Chart of the Day: Smart Money Checkup

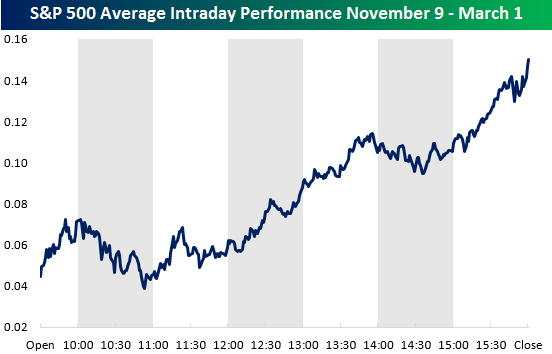

The “Smart Money Indicator” suggests that the “smart money” trades at the end of the trading day once all of the day’s events have shaken out, while the “dumb money” trades at or near the open in reaction to the day’s news. We like to track the intraday action of the market over time. While we’re not totally on board with the “Smart Money” theory, we do like to see the market finishing the trading day strong. Buying in the final hour or two of the trading day means investors are comfortable owning shares overnight. A market that opens up strong and then drifts lower throughout the trading day is one we’d prefer to avoid.

Below is a chart showing the average intraday pattern that the S&P 500 took from the close on Election Day 2016 (11/8/16) through the index’s last all-time closing high made on March 1st. This was a period where the market experienced a major move higher, and aside from slight pullbacks from 10 AM to 11 AM ET and 2PM to 2:30 PM, investors were buying, buying, buying all day long. The buying was especially strong in the final hour of trading, which suggests institutional investors were rushing to put money to work. The post-election move through the end of February was a massive buying event that brought quite a bit of new money into the market.

So how has the intraday pattern looked since the market peaked on March 1st? Have investors been selling into the close or stepping in to “buy-the-dip” late in the day? In today’s Chart of the Day (available to all paid clients), we answer these two questions and provide a chart of the S&P’s intraday pattern during the month of March. Start a no-obligation two-week free trial to Bespoke’s research platform to see the report now.

B.I.G. Tips – Economic Indicator Diffusion Index Near 52-Week Highs

Fixed Income Weekly – 3/29/17

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s note, we take a look at the US Treasury term structure and what’s likely to drive curve moves going forward.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

Gas Prices Sputtering Along

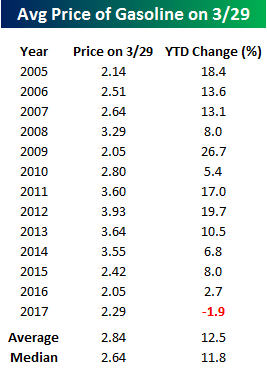

It’s been awhile since we last provided an update on national average gas prices, but recent trends are definitely worth highlighting. The table to the right shows the YTD change in gas prices based on AAA data this year and at the same point in each prior year dating back to 2005. With average prices at the pump down nearly 2% on the year, this is the first year where prices have actually been down YTD at this point in the year. This is a pretty big divergence from the overall average gain of 12.5% that is normal for this point in the year. Looking at the year by year returns, there has definitely been a trend in recent years where prices didn’t start off the year as strong as they have in the past, but this year’s decline is a bit extreme.

It’s been awhile since we last provided an update on national average gas prices, but recent trends are definitely worth highlighting. The table to the right shows the YTD change in gas prices based on AAA data this year and at the same point in each prior year dating back to 2005. With average prices at the pump down nearly 2% on the year, this is the first year where prices have actually been down YTD at this point in the year. This is a pretty big divergence from the overall average gain of 12.5% that is normal for this point in the year. Looking at the year by year returns, there has definitely been a trend in recent years where prices didn’t start off the year as strong as they have in the past, but this year’s decline is a bit extreme.

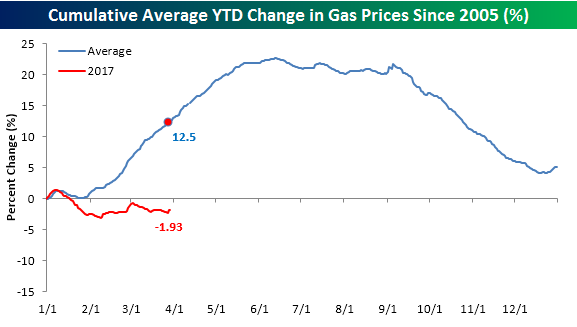

The chart below further illustrates this trend as it compares changes in prices YTD this year to a composite of the average YTD change for all prior years since 2005. By this point in the year, prices are typically already in rally mode leading up to the summer driving season. With oil prices weak this year, though, that seasonal lift has yet to materialize.

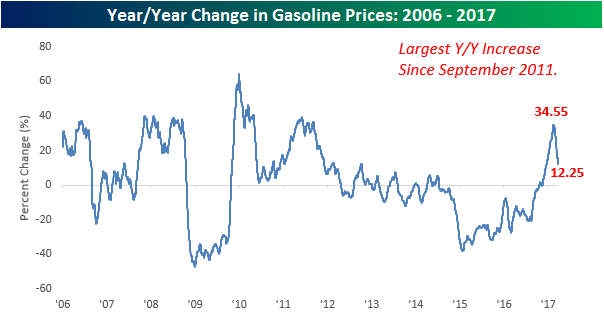

Finally, the chart below shows the year/year (y/y) change in gas prices going back to 2006. After prices bottomed in early 2016, the y/y change in prices began to recover and quickly accelerated to the upside the further away we moved from the lows. In late 2016, the y/y change in prices turned positive for the first time in over two years, and then quickly spiked to over 30% in February. As quickly as that y/y change increased, though, it has been declining even faster and is now just barely in double-digits at 12.25%, and if prices don’t start accelerating to the upside the y/y change will likely fall back to negative levels. The reason this is important is that it illustrates a trend we have seen throughout the commodity space in recent months, where base effects have had an exaggerated impact on y/y prices changes. Now that those low levels are falling further out than a year, though, the percentage changes are looking a lot less dramatic. This is also likely to start showing up in inflation statistics which have recently been lifting to multi-year highs on a y/y basis. Going forward, though, some of that upward pressure is likely to subside.

ETF Trends: International – 3/29/17

Natural gas and Energy names have led the way in terms of trailing 1 week returns, with micro caps, Latin America, and biotech also performing well. Gold miners, frontier markets, and a number of developed market FX ETFs are the worst performers.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Looking For Action? S&P 1500 Most Volatile Stocks

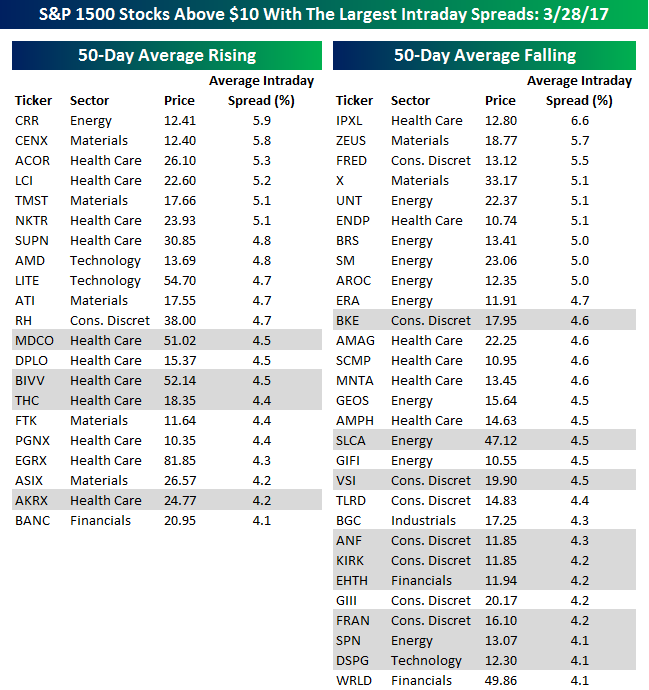

For traders with a short-term time horizon who are looking for big moves over a short period, we have updated our list of the S&P 1500 stocks trading above $10 that have the largest intraday high-low ranges (based on the average percent spread between the intraday high and low over the last 50 days). The stocks are grouped based on whether they have a rising or falling 50-day moving average (DMA). Stocks highlighted in gray are new to the list this month.

The S&P 500 may be within 2% of its all-time high, but the majority of stocks making up our list of most volatile stocks are currently in downtrends. As shown below, just 21 stocks have rising 50-day moving averages, while 29 have 50-DMAs that are in decline. Of the 50 stocks listed, just fifteen currently have average daily ranges of more than 5%, further illustrating how overall volatility is low. Also, of those fifteen stocks, just five are trading above $20 per share. In terms of sector representation, seven out of the eleven major sectors made the list. Health Care is the most well-represented sector with 17 stocks, followed by Energy with ten, and Consumer Discretionary with nine. Looking through the list, you’ve probably never heard of most of the names listed, but there are some household names including AMD, Restoration Hardware (RH), which are both in uptrends, as well as US Steel (X) and Abercrombie (ANF), which are in downtrends. Finally, given that most the stocks have relatively low share prices, they may be volatile, but they don’t necessarily have very large swings. That said, the highest priced stock listed (Eagle Pharma- EGRX) trades at over $80 per share, implying an average daily high/low range of just over $3 a day.

The Closer — Consumer Confidence Cruises — 3/28/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at extremely strong consumer confidence figures reported today.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

ETF Trends: Fixed Income, Currencies, and Commodities – 3/28/17

Mexico continues to outperform as the peso rallies; Mexican unemployment made a new low for the current cycle today. Biotech, European equities, Canada, and semiconductors are also up over the past week. Underperformers in the past five trading days include REITs, broker dealers, and commodity plays.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Bespoke Stock Scores: 3/28/17

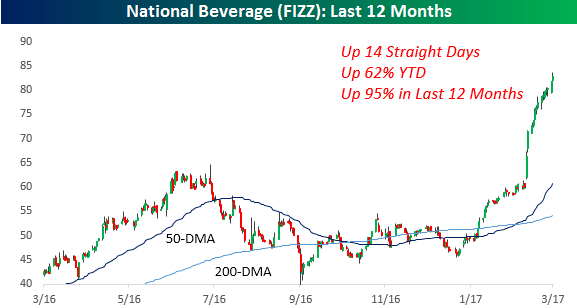

FIZZ Fizzes

We’ll be the first to admit that there are a lot of nutty looking charts out there, but one of the contenders for craziest chart has to be National Beverage (FIZZ). After reporting solid earnings earlier this month, the stock has traded higher for 14 straight days, during which it has rallied 38%. In those 14 days, FIZZ has also closed higher than it opened every single day. YTD the stock is already up 62% and its one-year return is 95%. Not quite a double, but close. So what does National Beverage do that has resulted in such strong performance? An energy drink? A miracle medical elixir? A hangover free alcoholic cocktail? A liquid cannabis drink?

No to all of those. National Beverage’s specialty drink is good old fashioned seltzer water. Sure, it’s a trendy looking can and name, but it’s still seltzer water – the same stuff you can buy at the supermarket for under 50 cents a liter. You have to give the company credit, though, because if they’ve managed to be this successful on the back of selling seltzer water, they deserve every penny. It also doesn’t hurt that three-quarters of the company’s outstanding shares are held by the company’s founder, which doesn’t leave a whole lot of shares left to trade in the secondary market.