click here to try out Bespoke’s premium research service.

Past performance is no guarantee of future results.

B.I.G. Tips – A Rate Hike Cometh

Chart of the Day: The Ides of March

Harder and Harder to Keep Up

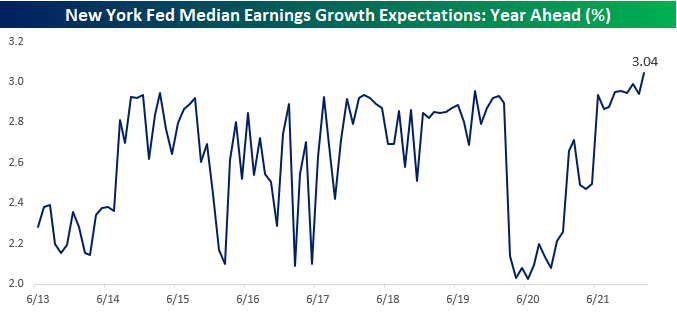

You don’t need us to tell you how confusing this market and economy have been. On Friday, the March preliminary read on sentiment from the University of Michigan showed lower levels of optimism than at the depths of the COVID crash. Despite the pessimism, though, on Monday, the New York Fed’s monthly Survey of Consumer Expectations showed that wage growth expectations for the next year broke out to 3.04% which is the highest level in the history of the survey.

If consumers are expecting wages to grow at the fastest pace in at least a year, why are they so negative? Doesn’t seem to make sense, does it? The reason for the disconnect can be summed up in one word. Inflation. In that same monthly survey of consumer expectations from the NY Fed, inflation expectations for the next year came in at a record high of 6.0%.

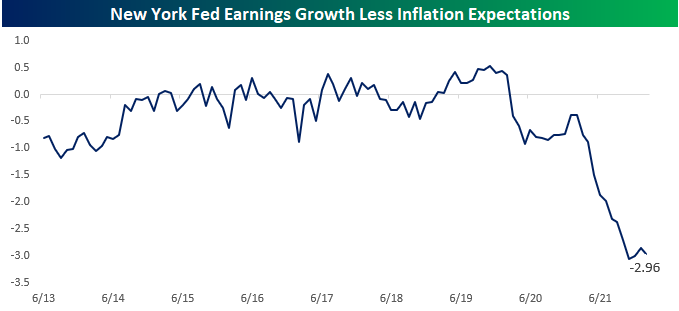

You don’t need a calculator or a chart to figure out that earnings growth of 3% isn’t enough to offset the impact of 6% inflation, but we’ll show you anyway. Below, we show the spread between the monthly readings of year ahead wage growth expectations versus inflation expectations. From the start of the New York Fed’s consumer survey in 2013 right up to before COVID, the spread between the two oscillated in a band of -1.25 to +0.5 percentage points. Once the initial phases of the COVID lockdowns passed and the economy started to reopen, though, all hell broke loose. For the last year, inflation expectations have been rising much faster than earnings growth expectations, resulting in the widest gap in the history of the survey. American consumers have found it hard enough over the years to climb the income ladder in normal times, but with inflation surging over the last year, even moderate levels of wage growth haven’t been enough for consumers to no longer feel as though they’re running up the down escalator. Click here to try out Bespoke’s premium research service.

Bespoke’s Morning Lineup – 3/15/22 – Round Trip

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In times of rapid change, experience could be your worst enemy.” – J. Paul Getty

Equity prices are recovering off early lows as commodity prices, especially oil, plummet. The cause of the decline could be attributed to either concern over weaker demand as the latest COVID wave washes ashore in China, or optimism over the war in Ukraine and the potential for a ceasefire. Those are two very different catalysts and would both have very different implications for the market and global economy as well.

In economic data, February PPI was just released and it came in weaker than expected at both the headline and core levels. Core PPI came in at just 0.2% which was tied for the lowest reading since the end of 2020. While inflation data was weaker than expected, Empire Manufacturing was a disappointment falling 11.8 versus expectations for a level of 6.8. That March reading for Empire Manufacturing was the weakest since May 2020.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

What a month it has been for crude oil. After finishing off February at a level of $95.72, WTI rallied nearly 30% on a closing basis and over 35% on an intraday basis in the span of just over a week. After hitting that multi-year high just a week ago, crude oil has practically round-tripped its entire early March gain, falling more than 22%. If these levels hold through the end of the day, it would rank as the largest decline from a 52-week high in the span of a week or less for WTI on record! Now, if prices at the pump would only reverse that quickly.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Bonds and Stocks at the Lows, Recession Signals, China COVID, EM – 3/14/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight by taking a look at prior instances of both stocks and bonds hitting six months lows, followed by a look into recession odds based on the recent action in equity and credit markets. We then take a look into the effects of China’s COVID-zero policy, and finish with an analysis on emerging markets.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!