Bespoke’s Morning Lineup – 11/14/19 – Walmart Ends on a Positive Note

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Above Average, Consumer Credit, CPI Slowing, Taxable Insight – 11/13/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a recap of the happenings on Capitol Hill as impeachment proceedings began alongside Fed Chair Powell’s visit. Next, we take a look at the S&P 500’s historic streak above its 50-DMA without any back to back declines over the past 25 days. Then we move onto a massive slug of macroeconomic data including the New York Fed’s quarterly household debt numbers, today’s CPI release, and the monthly budget statement.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Dividend Stock Spotlight: Texas Instruments (TXN)

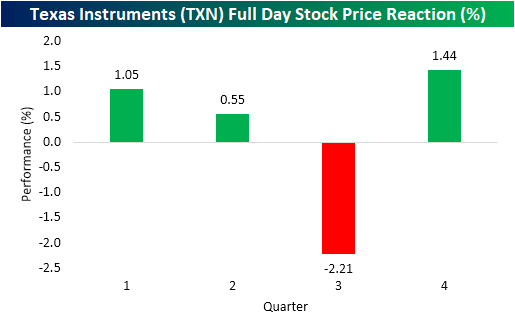

About three weeks ago, Texas Instruments (TXN) reported a weak quarter with EPS and sales both below estimates alongside lowered guidance, a reverse triple play. In response, the stock dropped sharply the following day (October 23rd) with a decline of 7.48%. That was the largest decline on earnings since October of last year when the stock fell 8.22% and was the seventh-largest decline on earnings for all quarters since 2001.

While that decline may sound worrying, it is important to take seasonality into account. The third quarter earnings report has by far been the weakest in terms of the stock price reaction for Texas Instruments. In response to all third-quarter earnings report since 2001, TXN has only risen 31.6% of the time; averaging a full day decline of 2.21% the day after the report. That is the only quarter that has averaged a decline.

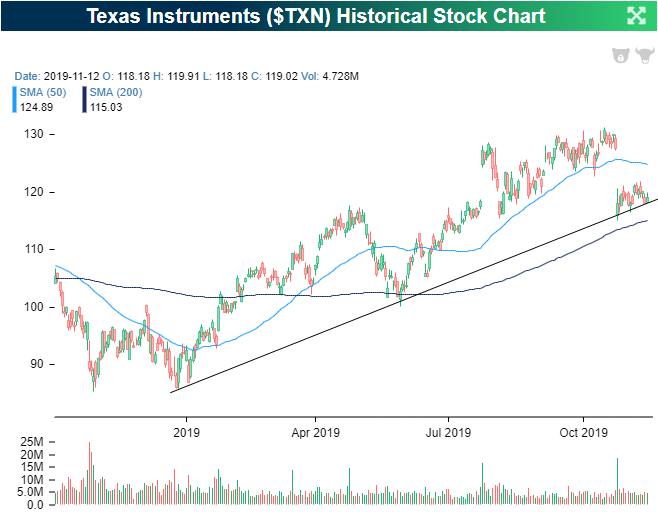

Regardless of seasonality, that massive decline on earnings did some technical damage to TXN, but not all was lost. The gap down sent TXN collapsing through its 50-DMA from which it has yet to retake. Fortunately, TXN found support right around the late April highs at ~$116, and the stock has not moved below the price from that gap down on earnings ($115.91). In other words, things have not gotten worse since that initial decline on October 23rd. In fact, TXN has been grinding higher along a longer-term uptrend line.

Adding to the attractiveness of Texas Instruments is a solid dividend currently yielding over 3%. That is the fourth-highest yield of all S&P 1500 semiconductor stocks. Not only is this a higher yield than other stocks in the industry, but the dividend also has an extensive history. The company has paid shareholders uninterrupted for every quarter since it was first declared in 1962. Texas Instruments has also grown the payout for each of the past 15 years. While some other high yielders in the space like Intel (INTC) or Broadcom (AVGO) may have a lower valuation on a price-to-earnings basis, the dividends do not appear to be as safe as the payout ratios top 90%. TXN on the other hand only has a payout ratio of 50.8%. This means the safety of TXN’s dividend appears much more intact than its competitors.

TXN has been a bit of a black sheep amongst the semis. Other quarterly reports this earnings season were strong, including triple plays from major players: Intel (INTC), Qorvo (QRVO), and Taiwan Semiconductor (TSM). Price action amongst other semis has similarly been stronger than TXN as well. As shown in the charts of other large-cap semiconductor stocks taken from our Chart Scanner, across the industry there have been several breakouts. In other words, even though TXN has lagged the rest of the sector recently, it is not as though the picture of the entire space is in bad shape. Start a two-week free trial to Bespoke Institutional to access our full library of reports and interactive tools.

Bespoke’s Daily Sector Snapshot Report

Along with numerous interactive tools on our website that investors can use to analyze the eleven major S&P 500 sectors, Bespoke also publishes a daily Sector Snapshot for subscribers. You can view a sample of our one-page Daily Sector Snapshot by clicking on the thumbnail image below.

Our Daily Sector Snapshot provides investors with an easy-to-read matrix of technical analysis, breadth and internal readings, and fundamental datapoints. It’s the perfect way to get an aerial snapshot of both current readings and the way they’ve been trending for each of the major sectors. This perspective also allows investors to see how sectors stack up versus each other as well as relative to themselves on a historical basis.

Go ahead and give this helpful report a look by clicking the image below. The various readings should be pretty self-explanatory, but if you’d like to read a more in-depth explanation, you can do so here. If you would like to start receiving our Daily Sector Snapshot in your inbox each morning, start a two-week free trial to our Bespoke Premium membership level.

Global Unemployment Rates Still Healthy

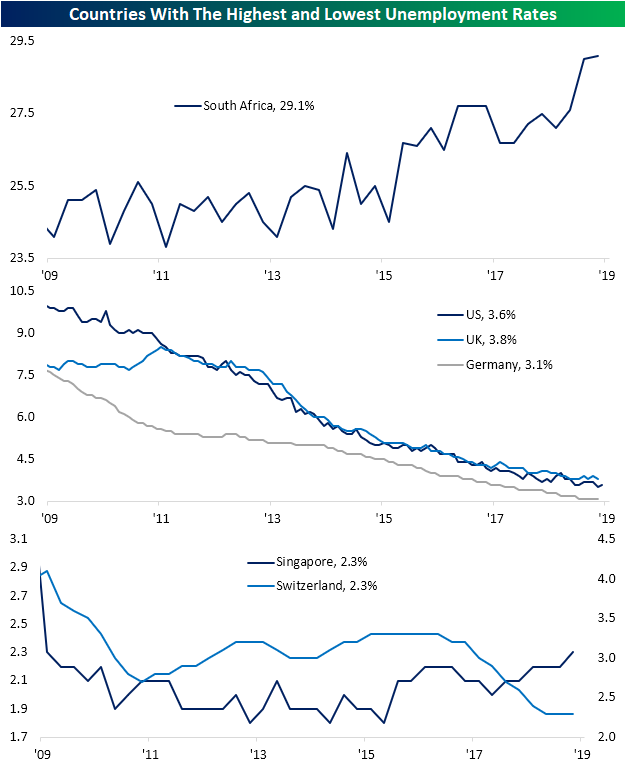

In spite of concerns of a slowing global economy, the unemployment rates of most major economies tracked in our Global Macro Dashboard around the world still appear to be at fairly healthy levels at the lower end of the past decade’s range. As shown in the table below, Canada, China, France, Germany, Japan, Russia, Spain, Switzerland, the UK, and the US are all within the lowest 5% of readings for unemployment of the past decade. While most other countries find themselves in more middling percentiles, only South Africa’s unemployment rate is at its highest level of the past decade at 29.1%; 7.6 percentage points above the decade’s low. Other than that, only Brazil, Italy, and Sweden are currently more than one percentage point above their 10-year low in unemployment.

Contrary to the rest of the world, the South African unemployment rate has been on the rise consistently over the past decade. But since 2015, unemployment has risen more rapidly bringing it to its currently elevated levels. On the other hand, the US, UK, Germany, and China are all near or at their lowest levels of the past ten years. While they are at their lowest levels relative to themselves, Singapore and Switzerland have the absolute lowest unemployment rates of the 23 countries tracked in our Global Macro Dashboard at 2.3%. What is interesting about these two countries is that while Switzerland’s reading is the lowest of the past decade as it sits in a downtrend, Singapore’s unemployment was much lower earlier in the decade given the rate has actually been in a slight uptrend over the past several years.

Overall, the global employment situation looks healthy with the average and median unemployment rates for the 23 Global Macro Dashboard countries near or at the lowest levels of the past decade. The only caveat to this otherwise healthy picture is that the rate of improvement has slowed lately. As shown in the second chart below, the year-over-year change for the average of these countries actually ticked into positive territory in the past month, rising 0.02 percentage points since one year ago. That is by no means an apocalyptic sign seeing as this occurred other times this cycle; the other times being in 2016 and from 2011 to 2013. On the other hand, the median—which would dampen effects from outlier readings from the likes of South Africa—is still showing YoY declines in the global unemployment rate. Start a two-week free trial to Bespoke Institutional to access our interactive Global Macro Dashboard, economic indicators monitor and database, and much more.

Fixed Income Weekly – 11/13/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we take a look at dividend yields for global equity indices relative to fixed income yields.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Record Closes Starting to Pile Up Again

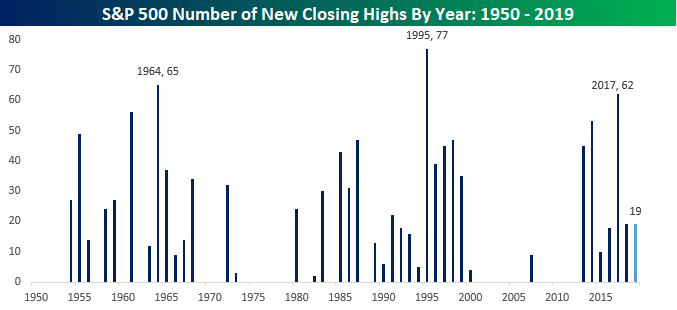

The S&P 500’s breakout to new highs in late October has kicked off a resumption in the count of record closing highs with half a dozen in just the last twelve trading days. With four record closing highs during the April failed breakout and then another nine in June and July, the total for 2019 now stands at 19, which is tied with 2018. A year ago today, the S&P 500 was close to 8% below its record high, so therefore the prospect for additional highs to close out the year was low, but this year is another story altogether. As of this writing, the S&P 500 is actually above its record closing high of 3,093.08, so not only are additional new highs likely over the next seven weeks, but we may even see one today.

The chart below shows the number of new highs for the S&P 500 by year going back to 1950. Over the 70 years shown, the greatest number of record closing highs for a given year was in 1995 when there were 77, while 1964 saw the second most with 65. In the current bull market, 2017 had the most record closing highs at 62. 2017 was also a year where the S&P 500 never saw a pullback of 3% or more, so therefore record highs were always within striking distance.

One interesting aspect of the chart is that there have basically been three distinct periods since 1950 where new highs for the S&P 500 were clustered together. The first was from 1954 through 1968 (there were also two years in 1972 and 1973 but there were four years between without any) and the second spanned a 21-year window from 1980 through 2000. The latest period began seven years ago in 2013, and while it may seem like the current 10-year market run has become long in the tooth, if it’s anything like the prior two periods, it could be another few years at least before occurrences of record new highs start to dry up. Sign up for Bespoke’s “2020” special and get our upcoming Bespoke Report 2020 Market Outlook and Investor Toolkit.

Bespoke’s Global Macro Dashboard — 11/13/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Bespoke’s Morning Lineup – 11/13/19 – Inflation Hotter Ahead of Powell

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.