Chart of the Day: Recessionary Data From The Conference Board

Trend Analyzer – 3/26/19 – Only the Nasdaq (QQQ)

Declines over the past week have pushed all but one index ETF back to neutral from overbought territory. Currently, only the Nasdaq (QQQ) is overbought. QQQ has been a strong performer lately and while other indices have seen declines exceeding 3% over the last week, QQQ is only down 0.13% headed into today’s trading. It is also up the most YTD at 15.74%. On the other hand, the other index ETFs are all neutral with some having collapsed below the 50-DMA. There are now five ETFs below their 50-DMAs with the Core S&P Small Cap ETF (IJR) the furthest below. As IJR edges increasingly closer to oversold, it is now over 2% below its 50-DMA. Along with the Dow (DIA), it is also only seeing single digit returns YTD. While IJR has been exceptionally bad, the other small caps like the Micro Cap ETF (IWC) and Russell 2000 (IWM) have not been much better, as these three are now all down over 3.25%.

Bespoke CNBC Appearance (3/26)

Bespoke co-founder Paul Hickey sat down with Brian Sullivan earlier on Tuesday to discuss markets, the yield curve, and semiconductors. To view the segment, please click on the image below.

Morning Lineup – A Global Sigh of Relief

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Equity investors around the world are breathing a global sigh of relief this morning as most equity markets have at least partially rebounded from Friday and Monday’s weakness. There’s a healthy dose of economic data coming up 8:30 with Housing Starts and Building Permits and then Consumer Confidence at 10 AM. Keep an eye on semis today as yesterday, they underperformed the broader market by a pretty wide margin, and then last night Samsung issued a profit warning. Semis have been the market’s leadership group for some time now, so bulls don’t want to see that group falter.

Please click the link below to read today’s Bespoke Morning Lineup.

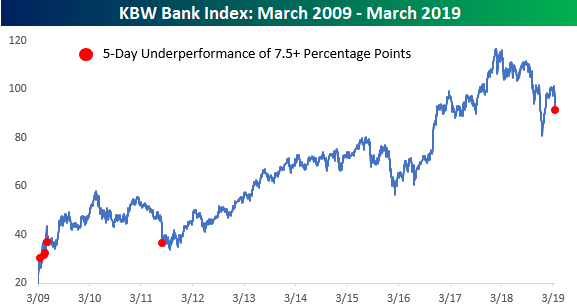

Things are looking up a bit today, but the last five trading days have been hell for bank stocks. After the KBW Bank Index briefly peaked above its 200-DMA last week for the first time since late September, it has been nothing but declines for the group ever since. During the last five trading days, the KBW Bank Index has seen daily declines of 1.32%, 3.02%, 1.53%, 3.92%, and 0.42%. In total, those declines work out to a five-day decline of just under 10% (9.83%) compared to a drop of just 1.22% for the S&P 500.

With bank stocks underperforming by more than 8 percentage points during this stretch, it goes down as the worst relative performance for the group since August 2011. Since the lows of the Financial Crisis, there have only been five other five day periods that saw similar underperformance, and all but the 2011 period occurred during the very early stages of the rally. You don’t see relative underperformance like this in the bank stocks very often.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Relative Underperformance, Yield Curve Diverges, Global Weakness — 3/25/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, in spite of equities’ strong performance so far this year, we highlight the asset’s underperformance relative to commodities and fixed income. Staying on the topic of fixed income, we take a look at the divergence between the long end and the front end of the yield curve, and what kinds of recessionary signals it is sending. Further, we provide an update on the market’s expectations for rate hikes and cuts based on the OIS market. Turning to macro data, we show another weak month of CPB data on global trade and industrial production, though it’s not all bad, as Germany trade and auto industry data is at least supportive.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Bottom-Fishing With Biogen (BIIB)

This Week’s Economic Indicators – 3/25/19

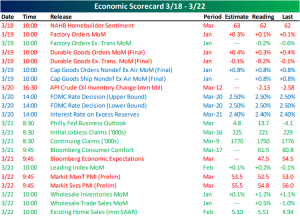

Last week saw 23 releases with pretty much an even split between beats and misses. Homebuilder sentiment was the only release on Monday; coming in unchanged from the prior month but also missing forecasts. Manufacturing data on Tuesday came in somewhat mixed. While Durable goods were weaker, Capital goods were unchanged. As expected, the FOMC did not change rates but their more dovish tone on Wednesday was a major shift. The Philly Fed came in very strong on Thursday thanks to strong shipments, although more forward-looking internals were weaker. To round out the week, much like other global Flash PMIs, the US releases for both service and manufacturing PMIs were weaker than expected.

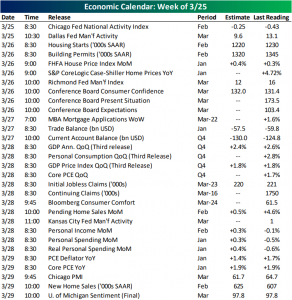

Things are slightly busier this week with 30 releases. The Chicago Fed’s National Activity Index kicked off the week this morning coming in at -0.29 versus expectations of -0.38. The Dallas Fed’s Manufacturing Activity Index was also just released showing some weakness coming in at 8.3. The Richmond Fed and Kansas City Fed counterparts will be released later in the week. In addition to several manufacturing releases, this week will have a heavy slate of housing data with FHFA and Case-Shiller Home Prices on Tuesday alongside Housing Starts and Building Permits. Pending and New Home Sales will also be released later in the week. Thursday we will get the third and final release of Q4 GDP figures which are expected to come in slightly lower.

B.I.G. Tips – Apple Product Announcements

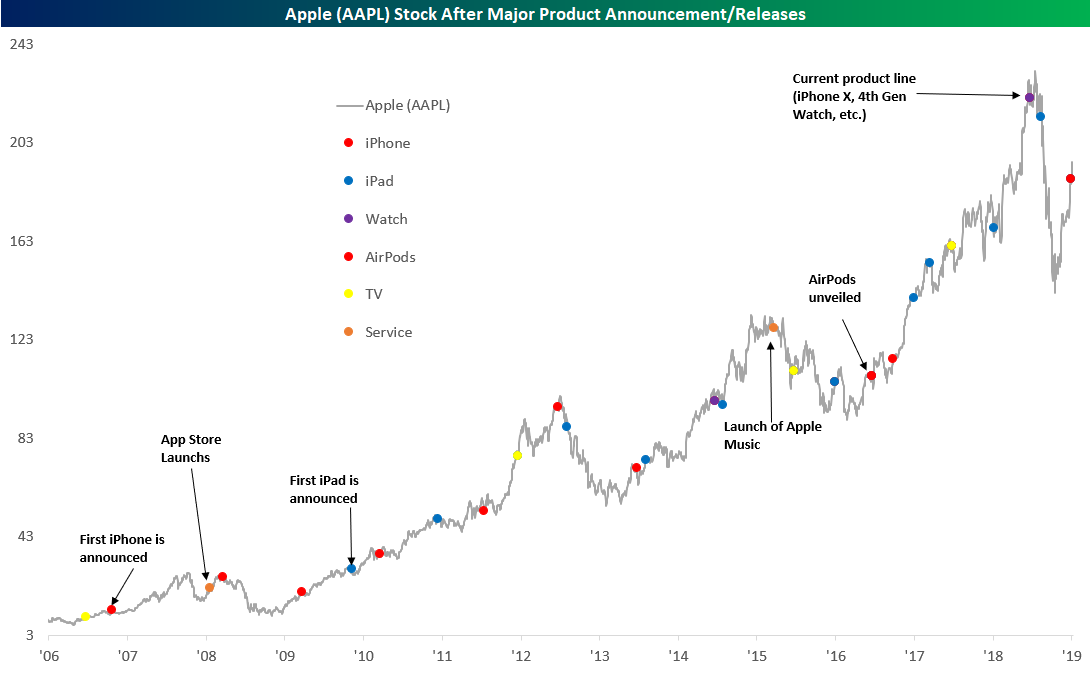

Apple (AAPL) will hold an event today at 1PM Eastern where the company is expected to make some big announcements. In addition to updated versions of existing products like their iMacs, iPads, and AirPods, Apple is expected to announce the launch of its own Netflix-like streaming service. That will also not be the only subscription service that the company is rumored to be revealing. It has also been circulated that AAPL plans to unveil a new subscription news service, taking advantage of their already popular news app. In our latest B.I.G. Tips report, we provide a summary of how AAPL stock has performed leading up to and after major product/services announcements over the years, and below we provide an annotated chart of AAPL over the years with color-coded circles to highlight announcements/releases of various products in its stable. To gain access to the full report, please start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Morning Lineup – Moving On

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium. Below is an excerpt:

The weekend’s release of the Mueller Report did not have the kind of fireworks that some were looking for but that markets can’t stand. From a political perspective, we’re probably far from the end of hearing about Russia, the elections, and any obstruction, but based on the market’s complete lack of any reaction this morning, it has already moved on.

Markets will also be trying to move on from Friday’s sharp declines after the yield curve (10y/3m) inverted for the first time in over a decade, and with the curve back in positive territory this morning, that should help stabilize things for now. Don’t forget, though, that there are just six days left in the quarter, and shortly after that Q1 earnings season kicks off, so that should be, at a very minimum, an interesting period for equities.

Following in the heels of Friday’s sharp declines, Asian equities were hit hard overnight. For China, that meant that its streak of 1% gains to kick off the week ended at six. That was still enough to be the longest such streak of 1%+ gains in over a decade.

From a technical perspective, China’s rally is still intact. While the Shanghai Composite has been consolidating gains over the last two to three weeks, the short-term uptrend that has been in place since it broke out in late February remains intact.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 3/24/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Taxes

Why Americans Don’t Cheat on Their Taxes by Rene Chun (The Atlantic)

High morale and faith they are paying their fair share are key reasons that the US has been able to maintain a high rate of voluntary compliance with taxes. [Link]

Real Estate

All Signs Point to a Housing Boom Ahead by Conor Sen (Bloomberg)

Contrary to dour outlooks for housing that have become prevalent in recent analysis as data cooled in the latter half of last year, there are some major tailwinds in place for the space. [Link; soft paywall]

A Growing Problem in Real Estate: Too Many Too Big Houses by Candace Taylor (WSJ)

After large, high-maintenance palaces in remote (albeit attractive) locations, Baby Boomers are having a hard time finding bids of properties that don’t fit the income, lifestyle, and preferences of younger buyers. [Link; paywall]

The lawyers who took on Big Tobacco are aiming at Realtors and their 6% fee by Andrea Riquier (MarketWatch)

A class action suit filed in Chicago alleges that the realtor system is a monopoly that is not legal under federal antitrust law. [Link]

Popped Bubbles

Behind the curtain at China Ding Yi Feng by Jamie Powell (FTAV)

A Chinese conglomerate suspended from trading earlier this week had some…interesting ideas about how the world – especially related to finance and investing – works. [Link; registration required]

Bitcoin Is in the Dumps, Spreading Gloom Over Crypto World by Paul Vigna (WSJ)

Since bitcoin’s 2017 blow-off top, trading volumes have collapsed, miners are facing a desperate cash crunch, and the ecosystem premised on ever-expanding prices for the underlying cryptocurrency is falling apart. [Link; paywall]

Food

The People Who Eat the Same Meal Every Day by Joe Pinsker (The Atlantic)

As many as one-third of Brits eat the same lunch every day, and the ranks of the monotonous menu brigade are large elsewhere as well. [Link]

Chicken nugget demand is flatlining — here’s what happened by Marilyn Haigh (CNBC)

The historic bedrock of kids’ menus across the nation is falling on tough times as chicken strips and health concerns keep them off consumers’ plates. [Link]

Boeing

Capt. Sullenberger on the FAA and Boeing: ‘Our credibility as leaders in aviation is being damaged’ by Captain Sully Sullenberger (MarketWatch)

After a catastrophic series of accidents related to software on its 737 MAX airframe, Boeing and its regulator have some tough questions to answer; the entire US aviation industry may be in trouble as a result. [Link]

Hedge Funds

At Hedge Fund That Owns Trump Secrets, Clashes and Odd Math by Katherine Burton, Sridhar Natarajan, and Shahien Nasiripour (Bloomberg)

A hedge fund that owns the National Enquirer has a reputation as a litigious, boundary-pushing organization in its pursuit of returns. [Link; soft paywall, auto-playing video]

Buy Gold!

Buy Gold, Sell Stocks Is the ‘Trade of Century’ Says One Hedge Fund by Sarah Ponczek (Bloomberg)

Small macro hedge fund Crescat Capital thinks precious metals are the play while equity markets are poised to tumble. [Link; soft paywall, auto-playing video]

De-Cycling

As Costs Skyrocket, More U.S. Cities Stop Recycling by Michael Corkery (WSJ)

After China decided to stop buying US recycling materials (citing too much trash mixed in), costs have surged for municipalities that offer curbside pickup. [Link; soft paywall]

This Week In Tech

Most Amazon Brands Are Duds, Not Disrupters, Study Finds by Spencer Soper (Bloomberg)

While there’s lots of speculation that Amazon could use its market power to monopolize activity within its e-commerce platform, one study shows that Amazon-branded products don’t actually perform that well with consumers. [Link; soft paywall, auto-playing video]

The Hottest Chat App for Teens Is … Google Docs by Taylor Lorenz (The Atlantic)

With laptops proliferating and Google Docs often used as a tool for collaboration or doing work on a given subject, students are starting to use the tools as a way to talk where the teacher can’t hear. [Link]

A first look at Twitter’s new prototype app, twttr by Sarah Perez (TechCrunch)

In an effort to improve engagement, Twitter is experimenting with an alternate mobile app; here are the early results of the effort. [Link]

Class

On Class Difference by Chris Dillow (Stumbling and Mumbling)

A discussion about how natural comfort in elite institutions – thanks to the income, social status, or culture a person is used to being in – can confer both benefits and create horrific blind spots. [Link]

Espionage

A shadowy group trying to overthrow Kim Jong Un allegedly raided a North Korean embassy in broad daylight by John Hudson (WaPo)

Ahead of a meeting between North Korea’s leader Kim Jong Un and President Trump, an expat dissident group ransacked the North Korean embassy in Madrid. [Link; soft paywall]

Labor Markets

Shake Shack Tests Four-Day Work Week Amid Tight U.S. Job Market by Matthew Boesler and Jeanna Smialek (Bloomberg)

Efforts to introduce a four-day work week in the US have been resisted for decades, but one fast food company is trying to do it in response to tight labor markets. [Link; soft paywall, auto-playing video]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!