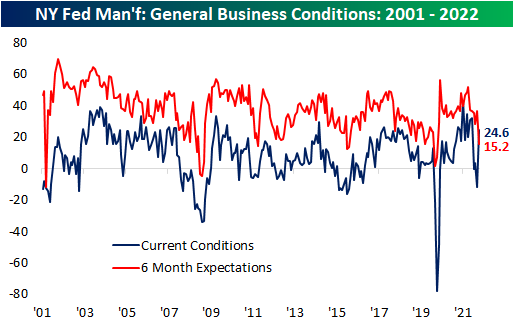

A Good Friday From the Empire Fed

Even though markets were shuttered on Friday for the Good Friday holiday, the New York Federal Reserve branch released the latest update on their monthly manufacturing report with astounding results. Heading into the release, the March reading had shown a significant decline back into negative territory indicating the region’s manufacturers reported contractionary overall activity. In April, activity rebounded substantially with the headline number rising 36.4 points all the way up to 24.6. That set the second-largest month-over-month increase on record behind the 48.3-point jump back in June 2020. In terms of the level of the index, it brought it from a lower decile reading to levels just shy of the upper decile of its historical range going back to the start of the survey in the early 2000s.

Although current conditions were impressive, we would caution that expectations soured in an equally dramatic fashion. The six-month expectation index dropped 21.4 points to 15.2. That was only 0.3 points shy of the second-largest decline on record (21.7 point decline in March 2020) but was far better than the 61 point drop after 9/11 in the early days of the survey.

The move higher in General Business Conditions was thanks to big turnarounds in New Orders and Shipments but breadth elsewhere in the report was not as positive. Of the seven other categories, four declined month over month with three of those declines ranking in the bottom decile of each one’s respective histories. Again, expectations were much more worrisome with large declines across categories and readings in the bottom few percentiles for things like New Orders, Shipments, and Unfilled Orders. Overall, the report showed solid improvements in conditions but how sustainable those improvements will be in the coming months could come into question.

The biggest contributors to the increase in the headline reading were improvements in New Orders and Shipments. Each one crossed back into the top decile of their historical ranges on some of the biggest month-over-month increases on record outside of the spring of 2020. Unfilled Orders were also higher, though, unlike New Orders or Shipments, the index is coming off of already elevated levels. Given the strength in demand and shipments, inventories grew at a slower rate. Expectations were much less optimistic as across all four of these categories there were near-record declines. Unfilled Orders and Inventories even fell into contraction. That means that although New York area firms witnessed solid improvement in business conditions in April, the positive changes are not expected to keep pace or continue in the months ahead.

One likely reason for the big improvements this month was the easing of supply chain stress. The index of Delivery Times fell back down to the low end of its elevated pandemic range in April (higher readings indicate products are taking longer to reach their destination).

Those improvements in current conditions did not filter through to employment. While the region’s firms are on net still increasing hiring, the index for Number of Employees fell to the lowest level since October 2020 after two months of the largest MoM declines since the onset of the pandemic. As hiring decelerates, the average workweek did tick up solidly. That index rose 6.5 points to 10. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – Tax Day – 4/18/22

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “The difference between death and taxes is death doesn’t get worse every time Congress meets.” – Will Rogers

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Below is a table we highlight each year showing the S&P 500’s performance in the weeks leading up to and the weeks immediately following Tax Day. As shown, over the last 20+ years, the weeks before Tax Day have been much weaker for the market than the weeks after. This year has been no different thus far with the S&P falling more than 3% in the two weeks leading up to Tax Day. Now we just need the trend of gains in the two weeks following Tax Day to hold as well!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 4/17/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Real Estate

What Happened to the Gilded Age Mansions of New York City? by Candace Taylor (WSJ)

The history of the midtown mansions which used to be a defining feature of life in Manhattan; they’ve long since disappeared under soaring buildings which now dominate the city. [Link; paywall]

Redfin Reports Demand Slips, Pushing More Sellers to Drop Asking Prices (Redfin/Business Wire)

A summary of leading indicators for home buying demand that have started to slow. Fewer searches, fewer tours, fewer mortgage applications, and higher rates are all illustrating a looming cooldown in the housing market. [Link]

How Remote Work is Shifting Population Growth Across the U.S. by Adam Ozimek (Economic Innovation Group)

An analysis of Census data that suggests remote work is driving population outflows from high-cost dense metros and towards suburbs, exurbs, and rural areas around the country. [Link]

Work

Sure, Work Makes Us Want to Swear. But Should You? by Rachel Feintzeig (WSJ)

It’s one thing to let fly with profanity at home, but returns to the office have meant habits developed during the pandemic may require a bit of adjustment now that there are coworkers in ear shot again. [Link; paywall]

Everything Costs More, and That’s Disrupting Retirement for Many by Harriet Torry (WSJ)

Inflation appears to be playing a role solving a problem that was much fretted over last year: workers are returning to the labor force to augment retirement income amidst high rising prices. [Link; paywall]

Starbucks is weighing better benefits for employees but says they could exclude union workers by Amelia Lucas (CNBC)

Already facing one complaint from the NLRB for union-busting, Starbucks is trying to fight further unionization by denying benefits to union shops and may run further afoul of labor regulations in the process. [Link]

Innovation

A McDonald’s distribution partner in Canada is testing an electric Volvo truck — take a closer look at the big rig EV by Brittany Chang and Mary Meisenzahl (Business Insider)

EV trucks are starting to hit the road in Canada as part of a test for Volvo’s new offerings. McDonalds is testing the trucks as part of its distribution network. [Link]

World’s Biggest Particle Collider to Restart in Bid to Extend Frontiers of Physics by Aylin Woodward and Janet Babin (WSJ)

The massive particle accelerator along the Swiss-French border has been shut down for three years, but new collisions will resume soon after a series of upgrades. [Link; paywall]

Emerging Markets

Unsafe at any price by Jay Newman (FTAV)

Concerns are mounting over the shift away from protective covenants are especially grave among the highly-indebted sovereign borrowers from emerging markets, where legal enforcement against sovereign actors is always more complicated than in the private sector. [Link; registration required]

U.S. and Chinese Bond Yields Converge, Reversing a Decadelong Pattern by Rebecca Feng (WSJ)

The once-large yield advantage for Chinese government bonds relative to those in the US has been erased, with a slowing Chinese economy and tightening Fed policy leading to a convergence between the two large markets. [Link; paywall]

Supply Chains

Building Resilient Supply Chains (Council of Economic Advisors)

A detailed report on the general nature of supply chains and steps that could be taken to make them more resilient, part of the CEA’s annual Economic Report of the President. [Link; 42 page PDF]

France

First round of 2022 French election in charts by Eir Nolsoe, Ella Hollowood, and Oli Elliot (FT)

A series of charts explaining the geographic, material, and educational differences between voters that supported Marine Le Pen and Emmanuelle Macron in France’s first round elections. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Bespoke’s Crypto Report — 4/15/22

Bespoke’s Crypto Report contains numerous technical, momentum, and sentiment charts for bitcoin, ethereum, and other key cryptos. Page 1 of the report includes our weekly commentary on the space and attempts to identify any new trends that are emerging. The remaining pages include important overbought/oversold levels to watch, charts on historical drawdowns and rallies, seasonality trends, futures positioning data, Google search trend shifts, and more. Our weekly Crypto Report is produced so that followers of the space can more easily stay on top of price action, technicals, seasonality, and sentiment.

Sign up for a monthly or annual subscription to Bespoke Crypto to receive our weekly Crypto Report and anything else we publish related to cryptos. Note: If you’re currently a Bespoke Premium, Bespoke Newsletter, or Bespoke Institutional subscriber, you’ll need to subscribe to Bespoke Crypto as an add-on to receive access. The weekly Crypto Report and any additional crypto analysis is not included with our Premium, Newsletter, or Institutional memberships. You can sign up for Bespoke Crypto and receive our Crypto Report in your inbox weekly using the monthly or annual checkout links below. If you sign up for the annual plan, the first year of access is 50% off!

Bespoke Crypto Access — Monthly Payment Plan ($49/mth)

Bespoke Crypto Access — Annual Payment Plan ($247.50 for the first 12 months, then $495/year in year 2 and beyond)

Bespoke Investment Group, LLC believes all information contained in this service to be accurate, but we do not guarantee its accuracy. None of the information in this service or any opinions expressed constitutes a solicitation of the purchase or sale of any securities, commodities, or cryptocurrencies. This service contains no buy or sell recommendations. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

The Bespoke Report – 4/14/22 – Churn! Churn! Churn!

This week’s Bespoke Report newsletter is now available for members.

We can’t get the Byrds song “Turn! Turn! Turn!” out of our minds lately, but in our heads, we’re singing Churn! Churn! Churn!. Stocks can’t seem to find any direction these days, and that’s being somewhat generous. If anything, the trend has been lower, but with the weekend approaching, let’s be generous in order to keep up the mood. The 200-day moving average is typically considered a major trendline for the S&P 500 with breaks above considered bullish, while moves below suggest a bearish outlook. If that’s the case, what are we to make of the fact that the S&P 500 has crossed above its 200-DMA more than five times this year and crossed below it six times? As we’ve all said to our kids all too often, “Make up your mind already!”

While we had a holiday-shortened week, it was still plenty busy with the kick-off of earnings season and a bunch of economic data. We cover it all in this week’s Bespoke Report along with the big drop in bullish sentiment, some whipsaw moves in the treasury market, a look at seasonality around tax day, and lastly a checkup on the semiconductors.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Bespoke’s Weekly Sector Snapshot — 4/14/22

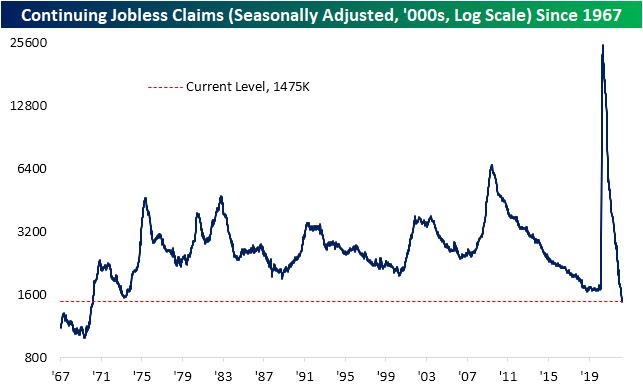

Claims Bounce Off Multi-Decade Lows

After coming in at one of the lowest levels on record last week, seasonally adjusted initial jobless claims bounced up to 185K this week. While higher, jobless claims are still historically strong having spent a record eight straight weeks with sub-200K readings.

As we noted last week, seasonal adjustments overstated the strength of claims as unadjusted claims experienced a seasonally unusual decline. This week was more normal from a seasonal perspective with initial claims rising from 194.4K to 222.5K and the first reading above 200K since the week of March 11. As shown in the second chart below, the current week of the year has consistently seen claims move higher week over week marking a temporary high before resuming the seasonal downtrend through the next couple of months. That means the slight uptick this month is likely mostly seasonal and far from any sort of a change in trend.

Lagged one week to initial claims, continuing jobless claims fell to a new low of 1.475 million. That is the lowest level of claims since March 1970. Click here to view Bespoke’s premium membership options.

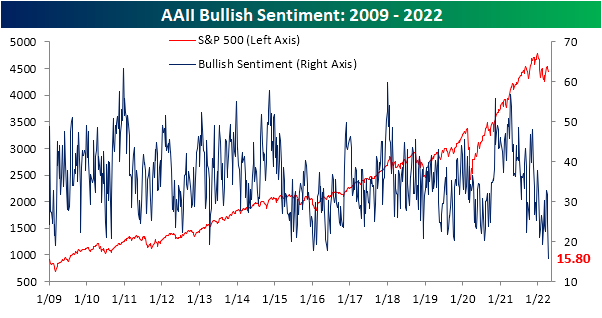

Where Have All the Bulls Gone?

Heading into this week, bullish sentiment on the part of individual investors, measured by the weekly AAII survey, was already depressed with less than a quarter of respondents reporting optimistic sentiment. One week later with the S&P 500 continuing to move lower and a couple of hot, but not exactly unexpected, inflation readings in the interim, bullish sentiment has collapsed another 8.9 percentage points to the lowest level since the week of September 3rd, 1992. That’s right, bullish investor sentiment never got this low even at the depths of the pandemic, during the Global Financial Crisis, or during the Dot Com bubble burst. This week marks one of only 35 weeks since the survey began in 1987 that bullish sentiment was below 20%; the most recent being only back in February when it fell to 19.2%.

As could be expected, the huge drop and the historic low in bullish sentiment was met with a coincident increase in bearish sentiment. Bearish sentiment rose 7 percentage points to 48.4%. While that is an elevated reading, there have been a couple of even more elevated readings as recently as March 17 (49.8%), February 24 (53.7%), and January 27 (52.9%).

Even though bearish sentiment is not at a new high, the still-elevated reading on pessimism paired with the extremely depressed reading on bullishness has resulted in the bull-bear spread to fall much deeper into negative territory. Only two weeks ago, bulls actually outnumbered bears. Today, bears outnumber bulls by 32.6 percentage points. The 37 point drop since that positive reading marks the largest two-week decline in the bull-bear spread since April 2013. It is also the lowest level of the spread since that same period.

While bearish sentiment picked up, not all of those gains came from the decline in bulls. Neutral sentiment was slightly higher rising 1.8 percentage points to 35.7%. That is a few percentage points above the historical average, but it is also well below the multiple highs of the past year. You can read Bespoke’s full analysis of investor sentiment and its contrarian aspects with a two-week trial to Bespoke Premium.

The Bespoke 50 Growth Stocks — 4/14/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 4/14/22 – Whoa

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You only get out of it what you put into it. If you are a sheep in this world, you’re not going to get much out of it.” – Greg Norman

As bad as you think you think you have it right now with the weakness in the stock and bond market this year, just consider yourself lucky you weren’t in Greg Norman’s shoes 26 years ago today at Augusta. Actually, at this point in the day, as the birds chirped, the morning dew on the fairways glistened in the sun, and the scent of azaleas filled the air, Norman probably had a pretty big smile sitting on a six-stroke lead over Nick Faldo heading into the final round of the Masters. When the round started, though, the path got a lot rougher. Norman started with a bogey on the first but got back on track with a birdie on two. Then, after a par on the third, Norman bogeyed the par-three fourth and then bogeyed again on the par-four eighth.

One over for the front nine wasn’t bad, but coming out on the back nine, Norman put up bogey, bogey, and double-bogey on 10, 11, and 12 and finished the round with a six over 78. What looked like a Sunday formality for Norman turned into one of the biggest collapses in Masters history as Nick Faldo countered with an epic 67 and was fitted for the green jacket in the clubhouse. 26 years later, Norman’s round is still considered the worst collapse in Masters history; almost like the golf equivalent of the 1987 crash (or at least Marlboro Friday). As a columnist for the Tampa Tribune described it, “For Greg Norman’s lifetime, for yours, for mine, for eternity, wherever golf is played and remembered, in pro shops, pawnshops, locker rooms, card rooms, bars, churches, in Augusta, Ankara, and Alaska, the 1996 Masters will be recalled simply as the one Greg Norman blew.” See, things aren’t so bad.

Even with that collapse, most of us would change places with Greg Norman in a second. Winston Churchill once said, “Success consists of going from failure to failure without loss of enthusiasm.” And while Norman never went on to win another major and only managed to win a handful of other tournaments, he went on to enjoy an extremely successful professional career in clothing, golf course design, wines, real estate, and a number of other endeavors. In other words, he adapted to and capitalized on the environment he found himself in. Similarly, the stock market is always evolving. While a certain approach works in one environment, as circumstances change, investors need to adapt and capitalize on the opportunities that present themselves.

Economic data this morning was mixed with Initial Jobless Claims coming in slightly ahead of forecasts while Continuing Claims were weaker. Headline Retail Sales were just shy of forecasts while the reading ex-autos and gas came in at 1.1% compared to forecasts of an increase of 0.9%. The reaction from futures has been muted as a lot of traders may already be starting their holiday weekend early.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Sometimes we look at an indicator and just say, “Whoa”. That was out reaction this morning when we saw the latest sentiment survey from the American Association of Individual Investors (AAII). After dropping to an already depressed level of 24.7% last week, this week’s reading plummeted to 15.8%. To find a lower reading you have to go back even further than Greg Norman’s collapse at the Masters. The last time there were fewer bullish investors in the AAII survey was in September 1992 when Boyz II Men topped the charts with “End of the Road”. While the period from 1992 through 1994 wasn’t the best time period for the stock market, it certainly wasn’t the end of the road either.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.