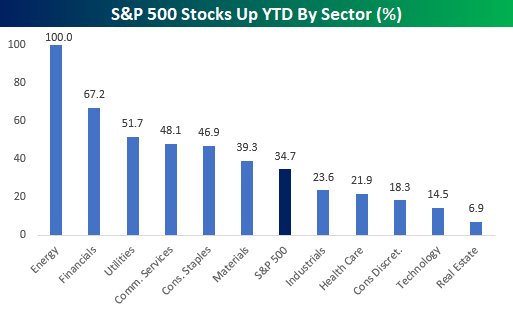

Sector Performance YTD: Energy Dominates

Earlier today in our Morning Lineup post, we highlighted the incredibly wide disparity between the performance of the S&P 500 Energy sector and the rest of the index. To further illustrate the divide, the charts below show the average YTD performance of S&P 500 stocks by sector as well as the percentage of stocks in each sector that are up YTD.

Starting with average performance, stocks in the Energy sector are up an average of 21.6% YTD which is more than 18 percentage points higher than the next closest sector (Financials). Energy is also one of just two sectors in the S&P 500 where the average YTD return of stocks in the sector is positive. For all the stocks in the S&P 500, the average YTD change is a decline of 4.1%, and in the Technology sector, its individual components are already down an average of just over 10% YTD!

With stocks in the Energy sector up an average of over 20% YTD, it shouldn’t come as too much of a surprise that every stock in the sector has posted YTD gains. After Energy, Financials and Utilities are the only two other sectors where more than half of the components are up YTD. For the S&P 500 as a whole, barely more than a third of stocks in the index are up YTD while less than 15% of Technology stocks and just 6.9% of stocks in the Real Estate sector (2 out of 29) are in the black. A number of strategists have said 2022 will be the year of the stockpicker, but so far this year, it’s been increasingly difficult for those stockpickers to find winners – especially outside of the Energy sector. See more in-depth market analysis from Bespoke by starting a two-week trial to Bespoke Premium today.

Bespoke’s Morning Lineup – 2/8/22 – New Highs in Yields

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We don’t have to be smarter than the rest. We have to be more disciplined than the rest.” – Warren Buffett

Futures are modestly higher for the S&P 500 and Dow this morning, but the Nasdaq is indicated to open lower in what’s looking like a mixed session for stocks. Futures started to lose some steam shortly after the European open as Treasury yields have been moving higher with the 10-year eclipsing 1.95% to its highest level since summer 2019.

The latest read on small business sentiment dropped to an 11-month low, but 61% of companies surveyed reported that they have raised prices, so inflation pressures remain firm. On a brighter note, WTI is trading back below $90 after hitting multi-year highs late last week.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

We’re barely a month into the new year, but 2022 is shaping up to be a year where it’s Energy and everyone else. Year to date, the sector is up over 25%, and besides Financials, which is up less than 3%, every other sector is staring at losses. The chart below shows the performance of the ProShares S&P 500 Ex Energy ETF (SPXE) compared to the performance of the S&P 500 Energy sector ETF over the last year. For much of the last twelve months, Energy has outperformed the S&P 500 Ex Energy, but as the calendar flipped to 2022, the divergence has widened out to extreme levels. Even as Energy has risen more than 25% this year, the rest of the S&P 500 is down close to 7% on a market-cap-weighted basis, and that has stretched the one year performance gap between the two ETFs over the last year to 50 percentage points (63.96% vs 13.95%).

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

B.I.G. Tips – “Cheapest” (For a Reason) S&P 500 Stocks

Daily Sector Snapshot — 2/7/22

Chart of the Day: Speculators Scatter

Gold “G-loiters”

Everyone knows that gold ‘glitters,’ but for the last year, it’s more like ‘gloiters’ as the commodity has been loitering around the $1,800 per ounce level. This morning, gold is trading modestly above $1,800, which is a level it has crossed above and below multiple times in the last 12 months. In fact, the average price of gold over the last 12 months has been $1,795 per ounce, so there hasn’t been a lot of movement.

Taking a longer-term look at gold shows some interesting trends. On a five year basis, the last 12 months of sideways trading looks like part of a consolidation phase for the commodity as it digests its big move higher from mid 2018 through early 2020 when prices surged from under $1,300 per ounce to more than $2,000.

While gold’s move over the last year looks like a consolidation of a strong rally on a five year chart, a ten year look at gold shows another trading range where prices today are right around the same level they were in 2012. As long as gold can hang around in the $1,700 to $1,800 range, the longer-term technical picture looks positive.

Just as the last year’s sideways pattern for gold looks like a consolidation of a strong rally on the five year chart, the sideways pattern of the last ten years looks like a very long-term consolidation following the rally in the early 2000s where prices rose more than six-fold from under $300 per ounce in early 2002 to nearly $1,900 in August 2011.

With a one-year trading range of less than 15%, gold is trading in its narrowest one-year range since July 2018, and before that, 2005. Eventually this range is going to break, and based on prior experience, once the range breaks, it usually expands pretty rapidly, so one direction or another, gold looks poised for a significant move going forward. See more in-depth market analysis from Bespoke by starting a two-week trial to Bespoke Premium today.

Bespoke’s Morning Lineup – 2/7/22 – Picking Up Steam

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have never in my life envied a human being who led an easy life. I have envied a great many people who led difficult lives and led them well.” – Theodore Roosevelt

After a lower start overnight, futures have slowly picked up steam this morning and are now in modestly positive territory across the board with the Nasdaq leading the way higher. Overnight, economic data in Asia was on the weak side with China’s Services PMI missing expectations while Japan’s index of Leading Indicators decelerated relative to December.

Here in the US today, the only economic report on the calendar is Consumer Credit at 3 PM Eastern. On the earnings front, key reports after the close today include Amgen (AMGN), Tenet Healthcare (THC), and Simon Properties (SPG).

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

If you talk to just about any investor lately, they’ll tell you that it has been a difficult year in the market. Putting the recent moves into perspective, it could have been a lot worse. Friday’s close marked 23 trading days since the S&P 500’s last closing record high, and during that span, the S&P 500 is down 6.2%. When comparing the last 23 trading days to other 23 trading day periods since 2000, there have been plenty of periods where the market saw much larger declines. Prior to the current period, the last time the S&P 500 declined 6% over a 23 trading day period was in late September 2020, but six months before that we saw what was the largest decline in a 23 trading day period since the Great Depression when the S&P 500 lost more than a third of its value from its peak on 2/19/20 to its low on 3/23/20.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 2/4/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Foreign Affairs

NAHB Welcomes Biden Administration Move to Lower Lumber Tariffs (NAHB)

A Biden administration proposal to reduce tariffs on lumber imported from Canada to the United States got a warm reception from the National Association of Homebuilders this week. [Link]

What the US could learn from China’s nuclear power expansion by Daniel Van Boom (CNET)

China will add ten new nuclear power plants per year over the next decade and a half as it seeks to meet soaring electricity demand while avoiding carbon-intensive power production like coal that has fueled electrification so far. [Link]

Ukraine and Dollar Weaponization by George Pearkes (Atlantic Council)

Bespoke’s macro strategist discusses the macroeconomics driving the unique properties of the dollar as a weapon that could be used to hem in Russian aggression towards Ukraine. [Link]

Battery Joe

Tesla, Who? Biden Can’t Bring Himself to Say It — and Musk Has Noticed by Dana Hull and Jennifer Jacobs (Bloomberg)

A difference of opinion over unions mean the President and the CEO of the world’s largest EV maker don’t see eye-to-eye despite huge enthusiasm for the emission-free vehicles from the White House. [Link; soft paywall, auto-playing video]

Biden’s Race to Convert Trump Voters to EVs by Gregory Korte (Bloomberg)

While EVs are gaining popularity, most GOP-leaning states have rejected the vehicles. Convincing conservatives to ditch gas or diesel for batteries will be a prerequisite for big uptakes in electric vehicles nationally. [Link; soft paywall]

Going Coastal

Jeff Bezos’ new megayacht is so big, the Dutch are going to have to take apart a historic bridge to let it pass by Avery Hartmans (Business Insider/MSN)

The massive, 417-foot yacht that is being built for Jeff Bezos up the river from Rotterdam won’t be able to pass under a bridge on its way to the Atlantic, so the company building the boat is paying to have the bridge temporarily dismantled. [Link]

The Last Oyster Tongers of Apalachicola by David Hanson (The Bitter Southerner)

Collapsing oyster populations in Apalachicola Bay mean that there will be no harvests for five years, part of an effort to rebuild beds so future tongers can ply their trade on ocean skiffs in the Gulf. [Link]

Crypto

Intuit CEO Warns of Tax Bill Shock for Bitcoin, NFT Traders by Joe Williams (Bloomberg)

Millions of small investors are at risk of serious tax liabilities this year, with capital gains taxes as high as 37% on gains from trading crypto and NFTs. [Link; soft paywall]

The Federal Reserve Bank of Boston and Massachusetts Institute of Technology release technological research on a central bank digital currency (Federal Reserve Bank of Boston)

The Boston Fed and MIT partnered in a research effort that was not designed to create a usable CBDC and is separate from the Federal Reserve Board’s own exploration of a CDBC. One codebase designed by the team was able to handle 1.7 million transactions per second with “the vast majority” settling in under 2 seconds. [Link]

Teachers

Teachers Are Quitting, and Companies Are Hot to Hire Them by Kathryn Dill (WSJ)

The pandemic is driving teachers out of the classroom even as the private sector goes on a hiring binge, and teachers are a popular target to work in a range of fields. [Link; paywall]

Novel Ideas

Our data centers now work harder when the sun shines and wind blows by Ana Radovanovic (Google)

This news is a bit old (published in 2020) but it’s still interesting: Google shifts data center use to ramp up when renewable electricity is more available, reducing the amount of non-renewable electricity data centers consume. [Link]

This company says it’s developing a system that can recognize your face from just your DNA by Tate Ryan-Mosley (Technology Review)

An Israeli startup claims it may be able to use DNA to predict what a person looks like, though the company is somewhat dodgy and experts see the technology as “pseudoscience”. [Link]

COVID

One Million Deaths: The Hole the Pandemic Made in U.S. Society by Jon Kamp, Jennifer Levitz, Brianna Abbott, and Paul Overberg (WSJ)

The US death toll from COVID is about to move above 1mm, with hundreds of thousands succumbing to the virus and huge numbers dying from related or adjacent causes. [Link; paywall]

Baseball Cards

This Philadelphia startup tells you what your old baseball cards are worth — with just a photo by Kennedy Rose (Biz Journals)

A start-up allows users to digitize their trading card collections with a mobile phone, making valuing and monetizing the cards much easier and more efficient than traditional assays. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 2/4/22 – Volatility In Markets, Volatility In Policy

This week’s Bespoke Report newsletter is now available for members.

We’ve seen some titanic shifts in response to earnings in the last couple of weeks, but even bigger ones are the pivots towards higher rates across global markets as central banks move to stifle growth as a path to lower inflation. We dive deep in to earnings results and reactions across equity markets on both sides of the Atlantic this week, economic data in the US and around the world, and cover a range of other topics in this week’s Bespoke Report.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.