June 2022 Headlines

Bespoke’s Morning Lineup – 7/19/22 – Working on a Turnaround Tuesday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Lots of companies don’t succeed over time. What do they fundamentally do wrong? They usually miss the future. I try to focus on that: What is the future really going to be?” – Larry Page

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After a disheartening late-day decline yesterday, futures are attempting a ‘turn-around Tuesday’ this morning. In addition to a handful of high-profile earnings reports from IBM, Johnson & Johnson (JNJ), and Lockheed Martin (LMT), we also just got the latest update of Building Permits and Housing Starts which came in mixed relative to expectations. Building Permits were slightly higher than expected and Housing Starts missed slightly.

Another notable report this morning was the latest Merrill Lynch Fund Managers Survey which showed widespread pessimism on the part of respondents. According to the report, exposure levels to risk assets were taken down to their lowest levels since the Financial Crisis while cash levels are higher now than at any other time since 2001!

Today’s Morning Lineup discusses earnings news out of Europe and the US, handicapping the ECB decision, and economic data from around the world.

Everyone wants to see inflation subside, and we welcome any sign of a pullback in upward price pressures. The latest datapoint optimists are glomming on to is the fact that the national average price of a gallon of gas dropped below $4.50 per gallon yesterday after touching $5 as recently as mid-June. That’s a decline of nearly 10%!

The move lower in gas prices is welcomed by us more than anybody, but before we all close the book on this chapter in the inflation saga and let our guard down, we should keep in mind that from a seasonal perspective, we are in what has historically been a relatively weak time of year for prices at the pump. Prices typically peak for the year around Memorial Day, trade sideways through the summer, and then decline into year-end. Second, while prices are down sharply after the last month, it follows what was a parabolic increase in prices year to date through mid-June.

Despite a 7.2% decline so far in July and a nearly 10% decline over the last month, the national average price of a gallon of gas is still up 9.3% over the last three months, 36.8% year to date, and 42% over the last year! That’s hardly a trend of lower prices. Moving further out, the percentage gains have been even larger. Over the last two years, Americans are paying more than double what they were paying for gas, and over the last three and four years, the average price has increased by roughly 60%.

We’re pleased as anyone with the direction of gas prices over the last month, but just as we’ve seen countless examples of the market or individual stocks in downtrends stage an impressive rally only to give it all back again, let’s hope this move lower in gas prices isn’t a false alarm in the other direction.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 7/18/22

Chart of the Day – Volume Ain’t All It’s Cracked Up To Be

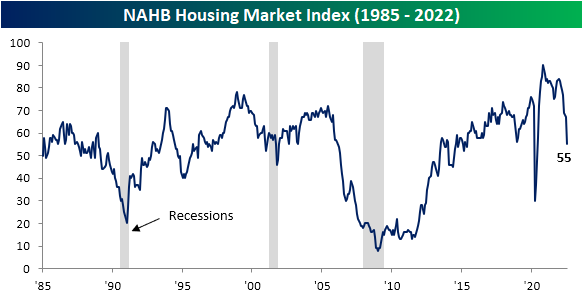

Homebuilder Sentiment Plummets

Another bad reading for housing hit the tape today as the NAHB’s Housing Market Index measuring the confidence of US homebuilders experienced its second largest decline on record behind the drop in April 2020. Homebuilder sentiment cratered 12 points month over month sending the index to the lowest level since May 2020 which is also one point below the late 2018 low.

Given the drop in the headline number, each of the individual components (present and future sales and sales traffic) similarly experienced historic declines month over month. Like the headline index, Present Sales and Traffic only experienced larger declines at the start of the pandemic. The same goes for Future Sales, although there was also a slightly larger drop in December 1987 making this month’s drop the third largest on record.

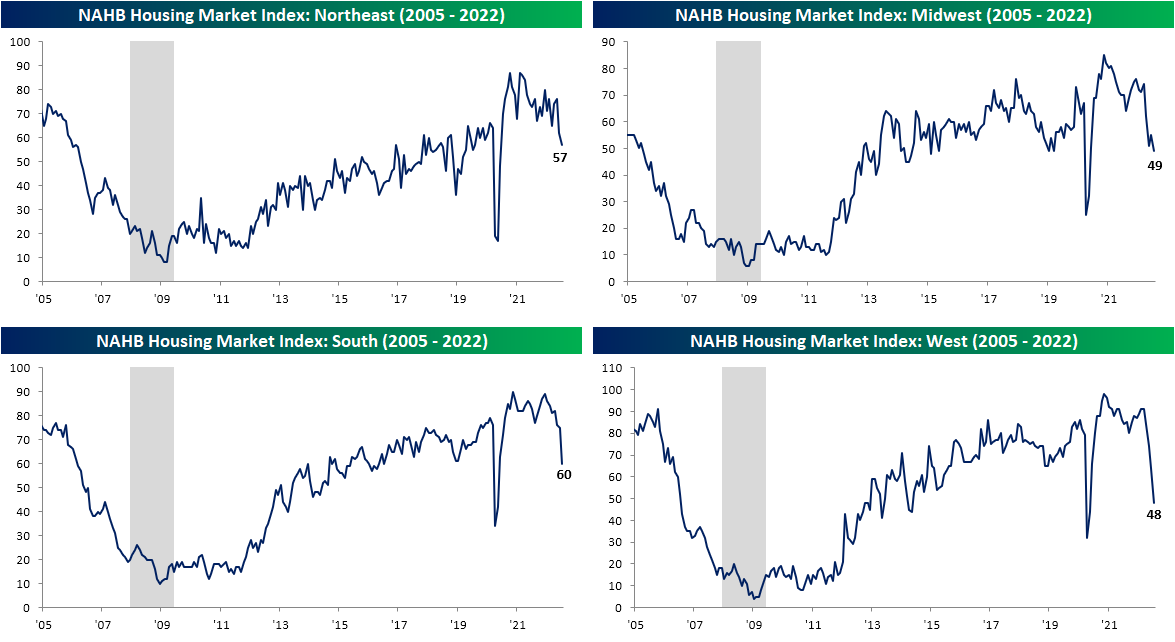

Geographically, no area of the country has been safe from plummeting sentiment, but the Northeast has held up remarkably well. Whereas the South and West saw double digit monthly declines that both were the second largest on record, the Northeast only fell five points to 57. That is a reading just shy of the top quartile of readings unlike the other regions that are in the 52rd percentile at best (South).

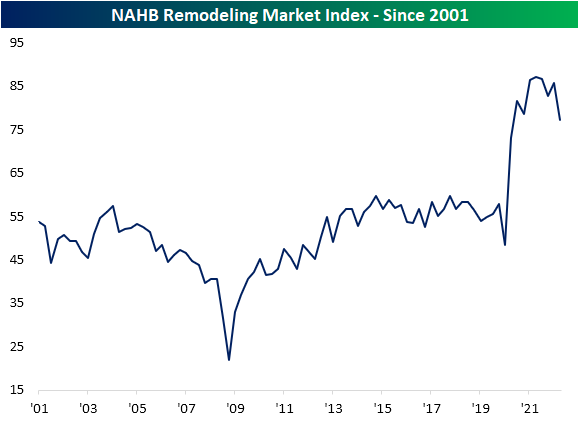

The lower sentiment for homebuilders is of course a function of rising mortgage rates and the subsequent dampening demand as a result. As for builder’s roles in existing homes, sentiment is also rolling over. In addition to today’s release, last week saw the quarterly release of the NAHB’s Remodeling Market Index measuring builder’s sentiment regarding remodeling projects. Unlike the Housing Market Index, this index remains historically elevated and down just a bit. In other words, remodeling demand has taken a hit but not to the same extent as projects to build a new home.

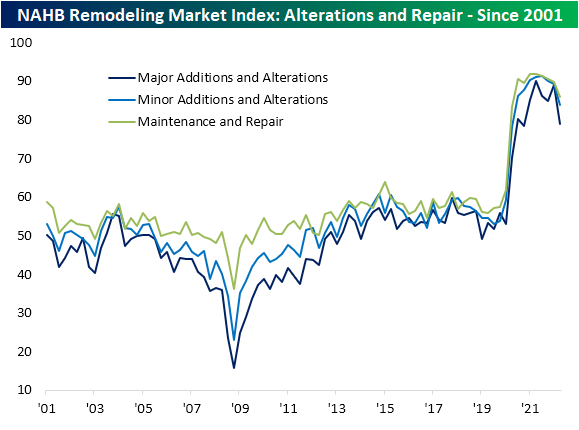

The most pronounced decline in remodeler sentiment has come from the projects carrying the highest costs ($50K or more) even though smaller project outlooks have also been falling for a few quarters now.

Backlogs have been unwinding as well even if they are historically elevated. A likely big reason for that has been a deceleration in new projects. The index for Appointments for Proposals is much less elevated in the 48th percentile compared to 56th for the headline reading or 68th for Backlog of Remodeling Jobs.

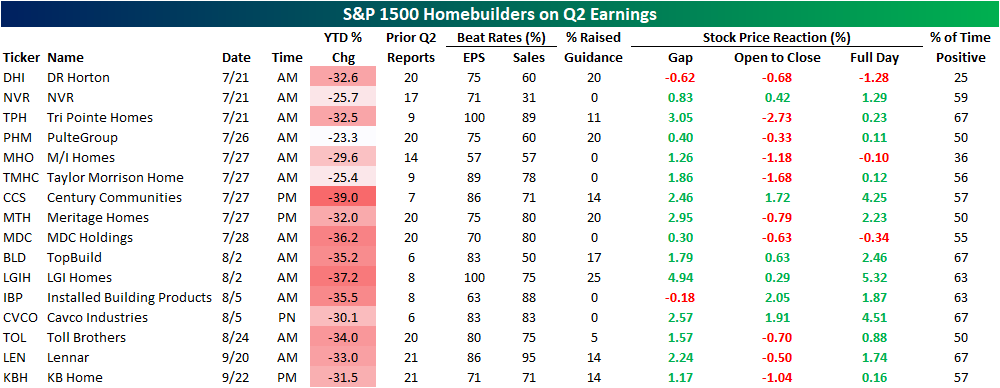

Homebuilder Earnings on Deck

While homebuilder sentiment experienced a historic plunge in the latest reading, homebuilder stocks have actually been on the move higher in today’s session. That brings the total rally off of the June low above 20%, although that is only a dent in the larger decline since late last year. The S&P 1500 Homebuilders group is currently down 31.4% since the December 10th high. Without a coincident drop alongside sentiment, homebuilders continue to hold above their 50-DMA.

Homebuilders are at a bit of a crossroads at the moment as a further move higher would definitively break the past several months downtrend whereas a break back below its 50-DMA would mark a failed breakout similar to what happened earlier this spring. If today is any indication, macro data hasn’t been a particularly strong catalyst for the industry, however, there is a huge slate of earnings in the month ahead. Later this week on Thursday, DR Horton (DHI), NVR (NVR), and Tri Pointe Homes (TPH) are all scheduled to release quarterly results. Of these, DHI has actually averaged some of the worst performance on Q2 earnings of any homebuilder. The stock has averaged a 1.28% decline on its historical Q2 earnings reaction days and positive returns only a quarter of the time. As for other notables, Q2 has tended to be the best quarter of the year for stock price performance of Century Communities (CCS), Installed Building Products (IBP), LGI Homes (LGIH), and NVR (NVR). Click here to learn more about Bespoke’s premium stock market research service.

Pumped For Some Relief

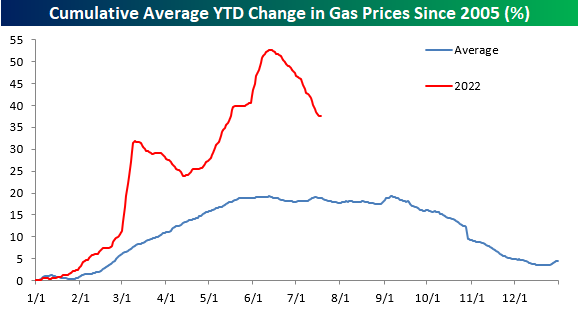

After one of the sharpest YTD surges on record, US consumers have seen a bit of relief at the pump over the last month as gasoline prices, as tracked by AAA, have seen a sharp pullback. The national average price of a gallon of gas currently stands at $4.52, which at any other point in history would have been astronomical, but compared to mid-June when the national average briefly topped $5, current prices seem downright cheap – at least on a relative basis!

The table below shows prices as of 7/18 each year going back to 2005 and where they stood on both a MTD and YTD basis. At $4.52, the national average has never been higher at this time of year, and the only year it was above $4 per gallon on 7/18 was in 2008. On a YTD basis, the average price is still up 37.6%, which is roughly double the average and median YTD gain at this point in the year, but 2021 (40.6%) and 2009 (52.6%) both saw larger YTD increases. One notable aspect of this year so far is that despite the big increases on a YTD basis, this month’s 6.6% MTD decline actually ranks as the largest MTD decline in prices through 7/18.

While the moves this year have been much more extreme than normal, average gasoline prices are following their typical seasonal pattern. Historically, prices tend to peak right around Memorial Day or into early June, and this year’s peak in prices was on June 13th. Granted, this year’s peak (50%+) was much larger than the typical YTD increase leading up to the peak, but the magnitude of the decline in percentage terms has also been steeper than normal. In order to get back down to a more normal YTD pattern, we’re going to need to see continued weakness in prices going forward. But from a seasonal perspective (and barring any hurricanes), there is a tailwind for lower prices. Click here to learn more about Bespoke’s premium stock market research service.

Besides the fact that gas prices hit record levels this year, what has made the period especially painful for consumers is how consistent the increase in prices has been. The chart below shows the y/y change in prices going back to 2005. The current level of 42.71% isn’t necessarily extreme in terms of its magnitude, but what stands out in the chart below is how long the y/y increase has stayed at elevated levels. Back in March 2021, the year-over-year change for gas prices first crossed 30%, and it hasn’t looked back since. When you start lapping 30% y/y increases, it really starts to add up! Let’s hope that this recent dip really starts to have some legs.

Bespoke’s Morning Lineup – 7/18/22 – An Up Monday For A Change

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Let me assert my firm belief that the only thing we have to fear is fear itself” – Franklin D. Roosevelt

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

What was looking like a very strong start to the week a couple of hours ago is now looking more like merely a positive start to the week as S&P 500 futures went from up well over 1% to up about 75 basis points (bps). Given the market’s tendency to kick off the week on a down note this year, though, and positive start to the week is a win. Consider this, including today, of the 29 weeks so far in 2022, the S&P 500 tracking ETF (SPY) has only opened higher on the first trading day of the week ten times.

Economic data is light today with Homebuilder Sentiment the only report on the calendar. The pace of earnings will pick up as the week goes on, but already we’ve already had reports from Bank of America (BAC) and Goldman Sachs (GS). Neither company had any major landmines, and while BAC is flat in the pre-market, GS is up over 3%.

Today’s Morning Lineup discusses earnings news out of Europe, action in Asian and European markets, and economic data from around the world.

Last Friday’s rally helped to end what was a lousy week up until that point on a positive note. Heading into the day, the S&P 500 was down for five straight days, and even after the rally, finished the week down nearly 1%. But with a strong finish and futures trading where they are right now, both the S&P 500 and the Nasdaq are poised to erase just about all of last week’s losses at the opening bell.

There’s been an awful lot of bottom talk circulating over the last few days, and the charts of the Nasdaq 100 (QQQ) and S&P 500 (SPY) have been showing some positive signals as they both managed to make higher lows last week. There’s still a lot of resistance to work through on the upside, though, as the 50-day moving averages and prior highs from this summer loom above. Given the market’s tendency to disappoint bulls in prior rallies this year, traders are increasingly less likely to give the market the benefit of the doubt and give an all-clear.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 7/17/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Labor Markets

Here’s where Tesla’s recently laid-off talent is going by Fred Lambert (electrek)

Workers who have been laid off or otherwise departed Tesla recently has headed to other tech firms, with Rivian, Apple, and Lucid Motors among the biggest recruiters. [Link]

Netherlands Poised to Make Work-From-Home a Legal Right by Lucy Papachristou (WSJ)

Dutch legislation will force employers to consider remote work requests and provide a covered reason denying their request. [Link; paywall]

Food

Learning to Love an Induction Stove by Hannah Goldfield (NYer)

While gas remains a favored cooktop for chefs, home cooks are likely to reduce greenhouse gas emissions, protect their family’s air quality, and reduce cook time. [Link; soft paywall]

Rising prices curb consumers’ taste for chocolate by Maytaal Angel and Jessica DiNapoli (Reuters)

Sweet treats are an easy item to give up for many consumers, especially when high prices for chocolate mean choco-holics are paying out the nose for their fix. [Link]

In Portugal, Taking a Dive Into Sardines by Lily Puckett (NYT)

A look into the very old and very big business of fish canning, an industry dominated by women that is having a moment thanks to foodies’ search for intense and widely available flavors. [Link; soft paywall]

China

Chinese Homebuyers Across 22 Cities Refuse to Pay Mortgages (Bloomberg)

With apartment development timelines dragging out in part due to builders’ financial challenges, owners already on the hook for payments are starting to boycott their loans in protest. [Link; soft paywall]

China Is Stealing Taiwan’s Sand by Elisabeth Braw (FP)

Taiwanese islands close to the mainland regularly see thousands of dredgers and support vehicles trespass with the goal of removing sand for use in a huge range of applications from land reclamation to concrete or glass manufacturing. [Link]

Subscriptions

Instagram now lets creators publish feed posts just for their subscribers by Chris Welch (The Verge)

Content on Instagram can now be pushed exclusively to paid subscribers, following in the steps of Twitter and adding to a similar feature for Stories. [Link]

Netflix Changes Tack With Marketing Spree for $200 Million Film by Lucas Shaw (BNN Bloomberg)

Instead of just letting users discover a new movie, Netflix is actively marketing its new blockbuster (featuring Ryan Gosling) in a bid to re-start subscriber growth and maintain its position within the streaming wars. [Link]

BMW starts selling heated seat subscriptions for $18 a month by James Vincent (The Verge)

The German auto manufacturer is testing a feature that would allow users to pay full freight for heated seats up front or pay less in monthly installments…all to access a feature that comes built into the car but can be turned on or off with software. [Link]

Market Innovation

‘The market is just dead’: Investors steer clear of 20-year Treasuries by Kate Duguid and Colby Smith (FT)

Since being reintroduced in 2020, the 20y Treasury bond has found very little interest from investors as low liquidity and weak real money interest have made it attractive to nobody. [Link; paywall]

Lumber Futures Are Getting a Makeover by Ryan Dezember (WSJ)

In a bid to expand volumes, the CME is reducing the size of its lumber future by 75%, changed the delivery point, and broadened eligible species to allow for more participation on both sides of the contract. [Link; paywall]

Approval

Most Democrats Don’t Want Biden in 2024, New Poll Shows by Shane Goldmacher (NYT)

With President Biden deep underwater in broad polling, a majority of Democrats would prefer someone else in a primary challenge; that said, a failure to renominate a sitting President would be a major shocker in the longer-term history of the US two-party system. [Link; soft paywall]

Too Much of A Good Thing

A new ‘miracle’ weight-loss drug really works — raising huge questions by Hannah Kuchler (FT)

Last year the FDA approved a weight loss drug that led to patients losing 15% of their body weight on average. Its history and approval are controversial: patients will likely need to take it long term at a monthly list price of $1,350. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!