Daily Sector Snapshot — 4/5/22

Chart of the Day: Google Search Trend “Reopening” Update

Bespoke Stock Scores — 4/5/22

Bespoke’s Morning Lineup – 4/5/22 – Fed Speakers Step Up to the Plate

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The meek shall inherit the Earth, but not its mineral rights.” – J. Paul Getty

Outside of the drama surrounding Twitter (TWTR) and Elon Musk, who is now a board member of the company, there’s not a lot of newsflows this morning centered on US stocks. The only economic report on the calendar is the ISM Services report at 10 AM eastern, but there are also a number of Fed speakers scheduled. At 10 AM, we’ll hear from Minneapolis Fed President Kashkari, and then at 11:05 AM Fed Governor Lael Brainard will likely shed additional light on whether the Fed moves 50 bps at its next meeting. The final speaker of the day will be New York Fed President Williams at 2 PM.

Equity futures are modestly lower today, but the most noteworthy development of the morning is the fact that the 2s10s curve has steepened and has nearly ‘unverted’.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

With a month-to-date gain of more than 4% in just two trading days, the run higher in Brazilian stocks has continued into the second quarter. Year to date, the iShares MSCI Brazil ETF (EWZ) is now up over 40%, and given that gain, we don’t know what’s more noteworthy. Is it the fact that since its inception in 2000, this represents the best YTD start for the ETF (through 4/4) on record? Or is it that even after this year’s rally, the ETF is over 6% relative to its high in 2021?

Starting with YTD starts, the chart below shows the YTD gain for EWZ going back to 2001. This year’s 40.8% gain easily ranks as the strongest YTD gain for the ETF since its launch.

As mentioned above, the last year has been a roller-coaster for EWZ. Even after this year’s sharp rally, which began on 1/5, EWZ remains more than 6% below its June 2021 high.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Background Checks Rise, But Still Compressed

Although not a commonly used indicator, US background checks for firearm purchases can be interpreted as a gauge of sentiment and the view of Americans on the current state of the geopolitical environment. At times of ease, background checks can be expected to decline, whereas a volatile situation (ie the onslaught of COVID, the summer of riots, etc) or concerns over more stringent gun legislation often lead to increased firearm purchases. In March, background checks ticked higher by 20.6% month over month. However, on a y/y basis, background checks are still down by 34.3%, as illustrated in the chart below. On a year-to-date basis, background checks are down a similar 33.9%. In March, a total of 3.1 million background checks were run for Americans looking to purchase firearms.

Monthly background checks remain well above their historical trend, despite the y/y compression. In the near term, it is possible that checks bottomed out last month at 2.6 million. Long story short, although checks are down significantly y/y, the long-term uptrend that was in place prior to the COVID surge is still largely in effect.

Although we like to think that the market is forward-looking, the price action of gun manufacturer Sturm Ruger (RGR) tends to be highly correlated with the number of background checks over the prior twelve months. Since the turn of the century, total trailing 12-month total of background checks and the monthly price of RGR have held a correlation coefficient of 0.90, which indicates a strong positive relationship. Should background checks tick higher, RGR has room to benefit.

Looking at the two different publicly traded firearms manufacturers, the chart patterns for each look quite different. Whereas RGR has been in a short-term uptrend, Smith and Wesson (SWBI) has been trending lower for several months now, despite a positive federal court ruling in regards to turning over research data and advertising research to the NJ Attorney General just three weeks ago. Nonetheless, this goes to show that, even though these companies are exposed to the same secular trends, near-term performance can and will diverge due to company-specific exposures. Click here to try out Bespoke’s premium research service.

Chart of the Day: Economic Sentiment Can’t Get Much Worse

Daily Sector Snapshot — 4/4/22

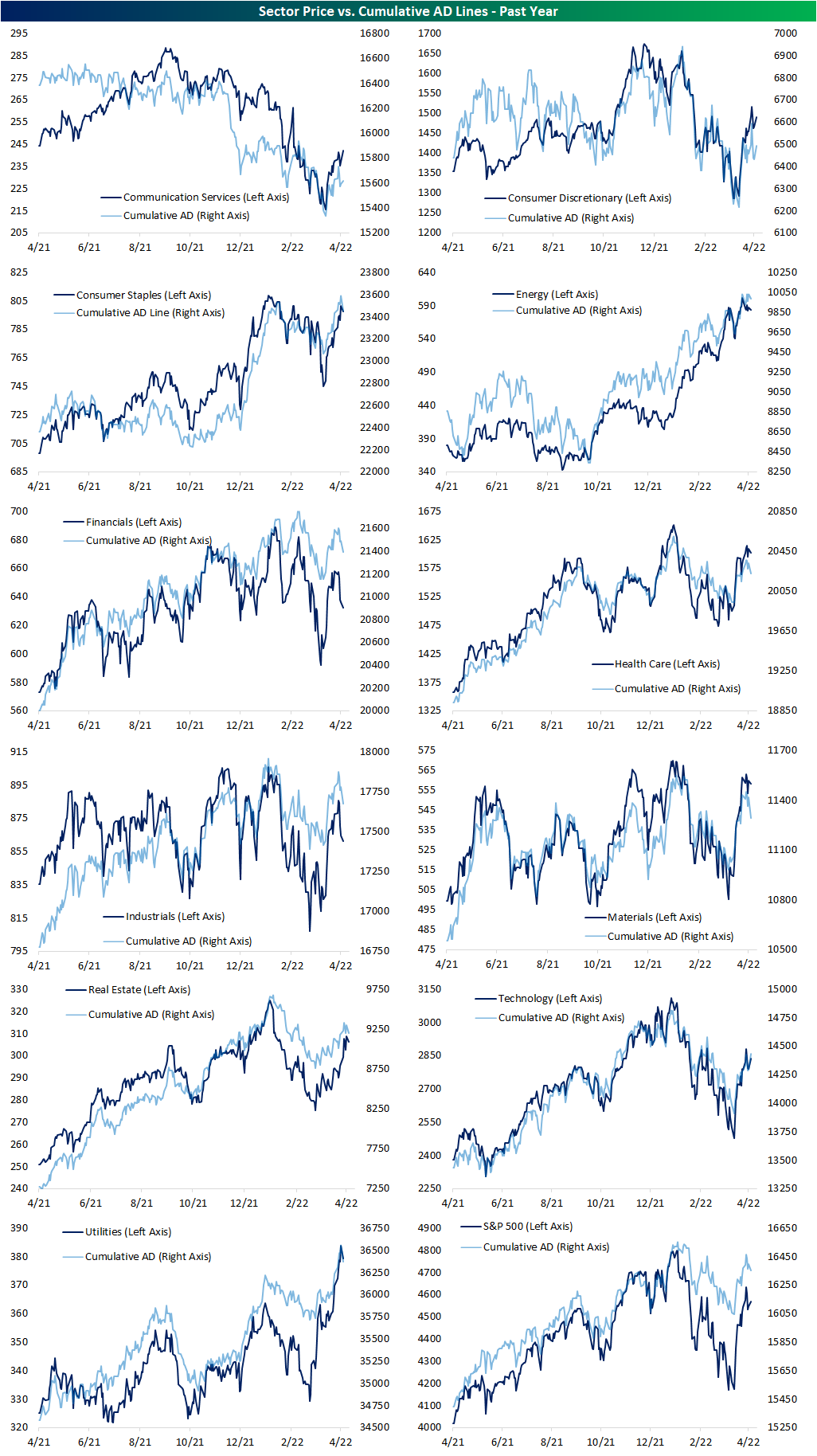

Sector Price and Breadth Update

In an earlier tweet, we highlighted some charts from our Sector Snapshot highlighting the new highs in multiple sectors’ cumulative advance-decline (A/D) lines as of Friday. The cumulative A/D line is used to signal confirmation of a trend by indicating broad participation of an index’s underlying stocks in a rally or decline. In the charts below, we show those same A/D lines updated through today with price also included on the opposite axis.

Utilities, Consumer Staples, and Energy are seeing their AD lines pull back from new highs, but price has been somewhat disconnected. On the one hand, for Consumer Staples, unlike the A/D line, price never broke out above the late 2021/early 2022 levels. Energy, meanwhile, has seen breadth hold up fairly well while its price has been experiencing a more consistent decline in recent days. On the other hand, Utilities have seen price and breadth move more healthily in sync with one another. Communication Services has been somewhat the inverse of these three sectors. While breadth is positive today, the cumulative A/D line is not setting any new short-term highs even as the price is. That is mostly a result of the huge gain in Twitter (TWTR) having an outsized impact on the sector.

Most other sectors have recently seen consistent moves between price and breadth without any sort of major new highs or lows. Technology is close to moving above last week’s high on both a price and breadth basis while both readings for Financials and Industrials have been falling sharply. For Materials, another cyclical sector, breadth and price have been moving in the same direction, but the decline in the cumulative A/D line stands out slightly more. Click here to view Bespoke’s premium membership options.

.

.

March 2022 Headlines

Bespoke’s Morning Lineup – 4/4/22 – Elon Flips the Bird

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Given that Twitter serves as the de facto public town square, failing to adhere to free speech principles fundamentally undermines democracy.” – Elon Musk

Heading into today, it was looking like a quiet start to what was looking like a slow week as the economic calendar is light and earnings season doesn’t kick off for at least another week. That changed a bit following news that Elon Musk had taken a passive 9.2% stake in Twitter (TWTR) pushing the stock up by more than 25% in pre-market trading to its highest level since late November. Last week on Twitter, Musk made the statement at the top of this note and then followed up with the question, “What should be done?” Well, this morning we appear to be getting an answer. Twitter has long been criticized for not realizing its full potential, and TWTR shareholders are hoping Musk can move the company in that direction.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

With the stock poised to open up more than 20% this morning, it will be just the fourth time in its history as a public company in 2013 that TWTR has gapped up more than 20%. Two of those days were in reaction to earnings (July 2014 and February 2018), and then on the day of its IPO in November 2013. Today, it’s all Elon.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.