The Bespoke Report – 2/26/21 – Poker Time For Bonds & The Fed

Stocks closed out the week in a full-throated test of uptrends after a week of historic volatility in interest rate markets. We discuss in detail the scale, nature, and implications of the move in interest rates, as well as some of the knock-on effects for equity markets. The rotation out of momentum and in to value has continued, with some of the most impressive gainers of recent years under harsh pressure in recent weeks. That’s going to cause a shake-up in terms of what stocks are included in momentum indices which are currently underperforming. We also take a deep dive into renewables, discussing some of the major stocks in the sector and their recent declines.

We also recap earnings results, discuss economic data here and abroad, make the case that the recent bond market move is a test for the FOMC, and more in this week’s Bespoke Report.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

February: In With a Bang, Out With a Whimper

The month of February has been a tale of two markets for global investors with the first half of the month seeing nothing but gains and the second half seeing pretty much nothing but declines. The Bloomberg World index of more than 4,000 global companies was up eleven days in a row to start the month for a gain of more than 6%! Since February 15th, though, the index has fallen on eight of nine trading days for a decline of more than 4%. As it stands now, the index is still up 1.9% for the month, but the second-half declines have now left the index below its 50-day moving average for the first time since Election Day 2020 (11/3). Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 2/26/21 – Uneasy Markets

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“We will ensure that there is no unwarranted tightening of financing conditions,” – Isabel Schnabel, ECB Board Member

Well, that didn’t take long. Just days into a market growing uneasy with the rise in government bond yields and Christine Lagarde noted that the ECB is ‘closely monitoring’ the situation in fixed income markets, Isabel Schnabel, a prominent member of the ECB tried to reassure markets that the ECB “will ensure that there is no unwarranted tightening on financing conditions”. She went on to add that the central bank would add further support to the markets if rising yields threaten to hurt growth. On both sides of the Atlantic, central bankers are doing their best to reassure markets that they will keep rates low, but for now, at least, the market isn’t so confident.

Futures have been volatile this morning and depending on when you look they may be up or down, and they are currently on the downside for both the S&P 500 and the Nasdaq. The economic calendar is busy with Wholesale Inventories, Personal Income, and Personal Spending at 8:30 AM. At 9:45, we’ll get the release of the February Chicago PMI, and then at 10:00, we’ll close out the week with the University of Michigan Sentiment Index.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports from around the world, ARK Invest fund flows, economic data out of Europe, an update on the latest national and international COVID trends, including a new series of charts tracking vaccinations, and much more.

Also, Paul Hickey appeared on CNBC’s Squawk Box this morning to discuss the current moves in interest rates and what they mean for the market. You can see that segment here.

Thursday was a day many bulls would rather forget as the S&P 500 dropped over 2%, and the Nasdaq 100 fell more than 3%. Historically, declines of these magnitudes usually see a modest bounceback the following day, but believe it or not, the distribution of returns based on the day of the market decline varies widely. The charts below show the S&P 500’s and Nasdaq 100’s average next-day return (top charts) and the percentage of time each index is up (bottom charts) following days when they experience sharp declines.

When the S&P 500 declines more than 2% on a Thursday, the average next-day return is just 0.02% with positive returns 50.6% of the time. Of all the days of the week, that is the second weakest next day return and the second-lowest percentage of positive returns.

For the Nasdaq 100, it’s a similar setup. When that index declines more than 3% on Thursdays, the average next-day return is a gain of 0.05% with positive returns just 47.3% of the time. More than any other day of the week, when the Nasdaq 100 drops 3% on a Thursday, the likelihood of a down Friday is the highest.

Chart of the Day: S&P 500 Dividend Yield vs. 10-Year Treasury Yield

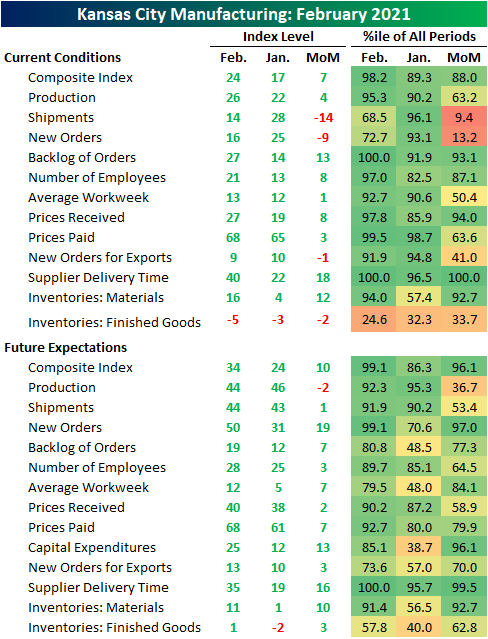

Kansas City Fed Goes Out With A Bang

The last of the regional Fed manufacturing reports for the month of February went out with a bang. The Kansas City Fed’s composite manufacturing index rose from 17 to 24 in February, exceeding expectations by 9 points. That brought the index to the highest level since June 2018 and is also in the top 2% of all monthly reading since the survey began in 2001. Expectations also remain historically optimistic with that index in the top 1% of all months, also rising to the highest level since June of 2018.

Not only was the headline index strong but most of the components of the report similarly came in at historically strong levels. Both Backlog of Orders and Supplier Delivery Times came in at record highs while all but three other indices are in the top decline of all prior readings. Most indices were higher month over month, though, there were a few components that fell like Shipments, New Orders, New Orders for Exports, and Inventories for Finished Goods.

Two of the weaker components of the report were the indices for New Orders and Shipments. While still at healthy levels, the declines this month meant that new orders and shipments both decelerated in February. But even though the indices for current conditions fell, expectations indices were much stronger. As shown below, both expectations indices for New Orders and Shipments were higher month over month with the former coming in the top 1% of all months. Although the reading in New Orders pointed to some slowing, Backlog of Orders accelerated rising to 27, the highest level on record.

The other index reaching a record high was Delivery Times. Higher readings in this index indicate longer lead times. The 18 point increase month over month in February left the prior record of 30 from March 2018 in the dust. Manufacturers also do not appear to have high hopes that supply chains will normalize in the near future either. The expectations index likewise came in at a record high of 35.

Alongside longer lead times, prices are on the rise as has been observed in other manufacturing reports. The indices for both Prices Paid and Prices Received were higher this month. Starting with Prices Paid, the current conditions index rose to the second-highest reading on record behind April 2011. Expectations were also at the highest level since April 2011. Consistent with other manufacturing surveys from the other regional Feds, Prices Received are more muted but are nonetheless at the highest level in some time. Rising to 27 this month, the index for Prices Received rose to the highest level since August 2008. Click here to view Bespoke’s premium membership options for our best research available.

Bulls Stay in Charge

The major indices have been a bit mixed in the past week, and in turn, bullish sentiment took a small turn lower. 45.9% of investors responding to the AAII weekly sentiment survey reported as bullish this week. That’s down from 47.1% last week but still fairly elevated in the top decile of the past five years’ readings.

Although bullish sentiment took a small turn lower, bearish sentiment also has kept grinding lower. Less than a quarter of respondents (23.8) reported as bearish this week which was down from 25.4% the previous week. That is the lowest level since the week of December 24th when just under 22% of respondents reported as bearish. In the four weeks since recent the bearish sentiment high of 38.3%, the reading has fallen 14.5 percentage points. That makes for the biggest four-week decline since November 2019 when bearish sentiment fell over 20 percentage points from 43.96% to 23.93%.

While both bullish and bearish sentiment were lower, the decline in bearish sentiment was larger meaning the bull-bear spread continued to move higher. The spread rose from 21.7 up to 22.1 which is the highest level since the first week of December. That is also the fourth week in a row that the spread has moved in favor of bulls.

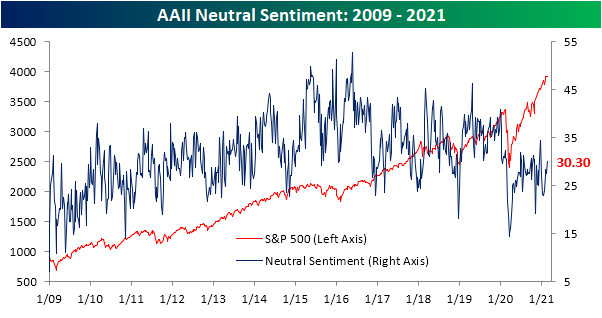

The losses to both bulls and bears meant more investors reported neutral sentiment. This reading tipped back above 30% for the first time in seven weeks. Click here to view Bespoke’s premium membership options for our best research available.

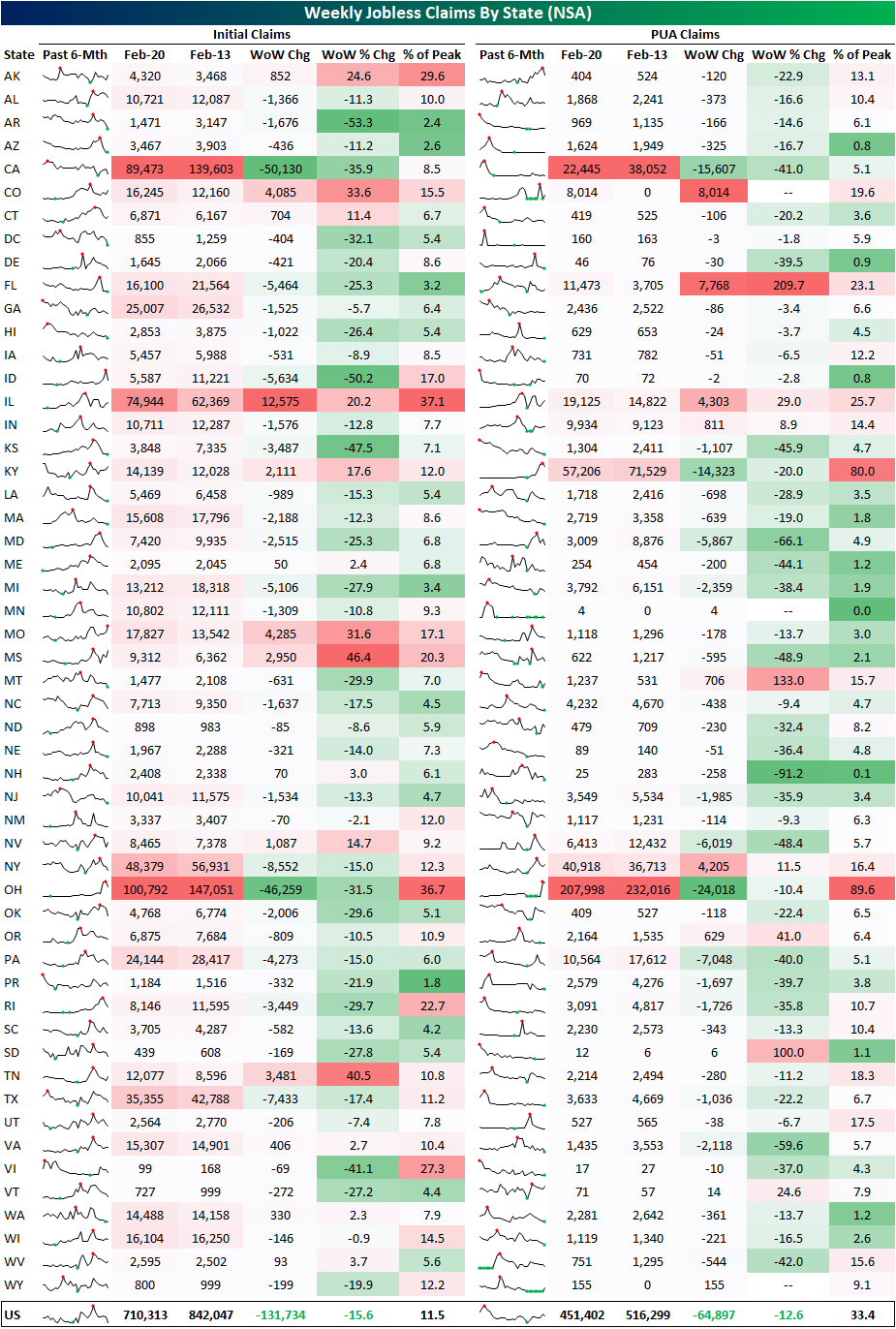

Was It The Weather?

While the weather may have artificially depressed the actual levels, today’s release of initial jobless claims came in at the lowest level since the last week of November. Seasonally adjusted claims totaled 730K, down 111K from last week’s revised reading of 841K (from the original 861K). While claims were expected to decline, this week’s release exceeded expectations by 95K.

On an unadjusted basis, claims also experienced a significant decline dropping by 131.7K. That was the largest weekly decline since mid-January when they fell by 176.7K. At 710.3K, this week’s print was the lowest level of jobless claims since last March. We would also note that the current week of the year has historically seen claims decline. The current week of the year (eighth) has only seen unadjusted claims rise week over week 13% of the time of all years since the data begins in 1967.

Pandemic Unemployment Assistance (PUA) also saw lower claims this week dropping from a multi-month high of 512.86K last week back down to 451.4K. Excluding last week, that is still one of the highest levels since early December. Despite this, the coincident drop in regular state claims meant the total between the two dropped to 1.162 million which is the lowest since the last week of 2020.

As we noted earlier, adverse weather in states like Texas was one factor that may have caused distortions in this week’s reading. While that could be a factor, we would note that other states were far larger contributors to the decline in aggregate claims. In the table below, we show the readings in regular state and PUA claims for every state for the current and past week as well as six-month charts. The states that saw the largest declines this week for regular state claims were California and Ohio with 50K and 46K declines, respectively. These two states also accounted for the largest shares of PUA claims. The next largest decline in regular state claims was an 8.5K drop in New York and then Texas’ 7.4K decline. While that was the largest decline for Texas since November, the big drop from Ohio was more of a factor. Accounting for over a third of the net decline in total aggregate decline this week, Ohio’s level of claims has skyrocketed recently with the additional qualm that the state has been flagging a high number of fraudulent claims. In other words, while some headlines have pointed to weather in the South affecting the lower claims counts, there are other potentially more impactful factors at play.

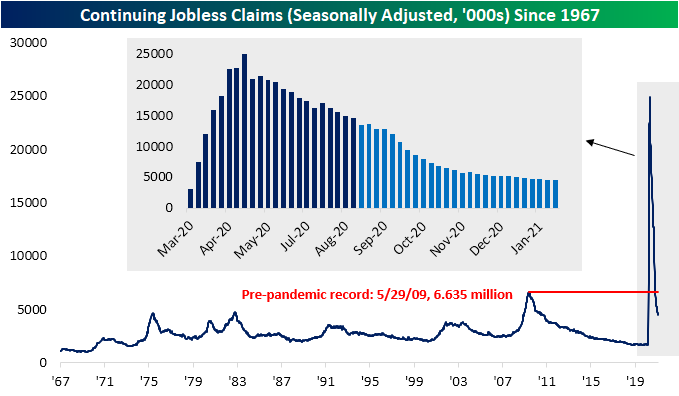

Turning over to continuing claims, the declines keep coming with claims for the week ending February 12th falling to 4.419 million. That is the sixth consecutive decline, and once again the lowest level of the pandemic.

Adding in other programs creates an additional week’s lag meaning the most recent data is for the first week of February. Total claims continued to trend a bit higher moving back above 19 million almost solely due to an over 1 million uptick in Pandemic Emergency Unemployment Compensation (PEUC). Due to that increase, the program accounted for a new high of more than a quarter of total continuing claims for the week of February 2nd. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 2/25/21 – Good Economic Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“All intelligent investing is value investing. Acquiring more that you are paying for. You must value the business in order to value the stock.” – Charlie Munger

The setup this morning is looking a lot like yesterday. Treasury yields are sharply higher, futures are lower, and bitcoin is above $50K. Yesterday, all those pre-market trends reversed themselves as Treasury yields gave up much of their gains, equities surged, and bitcoin pulled back. Will we see a repeat today?.

If lower treasury yields are what you’re looking for, this morning’s economic data isn’t likely to help much. Durable Goods Orders not only came in much better than expected (3.4% vs 1.1%), but December’s report was also revised higher from 0.5% up to 1.2%. Jobless claims came in 95K below estimates, although weather issues may have distorted that number. Lastly, the second look at Q4 GDP came in slightly lower than forecasts at 4.1% compared to estimates for growth of 4.2%.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports from around the world, sentiment data out of Europe, an update on the latest national and international COVID trends, and much more.

It’s been a tale of two markets for the major US equity indices over the last week. The Nasdaq 100 and S&P 500, both of which are loaded with mega-caps, have dropped more than 1% over the last five trading days, but smaller-cap focused indices have surged more than 2%, while the less tech-centric Dow Jones is up over 1% also. Most of the index ETFs shown have declined relative to their trading ranges in the last week, and all but one of them are still at least at overbought levels. The one index ETF that isn’t overbought heading into today is QQQ, and given its recent pullback, its timing score now ranks as ‘Good’.

The reason for QQQ’s ‘Good’ timing score is the fact that on Tuesday the Nasdaq 100 looks to have successfully tested its 50-day moving average and saw a decent follow-through on Wednesday. This morning, tech is under pressure again, so watch the $319 level to see if QQQ can continue to hold the line.

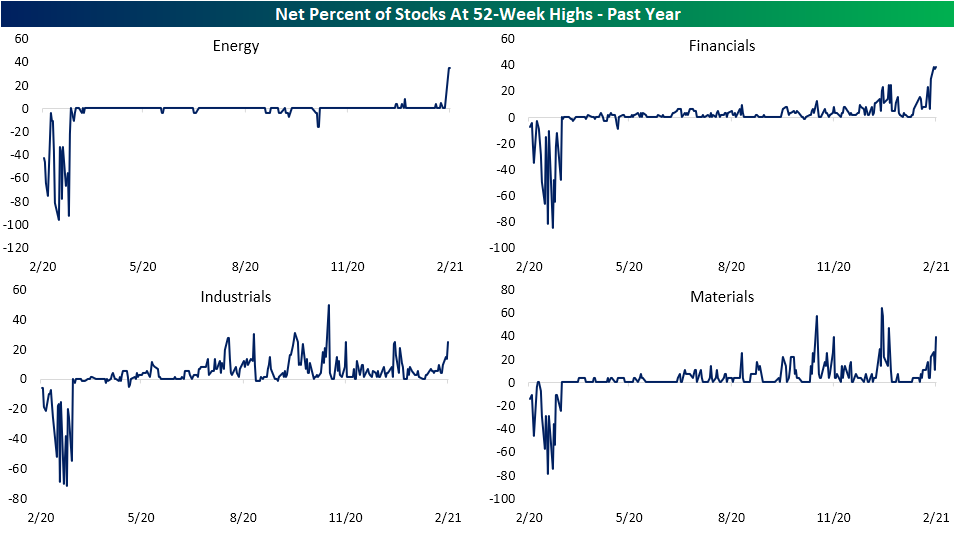

New Highs Picking Back Up Thanks to Cyclicals

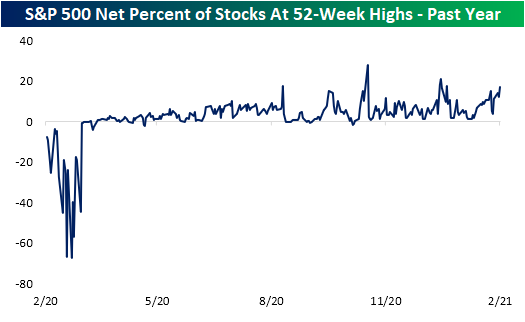

As equities bounce back today, a number of stocks are back up to 52-week highs intraday. As shown in the chart below, the reading on net new highs (percentage of stocks reaching new 52-week highs today minus the percentage reaching new 52-lows) for the S&P 500 is up to 16.8% which is on pace to be the highest level since January 12th. Over the past year, including today there have only been six days that the S&P 500 saw a stronger reading in net new highs.

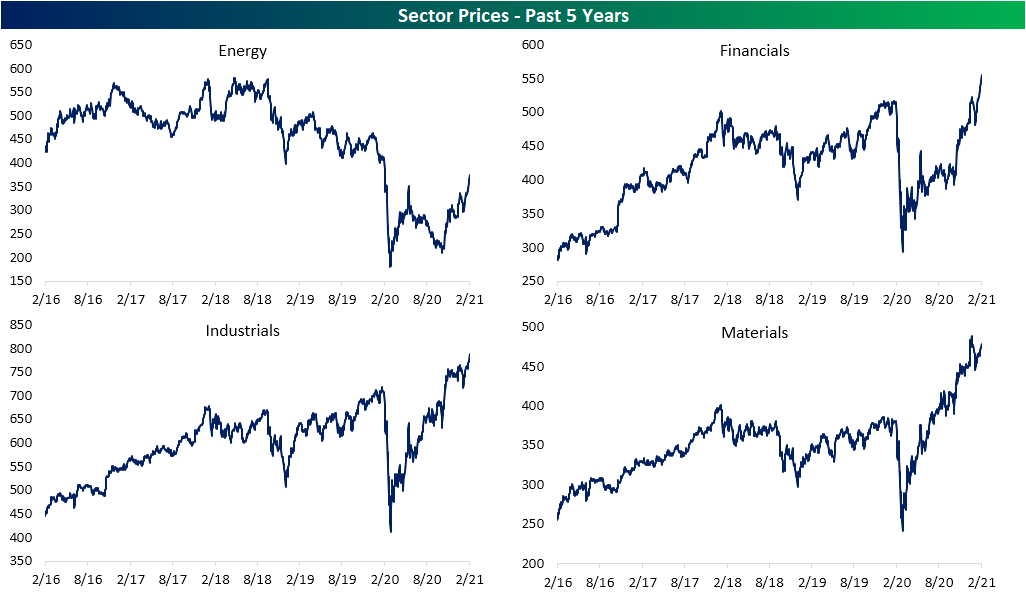

Looking across each of the eleven sectors, traditionally cyclical ones have stood out. Sectors that have been the best performers in the past week like Energy, Financials, Industrials, and Materials are also leading in new highs. The most impressive reading of these has been Energy. Over 34% of its stocks reached 52-week highs today which is the strongest reading since 5/17/18. While that is partially a result of big gains in these stocks recently, the higher number of new 52-week highs also has to do with higher prices of these stocks from prior to the COVID crash finally falling further into the rearview. For instance, as shown in the second set of charts below, even after its huge gains since the lows just over a year ago, the Energy sector still sits well below levels from prior to 2020. As for the other sectors, they not only have strong readings in net 52-week highs but also are making new highs in terms of price. Next to Energy, the reading for the Financials sector is the most notable at 38.46%; the highest since December 2019. While not at multi-year highs, Industrials and Materials have also seen some of the strongest readings in the number of new highs of the past year. AT 39.29%, Materials has the strongest reading of all sectors. Click here to view Bespoke’s premium membership options for our best research available.