Daily Sector Snapshot — 1/13/23

Bespoke’s Morning Lineup – 1/13/23 – Bank Bummer

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We ended the year on a strong note growing earnings year over year in the 4th quarter in an increasingly slowing economic environment.” – Brian Moynihan

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Earnings season has arrived, and it has made its presence known with a thud. Of the eight major reports this morning, all but two (Citigroup and Wells Fargo) beat EPS forecasts, and only two (Bank of New York and Wells Fargo) reported weaker-than-expected revenues. The results don’t appear good enough for investors, though. Six of the eight companies that reported are trading down in the pre-market, and the two trading higher (Bank of New York and BlackRock) have seen just muted gains. On the flip side, stocks trading lower in the pre-market have all declined at least 1%, while Wells Fargo and Delta head into the opening bell with declines of over 4%. Given the weak reactions to earnings, overall equity index futures are also weak and indicating a decline of nearly 1% at the open. Interestingly, despite the fact that none of the major reports have been related to technology, it’s the Nasdaq that is doing the worst in the pre-market with a decline of over 1%

The fact that these companies have seen their share prices initially react negatively to their reports is a bit of a letdown but remember that collectively they have performed well to start the year. Except for UNH, all the stocks are positive YTD with gains of at least 3.5%. Heading into this morning’s report, DAL had rallied more than 20% YTD, so a pullback in response to earnings is completely understandable. UNH, though, is another story. Through yesterday’s close, the stock was already down 6.5% YTD and in oversold territory, so the bar didn’t look especially high to begin with.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – 2 Year Breaks Down, Inflation Collapse – 1/12/23

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at the two year yield’s breakdown as the S&P 500 runs into resistance (page 1). Next, we dive into the latest CPI data including what drove today’s print and the potential paths it can take from here (pages 2 – 4). We follow up with a look at transportation costs from Cass (page 5) then run through the details of today’s historically strong 30 year bond reopening (page 6). We finish by taking a look at the plateau in housing inventories (page 7) as housing sentiment is a shade of its former self (page 8)

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

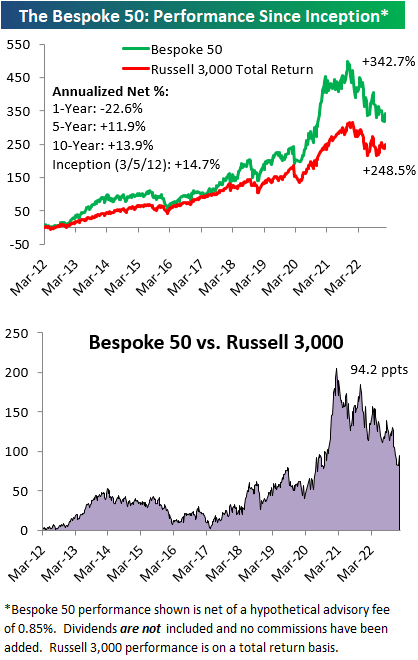

The Bespoke 50 Growth Stocks — 1/12/23

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were twelve changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Weekly Sector Snapshot — 1/12/23

Bears Back Down

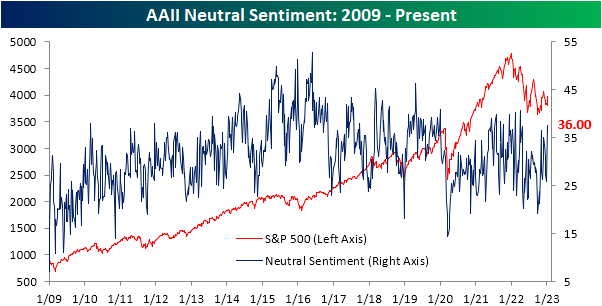

The S&P 500 has rallied impressively in the past week leading up to Thursday’s CPI print, and bullish sentiment has lifted along with it. While the reading remains low, the percentage of respondents to the weekly AAII sentiment survey reporting as bullish rose from 20.5% up to 24%. Bulls were higher only two weeks ago when the reading was at 26.5%

That rise in bulls has meant bearish sentiment has fallen to a notable level. For the first time since the first week of November and for only the eleventh time in the past year, bearish sentiment came in below 40%. Bearish sentiment has now fallen for three weeks in a row, which is the longest streak of consecutive declines since last August as well.

Although bullish and bearish sentiment are sending a more optimistic tone, the bull-bear spread remains heavily in favor of bears at -15.9. That grows the record streak of negative readings to 41 weeks in a row.

Last week, neutral sentiment leaped higher given the mid-single-digit declines in bulls and bears. Some of that move was given back this week with only 36% reporting as neutral. However, that remains an elevated reading at 4.6 percentage points above the historical average. Click here to learn more about Bespoke’s premium stock market research service.

Claims Drop But Were the Holidays Helping?

Initial jobless claims posted another low reading in the latest print, with national seasonally adjusted claims totaling only 205K. That was down slightly from 206K the previous week; a number revised up by 2K. After that revision, this week’s reading was the strongest showing for claims since the end of September.

Before seasonal adjustment, claims were considerably higher at 339.29K. At the end of the year and in the first weeks of a new year, claims tend to experience a significant seasonal increase which appears to be playing out in the current environment. This year’s reading is in line with the comparable weeks of the few years prior to the pandemic. As we also noted last week, this time of year tends to see the largest revisions in claims as well. In other words, from a seasonal perspective, claims can be a bit volatile in terms of actual levels and revised levels. So while the seasonally adjusted reading was solid and the non-seasonally adjusted number is nothing too concerning, the next several weeks will likely provide a clearer reading on how claims are trending.

Turning to continuing claims, this week’s print covered the final week of 2022. Like initial claims, the end of the year saw declines in continuing claims with the latest reading falling to a low of 1.634 million; the strongest level since the week of November 19th. Although that is a solid improvement following multiple months of claims rising rapidly, similary to initial claims, more weeks of data will help to provide a clearer picture given the effects of seasonality during the holidays.

We would also note, that although the drop in claims over the past two weeks has only put a small dent in the recent rise in claims, the 4.89% decline is historically large. That drop impressively ranks in the bottom 3% of all 2-week moves on record. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 1/12/23 – Bring An Umbrella Just in Case

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What weather they shall have is not ours to rule.” – J.R.R. Tolkien

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

In weather-speak, they call an atmosphere like this morning, the calm before the storm. Overnight in Asia, stocks were little changed and that was almost literally the case with the Nikkei rising just 0.01%. Chinese stocks were a little more biased to the upside with a gain of 0.20%. In Europe, the mood is considerably better as major benchmark indices in the region are all up over 0.50%. Bond yields in the US are modestly higher, and both crude oil and natural gas are higher after the latter attempts to bounce from 52-week lows reached on Tuesday following a massive three-week decline.

None of these moves really matter, though, as the 8:30 release of the December CPI – “the most important economic release in generations” – will dictate the tone of the trading day. With the President scheduled to speak on inflation later this morning, there is some speculation that the White House got an early look at the report and is looking to spike the ball on the administration’s policies to combat inflation.

If there’s one place where hyperbole rules, it’s in discussions pertaining to the market. We would argue, though, that the recent moves in natural gas may not have been talked about enough given how large the declines have been relative to history.

Let’s start with the short-term. Over the 15 trading days ending yesterday, natural gas dropped 36.9%. That alone is one of the most extreme downside moves in the history of the contract, but a week ago today, the 15-day decline was 46.4% which was the most extreme downside move on record (since 1990).

From a longer-term perspective, the declines have been just as large. In the 100 trading days ending Wednesday, the front month natural gas future declined 59.8% which also ranks as the most extreme downside move on record. The only other times there were declines of a magnitude in the ballpark of the current drop were in 2001 and 2006.

The scatter chart below compares the 15-day rate of change (x-axis) in natural gas prices to the 100-day rate of change (y-axis). The highlighted section at the bottom left with the most extreme downside moves over both a 15- and 100-day period all occurred so far in 2023. Whereas most other large 15-day declines followed periods when natural gas prices were up over the prior 100 trading days, the current period has been a snowball of weakness on top of weakness.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Chart of the Day: 2022’s Losers Lead the Way

The Closer – Surging Copper, Soaring Franc – 1/11/23

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the surge in copper over the past week and what that has done for the Chilean Peso. We also check in on credit spreads and auto lending (page 1). We then pivot over to a look at the Euro and European stocks (page 2). Next, we dive into the BLS data of expenditure and income data for 2021 (page 3) followed by a recap of the strong 10 year reopening (page 4) and massive crude oil inventory build (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!