Bespoke’s Morning Lineup – 9/22/22 – Central Bank – Palooza

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“No one knows whether this process will lead to a recession.” – Jerome Powell

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures are modestly higher following a slew of central bank rate hikes around the world and a currency intervention from the BoJ. Jobless Claims were just released for the latest week and came in at 213K which was 4K below consensus forecasts. Continuing claims were likewise lower than forecasts coming in at a level of 1.379 million versus forecasts for a level of 1.418 million. While yesterday’s close at the lows was disheartening for the bulls, when you consider how the market has performed following positive initial reactions to the Fed this year, maybe the Fed day weakness wasn’t so bad.

Years before he became Chairman of the Federal Reserve, Jerome Powell received an undergraduate degree from Princeton, a law degree from Georgetown, was a partner at the Carlye Group, and even served as under-secretary of the Treasury for domestic finance. He’s not only extremely intelligent, but unlike many of his colleagues on the FOMC, he has real-world experience of how the private sector and financial markets work.

Given his experience, we’re sure Powell is familiar with the yield curve and how its shape impacts the economy. Specifically, when the curve inverts and short-term interest rates rise above long-term rates, it tends to slow down economic activity. While at the Carlyle Group and the private equity firm that he started after (Severn Capital Partners), he probably experienced these slowdowns firsthand and was able to make investments on good terms for his clients.

The Federal Reserve’s preferred measure of the yield curve is the spread between 3-month and 10-year US Treasuries, which still has a modestly positive slope at about 25 basis points (bps). Besides that, another widely followed point on the curve is the spread between the 2-year and 10-year US Treasuries (2s10s). As of yesterday’s close, the 2s10s curve inverted to the tune of 52 bps making it the most inverted it has been since 1982! It was nearly as inverted in April 2000, but back then the maximum point of inversion was 51 bps. Think about that for a minute. A lot of people – maybe up to half- reading this right now weren’t even alive the last time the 2s10s curve was as inverted as it is now! Looking at the chart below, since the mid-1970s, there has never been a period when the 2s10s yield curve was as inverted as it is now that a recession wasn’t just over the horizon.

Getting back to Chair Powell, at one point in his press conference yesterday, he responded to one question with the answer that “No one knows whether this process will lead to a recession.” Let’s get this straight. The yield curve is extremely inverted, GDP growth in the first two quarters of this year has already been negative, and forecasts for growth in Q3 have been steadily declining as we close out the month. All this is before the recent unprecedented round of 75 bps rate hikes have had the opportunity to filter through the economy, and yet the Fed Chair is unsure of whether the US economy is either already in or on pace for a recession. Now we know that it’s not a good look for a Fed Chair to forecast a recession as the base case scenario, but does he really believe what he’s saying?

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 9/21/22

Bespoke Baskets Update — September 2022

Chart of the Day: Decile Analysis Since the Mid-August High

B.I.G. Tips: Bear Market Patterns – The Third Leg Lower

Bespoke’s Morning Lineup – 9/21/22 – Washington in Focus

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The worst of COVID may be behind us, but the economic challenges we face are no less daunting.” – Jane Fraser

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Despite some bellicose comments from Putin overnight regarding the war in Ukraine, futures are higher this morning as US Treasury yields are modestly lower and oil prices trade moderately higher. There’s also been some positive earnings news as General Mills (GIS) reported better than expected EPS and raised guidance, while Coty (COTY), a smaller company, raised Q1 guidance and sees full-year estimates inline with forecasts. You can read all you want into these early moves, but it’s likely to all be irrelevant by the end of the day after the FOMC rate decisions and Powell’s press conference.

The comments above come from the prepared remarks of Citibank CEO Jane Fraser in testimony to Congress today. Mid-term elections are just over a month away, so our elected representatives need some campaign soundbites. What better way to do that than bring a bunch of bank CEOs to DC in person and give them a good scolding? Anyways, the prepared remarks of Citibank CEO Jane Fraser and JP Morgan Chase CEO Jamie Dimon, who will say that “many Americans are being crushed by high inflation eroding real incomes, particularly from higher prices on gas and food,” don’t paint a very positive picture for the economy. Whatever happened to the roaring 20s we were supposed to have after COVID?

On the same day that bank CEOs present these dour economic forecasts, the FOMC will announce what is expected to be an increase of at least 75 basis points (bps) in the Fed Funds rate which would be the third straight increase of at least that magnitude. Not only that but Powell is widely expected to set the stage for more rate hikes to come. How much more in rate hikes that follow today’s meeting may depend on what the stock market does. In an article earlier this week, Nick Timiraos at the Wall Street Journal reported that Fed officials were unhappy with the market’s positive reaction following the July rate hike of 75 bps. Powell’s displeasure with the market rally was so intense that he scrapped his prepared Jackson Hole speech in favor of a more direct and forceful message that the FOMC would “Keep At It” and do everything it could to bring inflation down.

Powell got exactly what he wanted from the market following that speech as stocks have been cratering ever since. Minneapolis Fed President Neel Kashkari reinforced the Fed’s intent to get stock prices lower when he remarked that “I was actually happy to see how Chair Powell’s Jackson Hole speech was received…I certainly was not excited to see the stock market rallying after our latest Federal Open Market Committee meeting”.

Investors always discuss the Fed’s dual mandate of maximum employment and stable prices, and lately they have questioned whether the Fed has shifted to focus on a single mandate of stable prices. With Powell taking the unusual step of completely ditching his Jackson Hole speech last month and then Kashkari outright endorsing the negative market reaction to Powell’s speech, the idea of a single mandate Fed – one intent on lower stock prices – now seems accurate. Now, if only we knew how much of a bear market would satisfy the Fed’s new mandate.

When you have members of the Federal Reserve openly rooting for lower stock prices, you can’t be surprised by the performance of equities this year, but when you put it in a historical perspective, 2022 ranks right up there with the worst of them. Yesterday, the S&P 500 fell more than 1% for the 45th time this year. That works out to 25% of all trading days, or more than one 1% decline a week. Since the five-trading day week started in 1952, the only other years with a higher percentage of 1% down days were 1974, 2002, and 2008. With declines of 29.7%, 23.3%, and 38.5%, respectively in those years, this year’s decline of 19.10% seems pedestrian.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

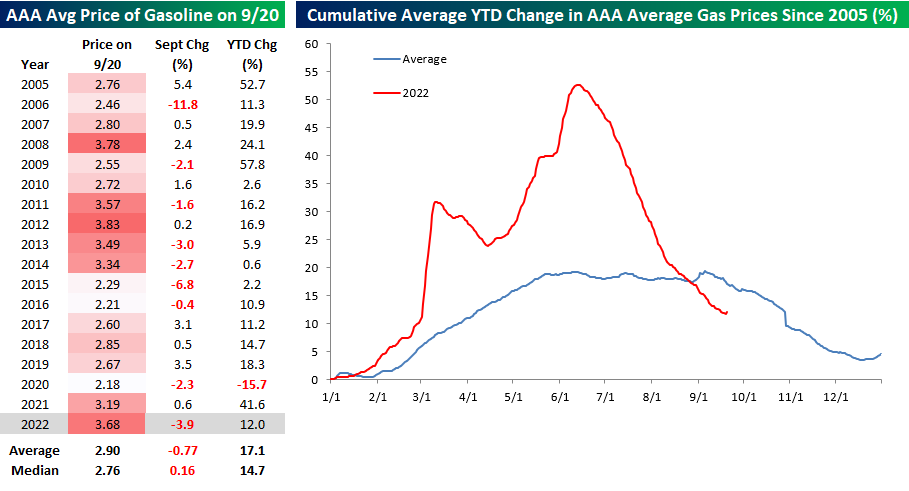

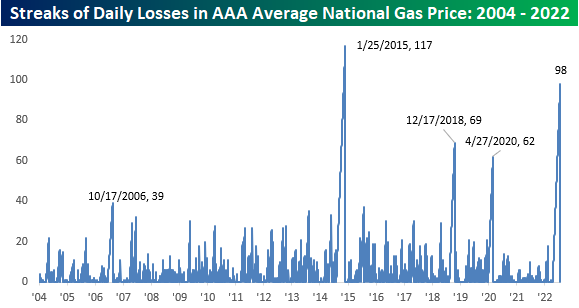

The Streak is Over

After falling every day since June 14th, the average price of a gallon of gasoline in the United States, according to AAA, rose yesterday. That ends what was the second-longest streak of consecutive declines going back to at least 2005. Had the streak lasted another three weeks, it would have gone down as the longest on record, exceeding the 117 days from back in 2015, but it’s ironic that this streak began back in mid-June when the Federal Reserve started to panic about inflation and leaked plans to hike rates by 75 bps at its June meeting to the WSJ and is now ending on a day when the Fed is expected to hike rates by at least 75 bps for an unprecedented third straight meeting.

While the streak is over, it still doesn’t diminish the fact that prices at the pump have been in freefall since that peak in June, falling by 27%. Prices at the pump are down close to 4% in September alone. While the national average price has only been higher at this time of year two other times (2008 and 2012), the 3.9% decline this month is larger than average. Even more surprising is the fact that with prices at the pump up 12% YTD, they are actually up less YTD than average for this time of year. There’s no dismissing that inflation continues to be a major problem, but most people probably wouldn’t believe that gas prices are up less this year through 9/20 than they are in the average year. Click here to learn more about Bespoke’s premium stock market research service.