Bespoke’s Weekly Sector Snapshot — 9/8/22

Chart of the Day: 2022 and the End of “Buy the Dip”

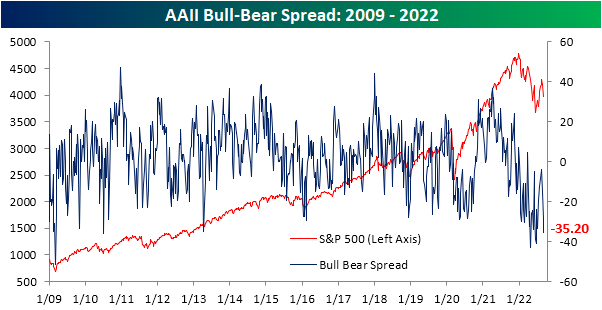

Bulls Back Below 20%

Although the S&P 500 managed to bounce yesterday and today (as of this writing), further declines in the days prior have meant sentiment continued to take a header. In the latest update, only 18.1% of responses to the weekly AAII sentiment survey reported as bullish. That marked the third consecutive decline in bulls resulting in the weakest reading since the end of April.

Bearish sentiment in turn has rocketed higher, climbing back above 50% last week and rising further to 53.3% this week. That is the highest level of bearish sentiment since the week of June 23rd and ranks in the top 2.5% of all weeks on record.

Given the large inverse moves in bulls and bears, the spread of the two has fallen deeper into negative territory after almost turning positive only a few weeks prior. We would also note that the over 30-point drop in the past month is the largest since a 47.4-point decline at the end of April and ranks as the 29th largest decline in a four-week span on record. With 23 weeks of negative readings in a row, the current stretch is now the second-longest streak of negative readings in the bull-bear spread on record.

Investors appear to be increasingly polarized between bullish and bearish sentiment as well. As optimism and pessimism have experienced wild swings, neutral sentiment has been relatively stable. Neutral sentiment only rose one percentage point this week, rising to 28.7%. That is right in the middle of its recent range. Click here to learn more about Bespoke’s premium stock market research service.

Continuing Claims Catching Up With Initial Claims

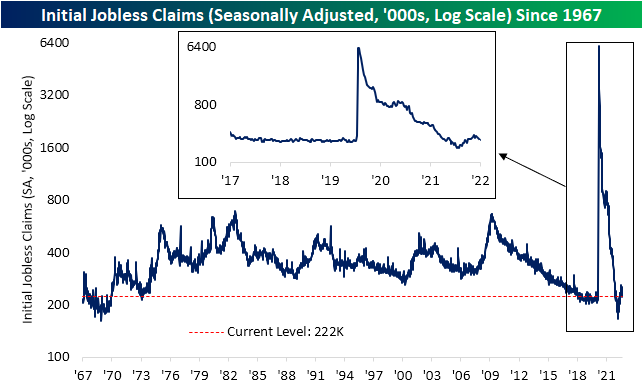

Although this year has seen seasonally adjusted jobless claims drift higher, the indicator is on a four-week-long streak of sequential declines. The latest reading released this morning fell by 6K to 222K from the downwardly revised number of 228K last week. In total, claims have now fallen by 30K during that streak of declines and are another 9K below the high of 261K from mid-July.

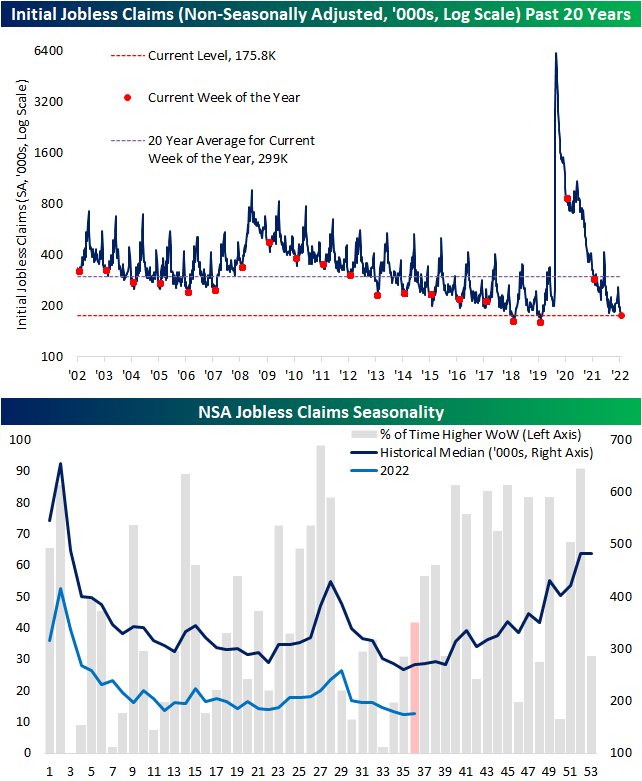

On a non-seasonally adjusted basis, claims were up slightly from 173.9K to 175.8K. Modest increases are the standard for this point of the year as claims have likely put in place their seasonal low before turning higher into year-end. As shown in the first chart below, this week’s reading is historically strong but came up short of the lows for the comparable weeks of 2018 and 2019.

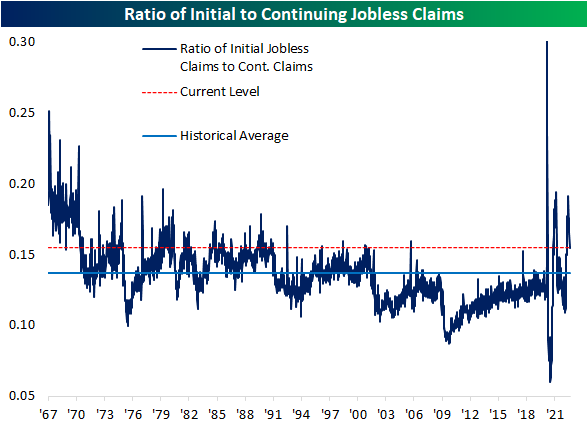

Although initial claims have been improving and came in lower than expectations, the opposite is true for continuing claims. Lagged an additional week to initial claims, seasonally adjusted continuing claims rose to 1.473 million (expectations of 1.438 million) which is the highest level since the start of April. Unlike initial claims, in spite of recent increases, continuing claims have ample headroom until they reach their pre-COVID range as current levels remain consistent with some of the strongest in over 50 years. In other words, even though initial claims have found respite and have reversed lower, the opposite is true for continuing claims which is evident through the ratio of the two having taken a sharp turn lower in recent weeks. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 9/8/22 – Listless Trading

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A government big enough to give you everything you want is a government big enough to take from you everything you have.” – Gerald Ford

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures have been trading rangebound around the unchanged line this morning as the ECB rate decision (hiked rates by 75 bps pretty much as expected) and lower-than-expected initial jobless claims have caused a pickup in trading activity generally in a lower direction. The only other indicator on the calendar in the US is Consumer Credit at 3 PM Eastern. Besides the data, there are plenty of investor conferences and even some Fedspeak on the calendar, so be on the lookout for tape bombs throughout the day.

New UK PM Liz Truss has announced a number of initiatives to help alleviate stress from surging energy prices. In a more long-term measure, she announced a lift of the ban on fracking and plans to approve more drilling for oil. In a more short-term-based measure, the new PM also announced a price cap on energy prices for consumers to take effect for the next two years. That should provide short-term relief, but the quote from Gerald Ford above should serve as a reminder – while prices may be capped, consumers will have to pay for it in some way (either through higher taxes or restrictions on the amount of energy one can use).

Investors have been able to buy and sell long-term US Treasuries via ETFs through the iShares 20+ Year US Treasury ETF (TLT) for just about 20 years now. In the first few years of the TLT’s existence, volatility in the ETF was what you would expect for a US Treasury – low. From 2003 through early 2007, the average daily move of TLT over a trailing 200-day period ranged between 0.30% and 0.70%.

Once the housing market crashed and the Financial Crisis set in, volatility in TLT surged with the average daily move breaching 1% on its way to 1.10%. As markets stabilized in 2009, volatility pulled back but never quite back down to its pre-Financial Crisis range. Then in 2011, volatility surged again as the US had its long-term credit rating downgraded in August 2011. Average daily volatility peaked in that period several months later in April 2012 and then began a multi-year decline to a range of around 0.50% per day.

Like everything else in the economy, COVID wreaked havoc on the Treasury market pushing the average daily move in TLT back up above 1%, but the exaggerated volatility was short-lived, and the market quickly returned to more stable levels by June 2021. The period of calm was just as short-lived, though. As the Fed found religion regarding inflation in late 2021 pushing long-term rates higher, volatility has once again surged. Just yesterday, the 200-day average daily move in TLT once again topped 1% for the first time since June 2020. How long this period of heightened volatility lasts remains to be seen, but if rhetoric on the part of Fed officials is to be believed, a return to calm seems a long way off.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 9/7/22

Historic Small Cap Volatility

It’s no secret that growth stocks have underperformed value stocks over the last twelve months. The trailing-twelve-month performance spread (percentage points) between the small-cap growth and large-cap value indices, two opposite ends of the equity market, is currently at -20.5 percentage points. Although this is far above the recent low of -33.9 ppts, the current reading is in the bottom 6% of all days since the mid-1994 (when both the MSCI USA Small Cap Growth and MSCI USA Large Cap Value Index were active). Interestingly, this year’s trailing twelve-month performance spread was the lowest since 2001 (unwind of the dot-com bubble). Funny enough, the spread had hit the highest level since early 2000 in 2021, as excessive performance from small-cap growth stocks has tended to reverse course after reaching extreme levels.

Small-cap growth stocks tend to trade at significantly higher valuation multiples than large-cap value stocks, which is part of the reason that small-cap growth equities have sold off at a higher rate than their counterparts. These stocks also have higher betas, so market moves have a disproportionate effect. These factors have caused the average daily percent change spread between the two indices to reach an extremely elevated level, the highest since 2000 – 2001. This measure of volatility is also yet to roll over, indicating no end to the volatility regime that has been in place. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day: Doubled Rates Dampen Demand

Apple on iPhone Announcement Days

Building upon yesterday’s Chart of the Day, we took a look into Apple’s (AAPL) intraday performance on iPhone announcement days. Today is one of those days, and although we couldn’t locate the exact announcement time for each day going back to 2008, the ones that we did find occurred at 1 PM Eastern, which is highlighted in red below.

As you can see, the stock has tended to sell off during the first hour of the day before slowly trudging higher until 1 PM Eastern. However, once the event begins, the stock has tended to decline in a sell-the-news reaction. That weakness has tended to last most of the afternoon until the final 40 minutes of trading when the stock has tended to bounce back a bit. For the entire day. AAPL’s stock has, on average, declined 78 basis points on the day of prior iPhone announcements since 2008. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Morning Lineup – 9/7/22 – Eight in a Row?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There’s nothing fair about it, it’s going to create economic hardship,” – Ryan Lance

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The above quote from the ConocoPhillips (COP) CEO from earlier this year was referring to the energy policy of the United States, but it could just as equally have been used as a response to this morning’s WSJ article that the FOMC is planning on a 75 bps rate hike at its September meeting. Whatever your views are regarding the path of inflation and whether a 75 bps hike is actually needed, the impacts will create some level of hardship on what is already a weakening economy. Chair Powell has admitted as much in numerous comments saying that the FOMC’s fight to reverse the post-COVID inflation surge will be ‘painful’.

Futures were modestly higher before the WSJ article was published but have since reversed into negative territory with the S&P 500 indicated to open down by 0.30% with the Nasdaq indicated lower by a similar amount. The Nasdaq is already down seven straight days, which is the longest losing streak since November 2016, and that streak ultimately went on for nine days before ending. Crude oil prices are modestly lower and treasury yields are lower as well.

Maybe we were just overdue for a losing streak like the Nasdaq is currently in the midst of now. Before this one, the last losing streak of seven trading days was right before the 2016 election, and the gap of 1,466 trading days between these two streaks was the longest in the Nasdaq’s history. Prior to the current period, the longest gap between 7-day streaks was from late 2001 until 2006, and the only other gap of over 1,000 trading days ended in January 2016.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.