Bespoke Brunch Reads: 11/6/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Labor Markets

CEO Patrick Collison’s email to Stripe employees by Patrick Collison (Stripe)

Amidst a blizzard of tech layoffs, payments company Stripe unveils a remarkably worker-friendly list of transition policies for fired workers that total about 14% of the labor force. [Link]

A Labor Supply Shock? by Preston Mui (Employ America)

Younger cohorts have almost entirely returned to pre-COVID levels of employment, leaving only the oldest segment of the labor market entirely responsible for the alleged lack of labor supply this year. [Link]

Liminal Spaces

Why One Chinatown Mini-mall Languishes While Another Thrives by Wilfred Chan (Curbed)

Detailed reporting on the magic of cheap rent in Chinatown and the downward spiral of the neighborhood over the past few decades. [Link]

The Eerie Comfort of Liminal Spaces by Jake Pitre (MSN/The Atlantic)

An investigation into why so many people are so enthusiastic for the “strange solace of being on the threshold of monumental change” in picture form. [Link]

Sports

Why is participation in girls’ high school sports — yes, even basketball — waning? by Langston Wertz Jr (Charlotte Observer)

High school sports participation is down sharply, with participation in basketball down 14% over the past decade, to the point that many schools are fielding only a varsity team with no JV squad and no cuts. [Link; soft paywall]

Professional Cornhole Has a Cheating Scandal Called BagGate by John Clarke (WSJ)

The formerly casual pastime has attracted sponsorship dollars and lots of attention, to the point where teams in the national finals were both caught cheating. [Link; paywall]

Traffic James

The Metals for Your EV Are Stuck in a 30-Mile Traffic Jam by Matthew Hill (Bloomberg)

Central African copper mines are tied to the rest of the world with tenuous and often-broken logistics lines that stretch across the southern half of the continent. [Link; soft paywall]

Why Egypt became one of the biggest chokepoints for Internet cables by Matt Burgess (Ars Technica)

Subsea internet cables are critical links for global connectivity with enormous volumes of traffic passing through physical chokepoints like the narrow land route between the Red Sea and Mediterranean. [Link]

China

China’s Local Governments Should Put State Assets to Better Use, Ministry Says by Chen Yikan (Yi Cai Global)

Beijing is starting to push local governments to start selling off assets including houses, land, and cars; other assets like stakes in businesses could also be sold to fund local government deficits. [Link]

Lasers

What it’s like to fire Raytheon’s powerful anti-drone laser by Kelsey D. Atheron (PopSci)

A small four wheeler can hold the 10 kilowatt Raytheon system designed to target and destroy drones on the battlefield. [Link]

Previewing Our Wisconsin Polling Experiment by Nate Cohn (NYT)

In an effort to correct for very low response rates in Wisconsin, the NYT attempted to pay respondents to complete one of its polls this cycle; it’s still not clear yet whether the new approach will prove accurate or not. [Link; soft paywall]

Doom

Hedge-fund giant Elliott warns looming hyperinflation could lead to ‘global societal collapse’ by Anviksha Patel (MarketWatch)

Elliott Management’s strategy is premised on buying assets cheap, so it’s not a surprise that they would be bearish towards overall asset prices. Still, some of the language here is pretty strong stuff. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Equity Market Risk Gauge — November 2022

This week’s Bespoke Report newsletter is now available for members.

In this week’s newsletter, we’ve updated our Equity Market Risk Gauge for the month of November, and we also provide a summary of earnings season thus far, highlight downtrends for the mega-caps, check up on market internals, and take a final look at GOP and Democrat odds for the upcoming Mid-Term Elections.

To see our updated Equity Risk Gauge and access everything else Bespoke’s research platform has to offer, join Bespoke Institutional and get half off for the first three months!

Daily Sector Snapshot — 11/4/22

On the Other Hand

Harry Truman is famous (among other things) for saying, “Give me a one-handed Economist. All my economists say ‘on hand…’, then ‘but on the other…” And it’s true. You rarely will see an economic analysis that doesn’t couch one view with an alternative scenario, and you can’t fault them for hedging their bets. Predicting the future is impossible, especially when it involves the direction of the world’s largest economy.

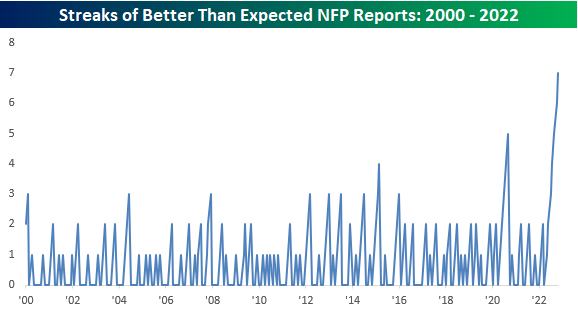

This morning’s employment report also has a number of hands. At the surface, the report was better than expected coming in ahead of expectations (261K vs 193K). As shown in the chart below, this was the seventh straight better-than-expected print and the ninth in the last ten months.

To illustrate just how impressive this recent run has been, the chart below shows streaks of better-than-expected prints in non-farm payrolls (NFP). The current streak of seven is easily the longest such streak since at least 2000.

While job growth in the US economy has consistently surpassed expectations this year, it is important to point out that the pace of job growth isn’t accelerating. This month’s print of 261K was actually the smallest monthly increase since late 2020 and is well off the peak readings seen in 2021 when the FOMC was maintaining its zero interest rate policy. To put this trend in perspective, in 2021 the average monthly change in NFP was 562K. In 2022, that average has declined to 407K, and in just the last three months, the average has been 289K. On the one hand, the job market remains strong. On the other hand, momentum has clearly peaked and there has been a trend of deceleration. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 11/4/22 – Jobs Jobs Jobs

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A man is worked upon by what he works on. He may carve out his circumstances, but his circumstances will carve him out as well.” – Frederick Douglass

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures are rallying nicely this morning on optimism over a relaxing of COVID restrictions in China, and the gains here follow what has been an overnight rally in risk assets around the globe. If these gains can hold, it will help to reverse some of the steep losses we’ve seen this week, but we still have to get through the October Non-Farm Payrolls report. Needless to say, any strength on the jobs or wage front will not be greeted kindly by the FOMC.

Wasn’t November supposed to be a good month for stocks? We’re only three trading days into it, but already the S&P 500 is down close to 4% (-3.92%) in what ranks as the worst three-day start to a month for the index since August 2019 and the 11th worst start since late 1952 (when the five-trading day week on the NYSE began). The chart below shows the first three-day performance for the S&P 500 for every month since 1953 and what really sticks out is the fact that all but two of the months that had weaker starts were all since the start of 2000, while the other two were in December 1973 and December 1975.

We’d also note that this month’s poor start followed October’s exceptionally strong start where the index rallied 5.51% in the first three trading days of the month. That strong start ranked as the 6th strongest three-day starts to a month since 1953.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Tech Layoffs, Data Deluge, Forty Year Inversion – 11/3/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a rundown of the major earnings reports released after the closing bell (page 1) followed by a review of the latest ISM and S&P Global Service PMI data (page 2). We then review hard manufacturing data (page 3) as well as the weak labor productivity figures (page 4). After diving into the latest homeownership rate (page 5) and Realtor.com inventory data (page 6), we finish with a look at the steep inversion of the 2s10s curve (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

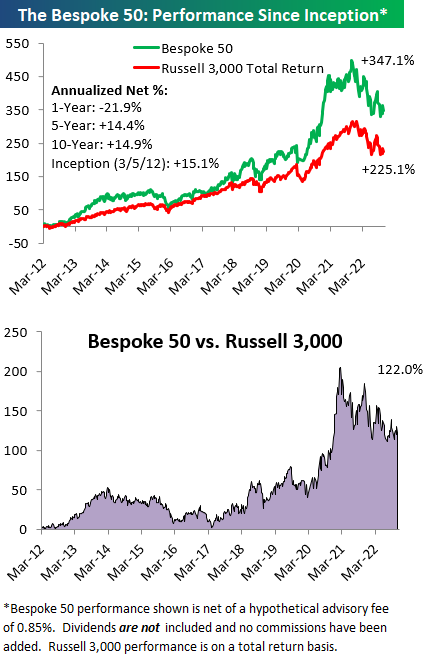

The Bespoke 50 Growth Stocks — 11/3/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were five changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Chart of the Day: Earnings Growth Estimates In Freefall

Jobless Claims Snoozer

Jobless claims continue to be a snoozer. Headed into tomorrow’s nonfarm payrolls report, initial jobless claims were little changed falling 1K down to 217K. Over the past month, claims have been in a relatively tight range of only 12K. That is the tightest one-month range since late June/early July, albeit claims are at slightly healthier levels than back then as well.

On a non-seasonally adjusted basis, claims are at 185.6K, which is the lowest level since 1969 for the comparable week of the year. Claims have been on the move higher as is the norm for the point of the year. In fact, the current week of the year has been one of the most frequent to see week-over-week increases in unadjusted jobless claims with increases 83% of the time since 1967.

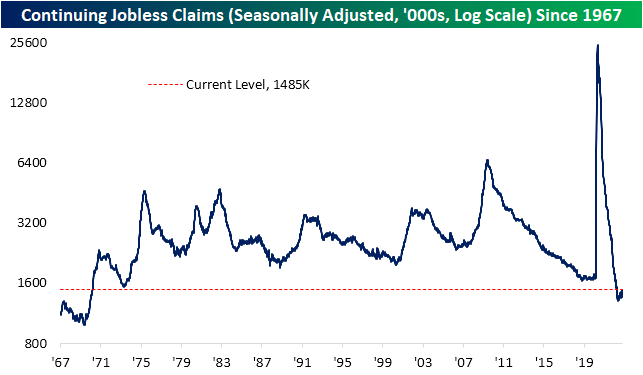

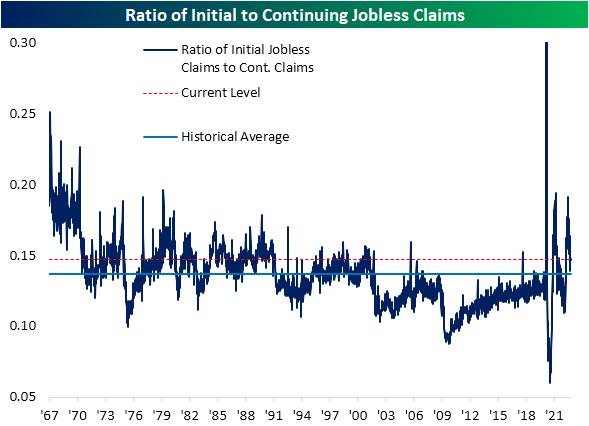

While initial jobless claims have not seen particularly large moves recently, the picture for continuing claims has begun to shift. Although continuing claims are much further below their pre-pandemic range than initial claims, the most recent week saw a move up to 1.485 million which is the highest level since the end of March. As a result, the ratio of initial to continuing claims has moved sharply lower and is closing in on its historical average. That compares to earlier this year when initial claims were running at much weaker levels than continuing claims implying little follow-through on initial claims. Click here to learn more about Bespoke’s premium stock market research service.

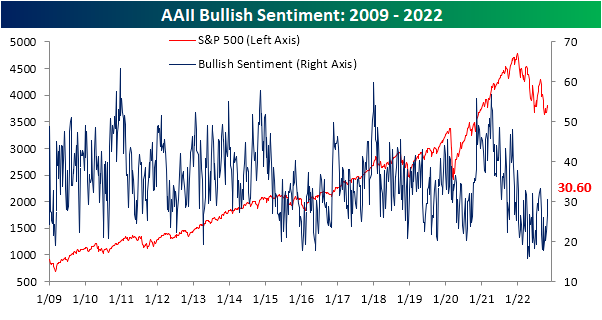

Bears Down By 20

Given the collection period, the latest sentiment data from the weekly American Association of Individual Investors survey would not have fully captured the FOMC meeting yesterday or the market’s reaction to the event. As a result, with the S&P 500 having erased a large portion of late September and early October losses, sentiment took a massive bullish swing. Bullish sentiment gained 4 percentage points for the third weekly increase in a row. Bullish sentiment topped 30% for the first time since the week of August 18th.

Relative to the moves in bearish sentiment, those gains to bulls are outright modest. In the past two weeks, bearish sentiment has seen back to back double digit declines, bringing it from 56.2% all the way down to 32.9%; the lowest level since the end of March. That was the first time that bearish sentiment has seen back to back declines of at least 10 percentage points since 2009, and further back in the history of the survey that has only happened two other times: June 2004 and in the first year of the survey in September 1987.

While back to back double digit declines for bearish sentiment are exceedingly rare, there has been more precedent for bearish sentiment falling at least 20 percentage points in a two week span. In the table below, we show each occurrence that has happened with at least 3 months between the prior occurrence.

As for how the S&P 500 has typically reacted, forward performance has been lackluster.

Given the massive drop in bearishness, the bull bear spread has experienced a massive reversal. At the moment, the spread is only at -2.3. That is the highest reading since the end of March, and the near record streak of consecutive negative readings (31 weeks) appears to be at risk.

Obviously considering only a small share of the losses to bears have gone to bulls, the percentage of respondents reporting neutral sentiment has risen sharply. The reading climbed 8.8 percentage points week over week to 36.5%. That is the highest reading and largest weekly jump since the end of March Click here to learn more about Bespoke’s premium stock market research service.