Bespoke Stock Scores — 10/1/19

B.I.G. Tips – Worst Starts to October

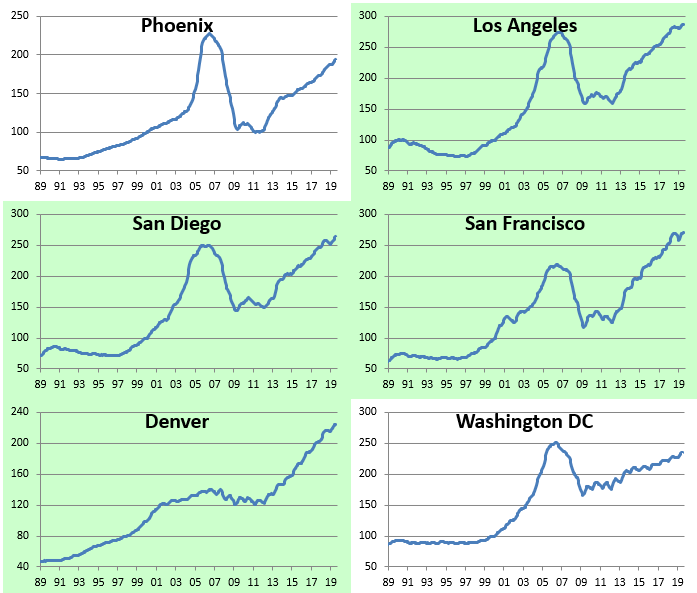

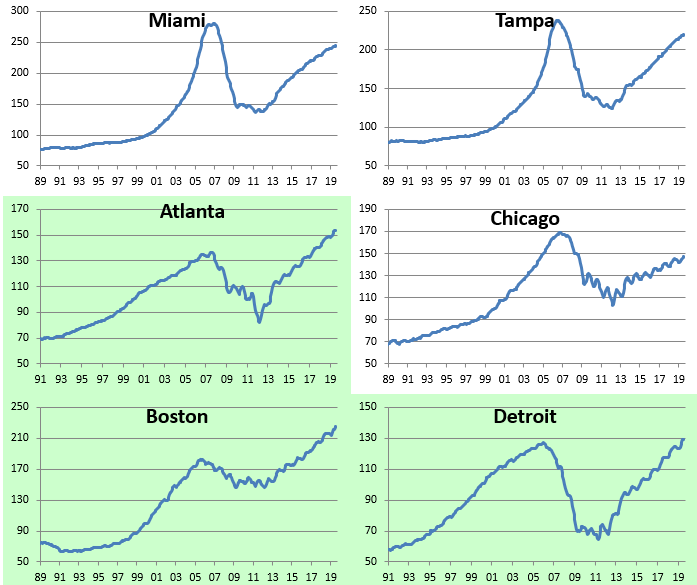

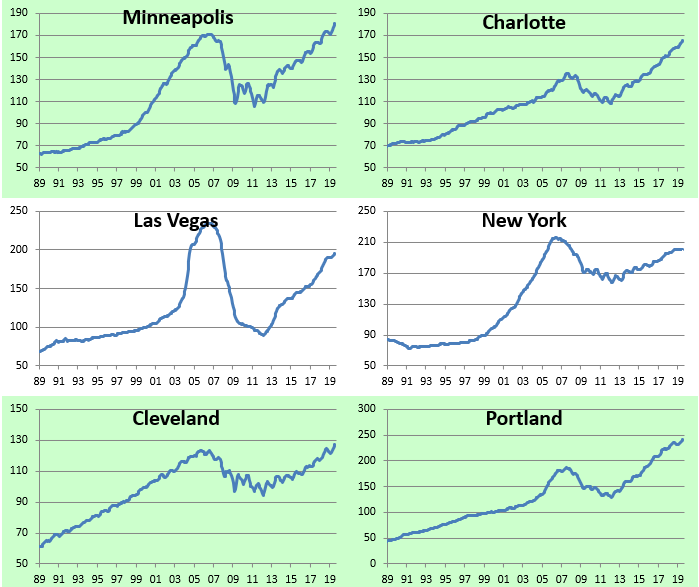

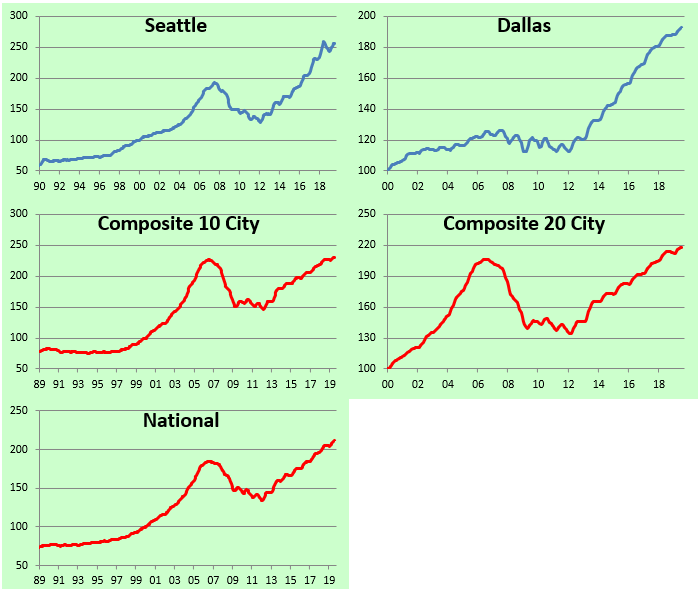

Updated Case Shiller Home Price Trends

Below is an updated look at recent home price changes for cities across the US based on the monthly S&P/Case-Shiller readings. As shown, a large majority of cities posted month-over-month gains in July, but it was the big three cities of New York, DC, and Los Angeles that saw home prices decline. Cleveland was the biggest MoM gainer at +1.11%, followed by Minneapolis, Phoenix, San Diego, Portland, and Las Vegas.

On a year-over-year basis, Seattle is the only city that posted a decline at -0.64%, while San Francisco was up just barely at +0.15%. These are two mega-cap Tech cities that saw prices boom over the last half dozen years, but they’ve cooled off recently as prices just got too absurd.

Below we show how much home prices are up or down versus their prior bubble highs seen in the mid-2000s. As shown, all of the composite indices are now at new highs, but there are still seven cities that have yet to get back their prior highs. These include Las Vegas, Phoenix, Miami, San Diego, Tampa, New York, and DC.

San Francisco, Las Vegas, and Detroit are now up 100% or more from their lows following the bursting of the housing bubble in the late 2000s. (Most lows were made in 2011 and 2012.) The composite indices are up roughly 60% from their lows, while home prices in New York are up just 27% since they bottomed out in 2012.

Below we show actual index price levels for the 20 cities tracked by S&P/Case-Shiller. This lets you see the long-term trend in home prices for each city. Cities highlighted in green are ones where home prices have taken out their prior highs during the current economic expansion. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

ISM Back to 2009 Levels

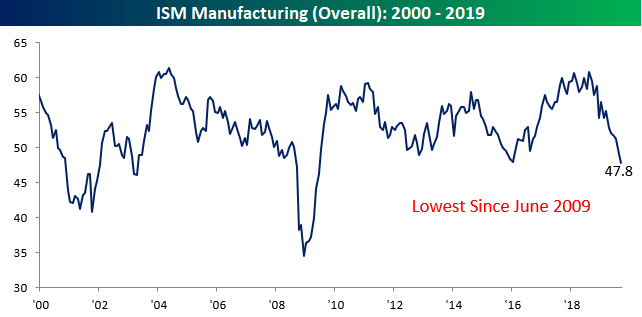

Talk about a disappointing start to the quarter. In the first economic report of the new quarter, ISM Manufacturing came in weaker than expected falling from 49.1 down to 47.8 compared to expectations for a reading of 50.0. While a miss of fewer than 1.5 points versus consensus expectations isn’t huge, investors treated it that way as the Dow has reversed more than 400 points from its earlier highs. What really spooked investors was the fact that the headline reading dropped to its lowest level since June 2009.

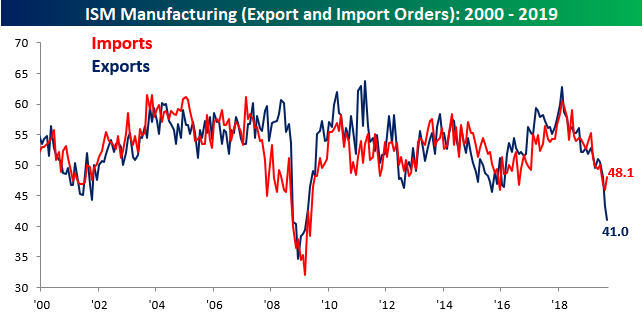

Breadth in this month’s report was also poor as six categories showed m/m declines while just four showed increases. On a year/year basis, things were even worse as Customer Inventories were the only category up versus this time last year. Some of the more notable decliners were Production (first chart below), which fell to its lowest level since April 2009, and Export Orders which is at its lowest level since March 2009.

In the case of Export and Import Orders, this month we saw a really wide disparity between the two. While Export Orders fell to its lowest level since March 2009, Imports actually increased. Normally these two indices move in unison with each other, but this month saw a wide divergence suggesting that the US economy is still on a better footing than international economies. In fact, the current spread between Exports and Imports hasn’t been this negative since September 2007. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

Dividend Stock Spotlight: Sonoco (SON)

One of the world’s largest packing product companies, Sonoco (SON)—not to be confused with major gas station brand Sunoco (SUN)—had a bit of a rough third quarter. Declining just over 10% in this time, the stock fell to the lower end of the past few years’ uptrend channel; taking out both the 50 and 200-DMAs in the process. Since mid-August, though, the stock has rounded out a bottom and has moved back above the 50-DMA. This also coincided with a support level that shares with the highs from around this time of year in 2018. In other words, while the shorter-term trend has been somewhat weak, the longer-term technicals have held up just fine.

SON’s dividend also helps its attractiveness. SON currently pays 2.94%, which is 50 bps more than the average for other Materials sector stocks in the S&P 1500. While somewhat high, the payout ratio is at 55.15%, meaning there is some security in the dividend by that metric. But that is not taking into account the fact that the company has been paying, and growing, its dividend consistently since the mid-80’s. Back in the spring, SON raised its quarterly dividend again from $0.41 per share to $0.43. That means for every 100 shares ($5,818), you’ll get $172 in dividend income per year from SON. That’s nearly twice the $96 you’d get per year from the same $ investment in the 10-Year Treasury.

Bespokecast Episode 31 — Alexandra Scaggs — Now Available on iTunes, GooglePlay, Stitcher and More

We’re happy to announce that the newest episode of Bespokecast is now available to the general public both here and via the various podcast platforms. Be sure to subscribe to Bespokecast on your preferred podcast app to gain access to our full collection of episodes. We’d also love for you to provide a review as well!

In this new episode of Bespokecast we sit down with Alexandra Scaggs of Barron’s. Alexandra joins us to discuss the plumbing of fixed income markets and the evolution of Federal Reserve policy. In recent weeks, the New York Fed has had to intervene in repo markets, driven by a sudden scarcity of liquidity that didn’t exist in recent years. We dive into why that scarcity has suddenly cropped up, why it matters for markets, and what the Fed can do about it in addition to recent steps it has already undertaken. Our guest previously wrote for Bloomberg and the Financial Times, and currently covers fixed income markets for Barron’s. You can follow her on Twitter here.

To listen to our newest episode or subscribe to the podcast via iTunes, GooglePlay, OvercastFM, or Stitcher, please click the button or links below. Please note that third-party podcast feeds may update at a lag of a few hours to this blog post.

Chart of the Day – The ISMassacre

US Equity Markets Enter Q4 in Neutral Territory

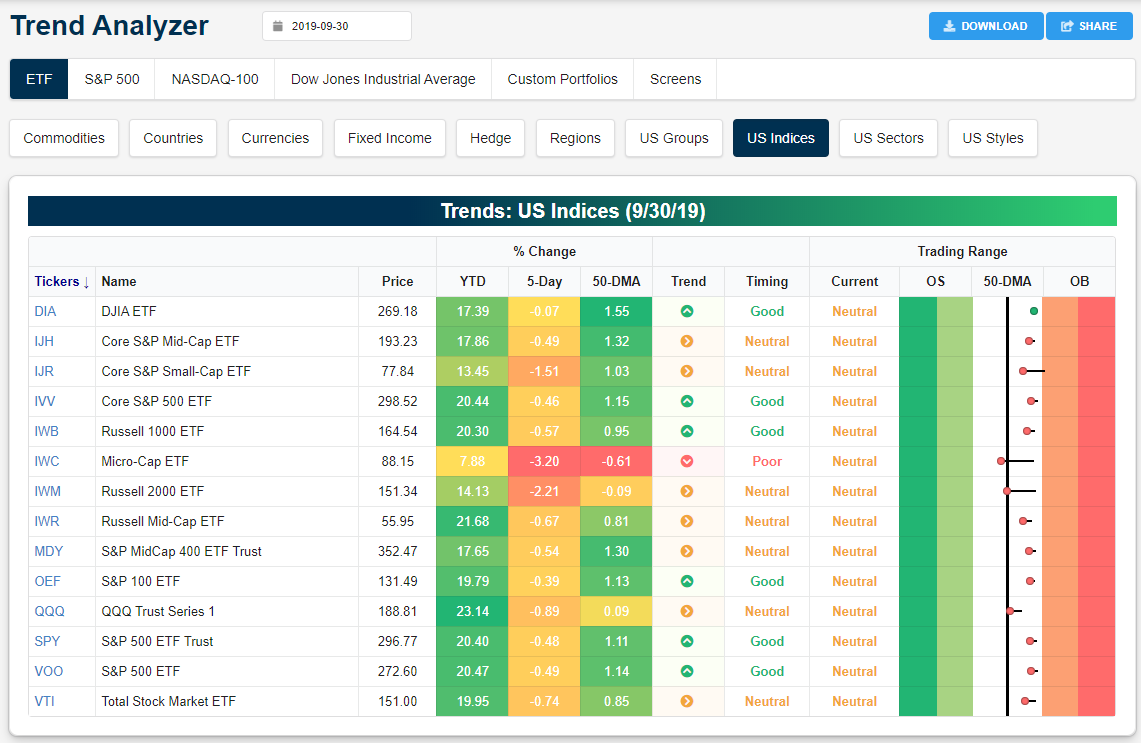

Below is a snapshot of US equity index ETFs from our Trend Analyzer tool. The Trend Analyzer helps investors easily see where a large number of stocks or ETFs are trading relative to their normal ranges. When looking at the “Trading Range” section, the black, vertical line represents each ETF’s 50-day moving average, and the dot represents where the ETF’s price is currently trading. The tail end of the dot shows where the ETF was trading one week ago, so if the dot is to the left of the tail, the ETF’s price moved lower within its trading range over the last week.

Over the last week, every major US equity index ETF moved lower within its range with the exception of the Dow 30 (DIA). The small-cap Russell 2,000 (IWM) and the Micro-Cap ETF (IWC) both moved back below their 50-day moving averages, while the Nasdaq 100 (QQQ) is the next closest to testing its 50-DMA. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

Looking at US sector ETFs, we saw Communication Services (XLC), Energy (XLE), and Health Care (XLV) break below their 50-day moving averages over the last week, while Consumer Staples (XLP) moved from neutral to overbought. Along with Utilities (XLU) and Real Estate (XLRE), the only sectors that are overbought right now are defensive in nature.

The Most Volatile Time of the Year

Welcome to October. The most volatile month of the year. While most investors and traders are well aware of the increased tendency for volatility in the month of October, the chart below provides an excellent illustration of that trend. In it, we show the average percentage spread between each month’s closing high and closing low going back to 1928. For all months since 1928, the S&P 500 has averaged an intra-month spread of 6.41%, but for the month of October, the average has been nearly two full percentage points wider at 8.25%! The next closest month in terms of intra-month volatility has been November with an average range of just 6.96%. While October is a big outlier in the data, volatility in the market is pretty seasonal. From July right through November, average intra-month volatility is above the historical average for all months, but from December through June, the average intra-month range has been below average. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

Bespoke’s Morning Lineup – 10/1/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

In case you didn’t see it last Friday, we just published our quarterly update of the “Pros and Cons” facing the equity market as we head into Q4. In it, we break down what we see as the biggest positive and negative issues facing the equity market. Make sure to check it out. For a brief summary, make sure to check out Monday’s CNBC segment on our outlook.

One interesting chart in today’s Morning Lineup is the chart of gold. Talk about losing its luster quickly! It wasn’t too long ago that gold was in massive rally mode on the way to new highs. After a lower high in September and now a bearish break of the 50-DMA, though, there looks to be quite a bit of space between now and the 200-DMA below.