Protests Pummel Hong Kong Data

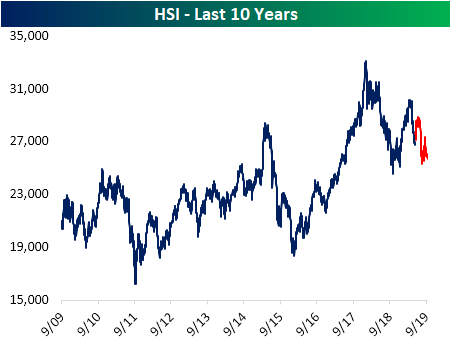

Through most of the second half of the year, a series of mass protests in opposition to Chinese extradition legislation has been consuming Hong Kong. While smaller-scale protests have been taking place since the early spring, things really began to ramp up in June when hundreds of thousands took to the streets. In the more than three months that have passed since then, some of the effects are beginning to be seen in the country’s economic data that we track in our Global Macro Dashboard. Markets were the quickest to respond as the country’s Hang Seng Index has fallen roughly 5% since the start of June. The HSI is now in a defined downtrend over the past couple of years and recently has been making its way towards support at last year’s lows.

Hong Kong retail sales have tanked since protests began. In the months leading up, retail sales had been contracting year-over-year for four consecutive months. The reading for May came in at -1.4%, but once protests took effect the following month, retail sales collapsed to a -6.7% growth rate. Conditions have only worsened from there as retail sales contracted 23% YoY in August. That is the worst contraction in the history of the data going back to 2006, surpassing the previous low of -20.6% in February 2016.

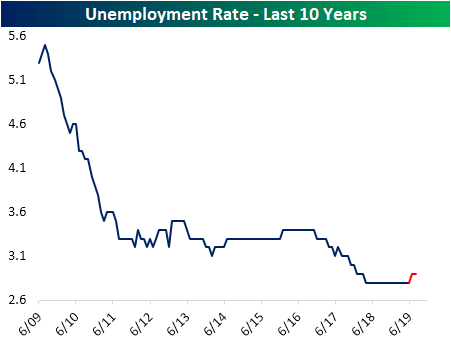

Likely as a result of people taking to the streets rather than showing up to work, the unemployment rate has begun to tick higher over the past few months. For the entire year before the protests began, Hong Kong’s unemployment rate held steady at 2.8%; the lowest level of the past decade. But the July release showed the rate has risen 0.1% to 2.9%. That was the first increase of any kind since the one month blip in July of 2017. Start a two-week free trial to Bespoke Institutional to access our Global Macro Dashboard as well as our Economic Indicators Database and much more.

Bespoke’s Global Macro Dashboard — 10/9/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Bespoke Morning Lineup – 10/9/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Chart of the Day: Northrop Grumman (NOC) Top Stock Score

S&P 500 Sector Technicals

The S&P 500’s rally to end last week proved to be a pump-fake, as the gains have already been washed away this week. As shown below, the S&P is still hanging onto an uptrend for the year, but its recent failure to make a new high above its July highs is a negative technical set-up.

Below are trading range charts of the ten major S&P 500 sectors (Real Estate is excluded). The red shading represents overbought territory while the green shading represents oversold territory. The white line is the sector’s 50-day moving average. Every cyclical sector is now below its 50-day moving average. Consumer Staples and Utilities are the only sectors above their 50-DMAs and the only sectors that managed to make new highs during the S&P’s early September rally.

While technicals don’t look especially positive, things haven’t broken down yet either. Most sectors are simply at or near the bottom of multi-month sideways ranges.

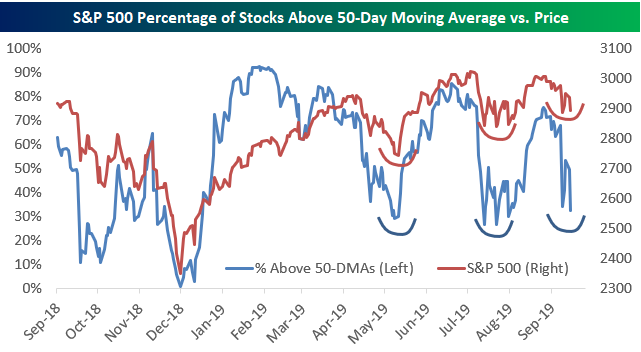

Some of the key breadth measures we track have gotten weaker and weaker with each rally recently. And while the S&P is still above lows it made in early June and again in August, the percentage of stocks now trading above their 50-day moving averages has moved back down to levels seen at those prior lows.

As shown below, 32% of S&P 500 stocks are now above their 50-DMAs, and Utilities and Real Estate are the only sectors with healthy readings of 86% and 69%, respectively. Defensives have been the place to be.

Technology has also started to weaken significantly. Only 27% of stocks in the sector are above their 50-DMAs, which is five percentage points below the reading for the S&P 500. Over the last few years, Tech has always been a market leader, but the sector’s internals are starting to show cracks that we don’t want to see.

There are four sectors with breadth readings in the teens. Communication Services, Health Care, Energy, and Financials all have 18% or less of their stocks above their 50-day moving averages.

A Seasonal Break?

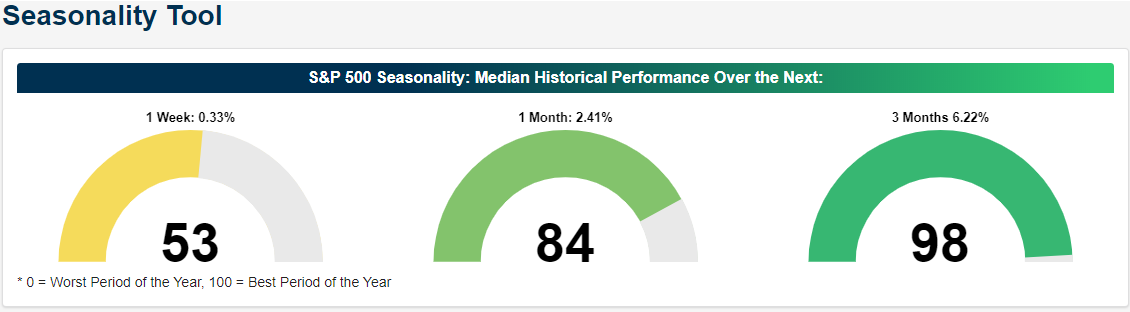

It has been a tough week and a half for bulls as equities have been under pressure since the start of October. While issues surrounding China don’t seem to be getting any better, seasonal trends may be starting to take a turn for the better. The gauges below are from our Seasonality Tool, which is part of the interactive section of our website. In it, we calculate the S&P 500’s historical median return in the one week, one month, and three months from the close on 10/8 over the prior ten years. While the S&P 500’s median one week return is a middling 0.33%, ranking in the 53rd percentile relative to all other one week periods throughout the year, the median one and three-month returns have been much more impressive at 2.41% and 6.22%, respectively.

In addition to the upcoming month being a good seasonal period for the equity market, there are a number of stocks that have traded higher during the one-month period in each of the last ten years. While it’s relatively common to see one or two stocks that have a perfect record of trading higher during a random one-month period of the year, nine is pretty high. Also, with names like Hormel (HRL), Analog Devices (ADI), and Starbucks (SBUX) on the list, they aren’t all companies that no one has ever heard of either!

Below we have listed how each of the stocks above look in our Trend Analyzer screen. On the left side of the table, we show each stock’s performance metrics over the last week and YTD as well as where each stock is trading relative to its 50-day moving average. In addition to the performance metrics, we also show whether the stock is in an up, down, or sideways trend using our proprietary algo, how the stock’s timing currently stacks up, whether the stock is oversold, overbought, or neutral, and then finally where it is trading relative to its trading range. Looking at the names on the list, SBUX looks the most attractive as the stock is at extreme oversold levels but also has a perfect timing score given its long-term uptrend. Meanwhile, Pier 1 (PIR), which is in a downtrend and coming off overbought levels, currently has a timing score that ranks as poor. Interested in tracking seasonal patterns of the market and individual stocks? Start a two-week free trial to Bespoke Institutional to access all of our research and our popular interactive features including our Stock Seasonality and Trend Analyzer tools.

The Closer – Trending Vol, Slow Volume, Small Business Growth, Balance Sheet – 10/8/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review the longer term trends of increasing volatility alongside lower volumes. We then look at Census data on the best and worst states for small business creation. Next, in the wake of Fed Chair Powell’s announcement today, we give some insight into the Fed’s balance sheet. We finish with a recap of today’s PPI data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Delta (DAL) and Other Air Lines Soar on Earnings

B.I.G. Tips – Next Stop – Earnings Season!

Investors are preoccupied with trade issues and impeachment headlines this week, but earnings season is coming up right around the corner. Whether the earnings headlines provide a welcome break from all the back and forth between the US and China or Republicans and Democrats remains to be seen, but at least it will be a change of pace.

Once again this month, the key trend to watch this earnings season will be how often the term ‘China’ or ‘tariffs’ comes up in quarterly conference calls. Just this morning, the NFIB reported in its Small Business Sentiment report that “Tariffs are adversely affecting many small firms, with 30% reporting negative effects in NFIB’s September survey.”

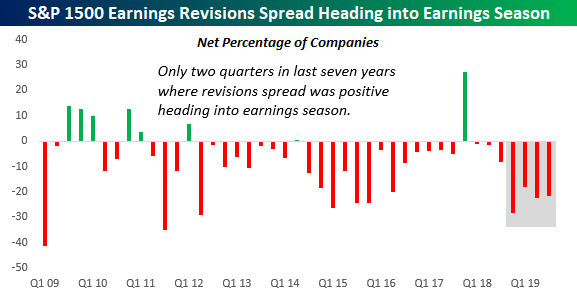

Based on the commentary, current trade policies are obviously making their presence felt. The only question is how much is priced in? Based on recent trends in analyst revisions, analysts have adjusted their forecasts by a decent amount. Over the last four weeks, analyst revisions have come in at a pace of two to one in favor of downside revisions. Analysts have raised EPS forecasts for just 312 companies in the S&P 1500 and lowered EPS forecasts for 634, which works out to a net of negative 322 or 21.5% of the stocks in the index. As shown in the chart below, this continues a trend that we have seen for four quarters now, where analysts have been consistently lowering forecasts in response to the impact of tariffs and other uncertainty related to trade.

We have just published our quarterly preview of the upcoming earnings season and what to expect in terms of the overall market and sector performance based on trends in analyst revisions. To gain access to the full report, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.