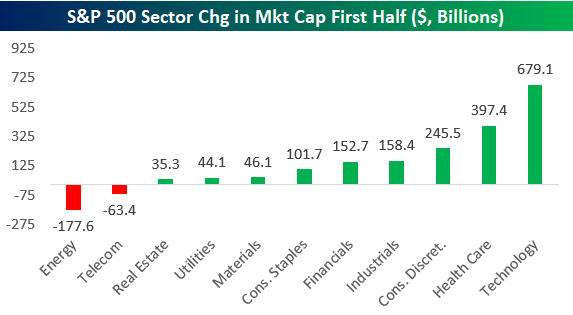

S&P 500 Sectors in First Half 2017

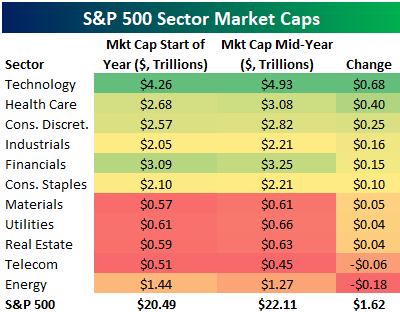

Below is a look at the change in market cap experienced by the S&P 500 and each of its eleven sectors in the first half of 2017. The members of the S&P 500 had a combined market cap of $20.49 trillion at the start of the year, and they added $1.62 trillion in the first half. This leaves the S&P 500’s current market cap at $22.11 trillion.

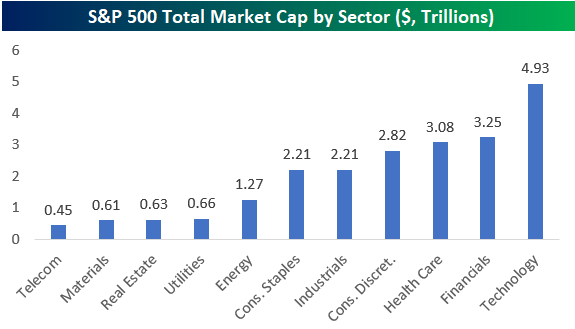

Of the eleven sectors, Technology gained the most in market cap at roughly $680 billion — moving from $4.26 trillion at the start of the year up to $4.93 trillion at the end of June. Health Care, Consumer Discretionary, Industrials, and Financials all added more than $150 billion in market cap.

Only two sectors — Telecom and Energy — saw a decline in their market cap during the first half. The Energy sector lost the most in market cap in the first half at -$177.6 billion.

Click here to start a no-obligation two-week free trial to our premium research platform.

The Closer — Mixed Indicator Monday — 7/3/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we review very mixed economic data from the US today, including ISM, vehicle sales, construction spending, and an unlikely piece of data from Mexico that speaks to the US economy’s current outlook. We also take a look at the huge rotation into Transports with the Dow Jones Transports index breaking out to new all-time highs today.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

B.I.G. Tips – 2017 First Half Decile Analysis

Bespoke Stock Seasonality: 7/3/17

ETF Trends: US Sectors & Groups – 7/3/17

Oil continues its strong performance among the world of ETFs that we track, up 7% over the past 5 days. Steel and Banks are also notable outperformers. On the other hand, Miners and Real Estate are underperforming, which has been a constant trend over the past couple sessions. Additionally, Biotech has slowed down after its recent strong performance, down just over 3% this week.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

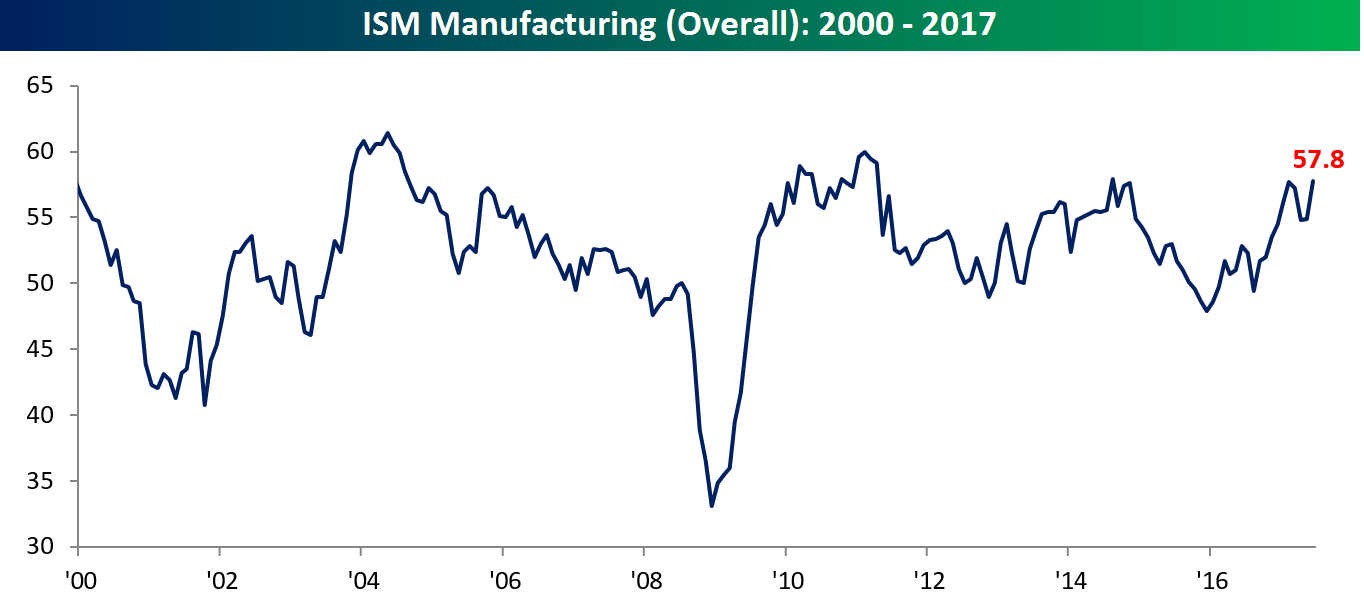

ISM Manufacturing Near a Six-Year High

While economic data continues to come in mixed to generally weaker relative to expectations, the ISM Manufacturing report for June was very strong on an absolute basis and relative to expectations. While economists were expecting the headline index to come in at a level of 55.1 from last month’s level of 54.9, the actual reading came in at 57.8, which is just shy of the six-year high of 57.9 back from August 2014.

Want to see more analysis like this? Click here to start a no-obligation two-week free trial to our premium research platform.

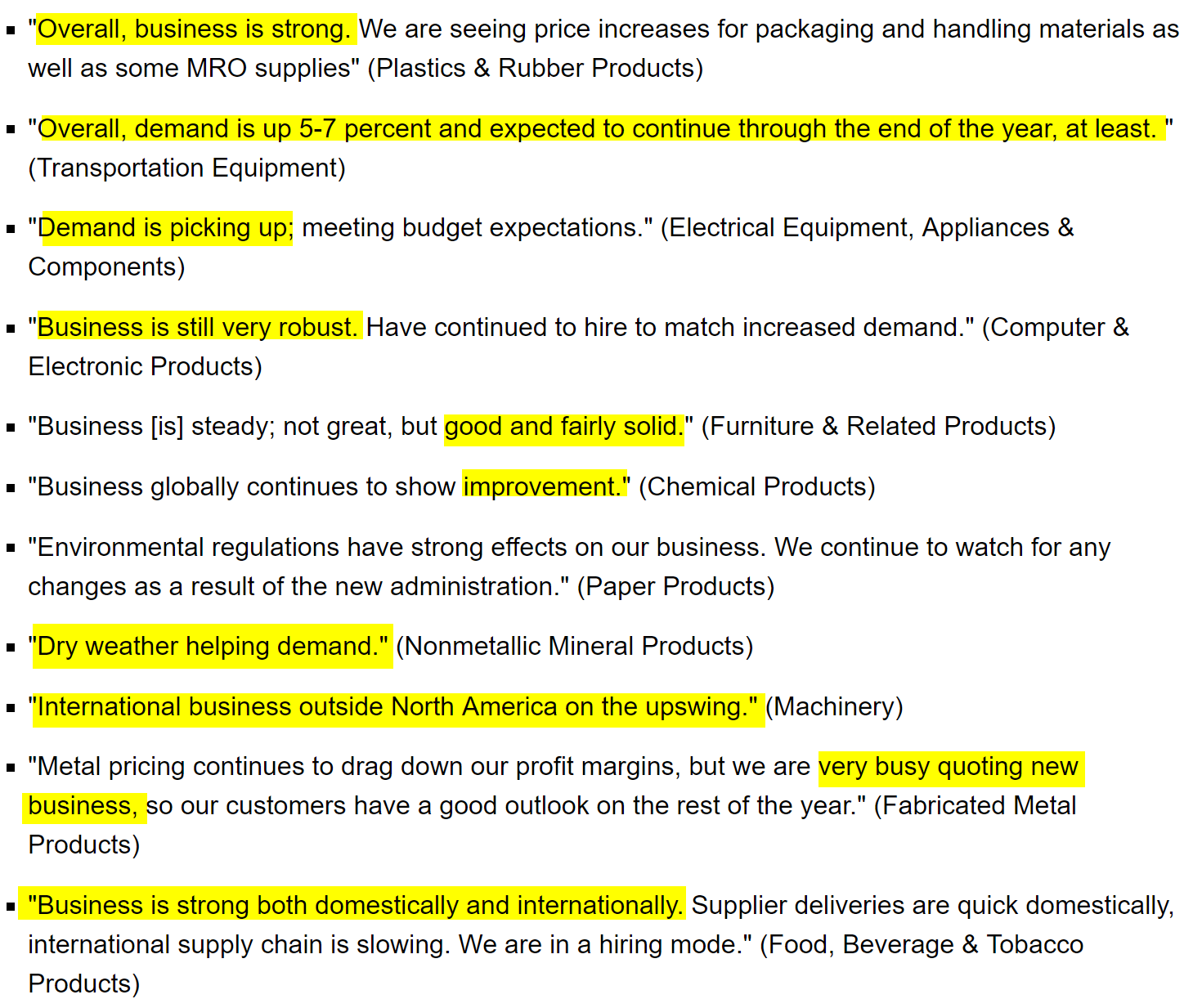

Not only was the headline index strong, but the commentary also paints a picture of robust activity. Below we have included a snapshot of some of the selected commentary from this month’s report. With the exception of one comment concerning environmental regulations, every other one suggests steady, solid, and or strong business activity.

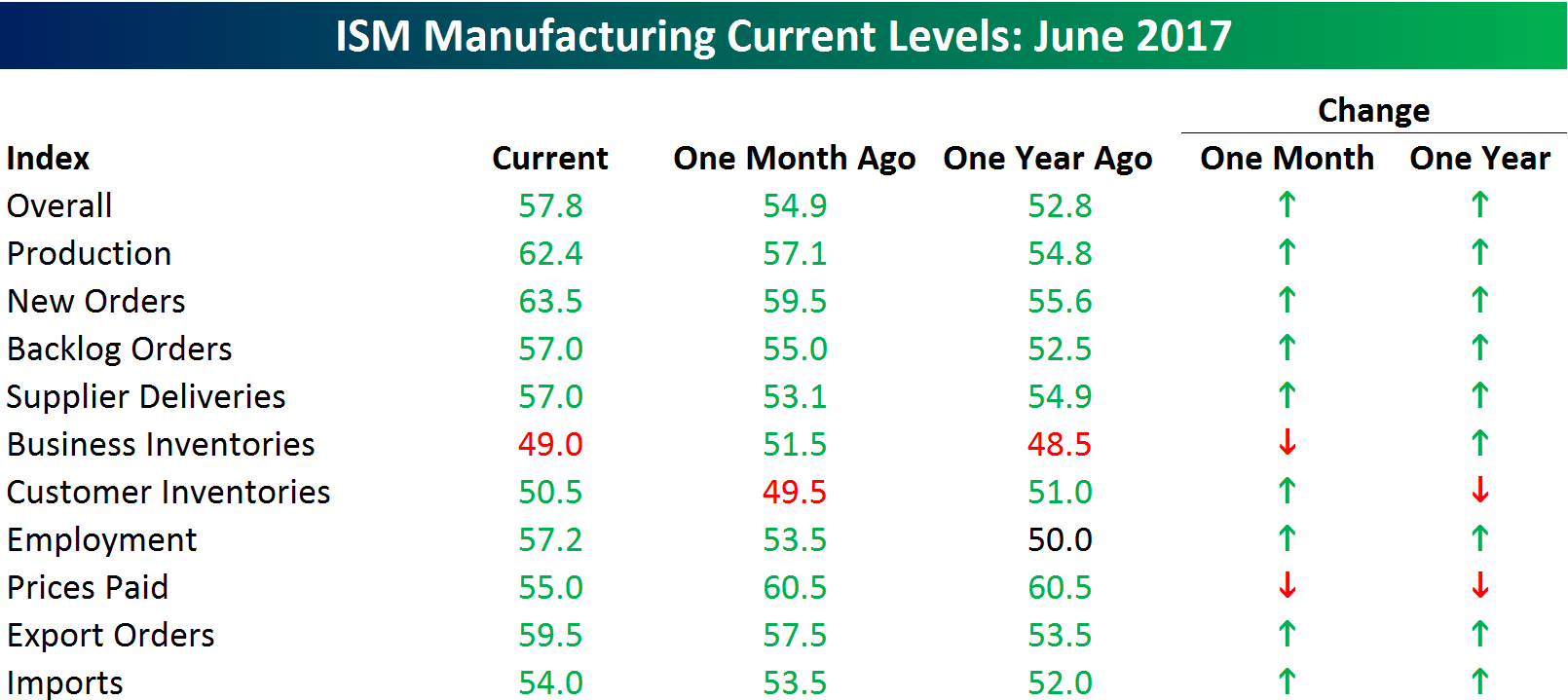

The internals of the report further confirm that positive tone. Of the ten sub-indices in the report, all but two showed a m/m and y/y improvement in June. The biggest increases on a sequential basis were Production and New Orders. On the downside, Prices Paid was far and away the largest decliner in June.

July “Old Reliables”

Every Monday (or the first trading day of the week), Bespoke Premium and Institutional clients receive our S&P 500 Stock Seasonality report. Using the last ten years worth of price data, our Stock Seasonality report looks at the median returns for the S&P 500, its eleven sectors, and its 500 individual stocks. In the report, we highlight the five stocks in each sector that have historically been the best and worst performers over the next two weeks. For each stock, we also include information such as median returns, the percent of time each stock or sector is positive/outperforms the S&P 500, and its historical performance over the next two weeks for each of the last ten years. To see a sample, check out a recent report here. To receive regular access to the full S&P 500 Stock Seasonality report, sign up for a Bespoke Premium membership now.

With July kicking off today, we wanted to highlight S&P 500 stocks that have been the most consistent to the upside during the entire month over the last ten years. The table below lists the 13 stocks in the S&P 500 that have been up during the month of July in at least nine of the last ten years. Leading the way higher among the stocks listed is Celgene (CELG) which has seen a median gain of 11% with gains in every July except 2011 when it fell 1.7%. Behind CELG, another biotech — Alexion Pharma (ALXN) — has seen a median gain of 9.7% with gains in July in each of the last ten years.

Number three on the list is Wynn Resorts (WYNN), which has been up in every July over the last ten years except 2012. Over those ten years, the stock has seen a median gain of 7.4%. WYNN is digging itself into a bit of a hole to start the month as the stock is down 3% following weaker than expected revenue growth in Macau gaming revenues, but there are still another 30 days left in the month, so we shall see.

The fourth and fifth best-performing stocks are two that are going in seemingly different directions. Amazon.com (AMZN) has been a star for the last several months, and July also tends to be a good month as the stock has seen a median gain of 7.0% with gains in each of the last ten years except for 2014. Behind AMZN, IBM has been a proverbial stick in the mud for years now, but at least July has been good for the stock as it has seen a median gain of 5.4% with gains in every July except 2015 when it fell just 0.4%.

Obviously investors shouldn’t trade solely on the calendar, as macro or stock-specific events can come up and trump seasonal tendencies. That being said, there certainly is evidence that the market and many stocks do indeed follow seasonal patterns, so it pays to be aware of them

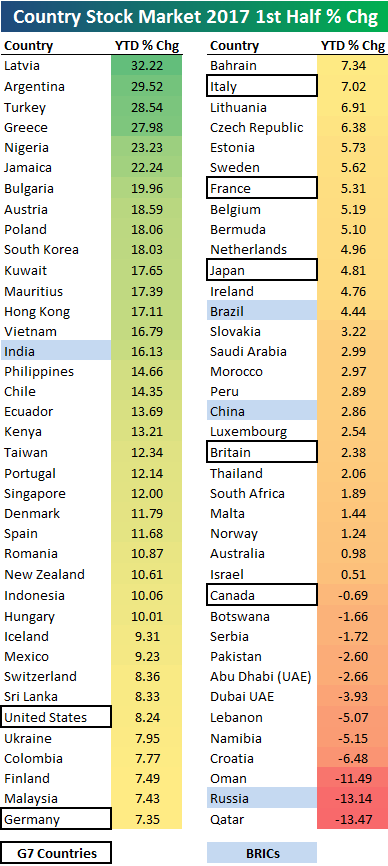

2017 First Half Global Equity Market Returns — Latvia Takes Top Prize

Below is a look at the performance of 76 country stock markets around the world in the first half of 2017. Returns are in local currency. The average first-half percentage change for all 76 countries was 7.84%, and 84% of countries were in the green.

As shown, Latvia takes first place in the first half with a gain of 32.22%, followed by Argentina (29.52%), Turkey (28.54%), and Greece (27.98%). The United States was the top performing G7 country in the first half with a gain of 8.24%, followed by Germany , Italy, France, and Japan. Canada was the worst G7 country with a decline of 0.69%.

Of the 4 BRICs, India was up the most with a gain of 16.13%. Russia was the only BRIC in the red with a decline of 13.14%.

Russia was the second worst stock market in the first half behind only Qatar, which fell 13.47%.

Want to see more analysis like this? Click here to start a no-obligation two-week free trial to our premium research platform.

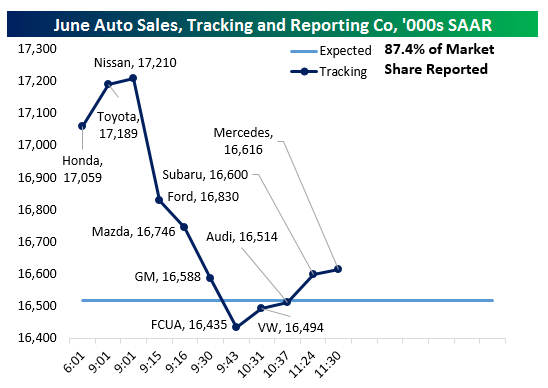

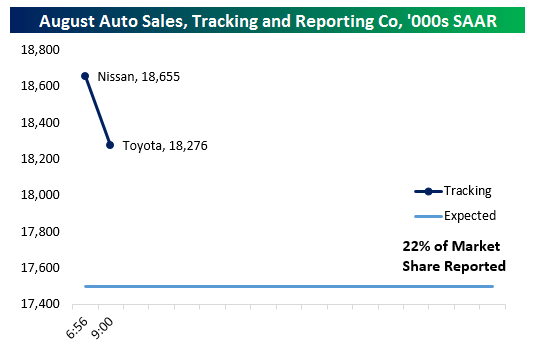

Auto Sales: Don’t Call It A Comeback

Update 2 11:49 AM: Strong sales growth from Volkswagen (rebounding off post-diesel scandal market share lows) and Subaru (gaining share in leaps and bounds from a relatively low starting point, but making new highs) have helped push our tracker for industry sales pace in June back above estimates. Currently we are tracking a very small beat despite enormous sales declines from the largest US auto makers. Fiat-Chrysler’s cringe-worthy declines actually drove our sales tracker below estimates at one point, and Toyota is the only major to report YoY volume growth. Generally speaking, smaller car companies have been able to do a better job growing sales than the large US brands.

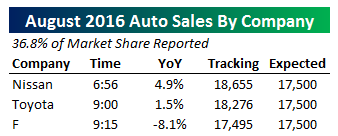

Update 1 9:34 AM: While the industry was looking pretty strong prior to 9:15, Ford, Mazda, and GM reports around that time put an end to the extremely strong versus expectations tracking data we discuss below. As shown in the table at right, all three companies reported large NSA sales declines YoY, and had a combined negative impact of nearly 700,000 SAAR on our tracker. With 66% of the industry now reported, instead of strong gains that were indicated by tracking this morning, it’s now possible that the industry will miss estimates entirely! We will continue to update our tracker as new sales data is released from manufacturers throughout the day.

Auto sales have strung up a series of brutal defeats recently as sales pace has sagged to the mid-16mm SAAR range from over 18mm SAAR at the recent peak. That includes a string of misses in recent months that have seen analysts drastically over-estimate sales figures for the industry. .In June, however, we’re getting the opposite. As of this writing, with about one-third of the industry reported, auto sales are tracking a beat versus expectations per our seasonal and trading day adjustment of raw manufacturer sales figures. Honda, Toyota, and Nissan have all bested analyst estimates, and have together put the industry on pace to handily beat the expected 16.52mm SAAR sales pace that analysts had forecast for the month. We’ll continue to update this post throughout the day as other manufacturer sales figures are released.