Bespoke Stock Scores — 3/26/19

Trend Analyzer – 3/26/19 – Only the Nasdaq (QQQ)

Declines over the past week have pushed all but one index ETF back to neutral from overbought territory. Currently, only the Nasdaq (QQQ) is overbought. QQQ has been a strong performer lately and while other indices have seen declines exceeding 3% over the last week, QQQ is only down 0.13% headed into today’s trading. It is also up the most YTD at 15.74%. On the other hand, the other index ETFs are all neutral with some having collapsed below the 50-DMA. There are now five ETFs below their 50-DMAs with the Core S&P Small Cap ETF (IJR) the furthest below. As IJR edges increasingly closer to oversold, it is now over 2% below its 50-DMA. Along with the Dow (DIA), it is also only seeing single digit returns YTD. While IJR has been exceptionally bad, the other small caps like the Micro Cap ETF (IWC) and Russell 2000 (IWM) have not been much better, as these three are now all down over 3.25%.

Bespoke CNBC Appearance (3/26)

Bespoke co-founder Paul Hickey sat down with Brian Sullivan earlier on Tuesday to discuss markets, the yield curve, and semiconductors. To view the segment, please click on the image below.

Morning Lineup – A Global Sigh of Relief

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Equity investors around the world are breathing a global sigh of relief this morning as most equity markets have at least partially rebounded from Friday and Monday’s weakness. There’s a healthy dose of economic data coming up 8:30 with Housing Starts and Building Permits and then Consumer Confidence at 10 AM. Keep an eye on semis today as yesterday, they underperformed the broader market by a pretty wide margin, and then last night Samsung issued a profit warning. Semis have been the market’s leadership group for some time now, so bulls don’t want to see that group falter.

Please click the link below to read today’s Bespoke Morning Lineup.

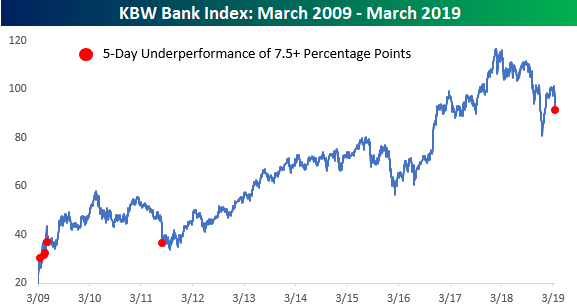

Things are looking up a bit today, but the last five trading days have been hell for bank stocks. After the KBW Bank Index briefly peaked above its 200-DMA last week for the first time since late September, it has been nothing but declines for the group ever since. During the last five trading days, the KBW Bank Index has seen daily declines of 1.32%, 3.02%, 1.53%, 3.92%, and 0.42%. In total, those declines work out to a five-day decline of just under 10% (9.83%) compared to a drop of just 1.22% for the S&P 500.

With bank stocks underperforming by more than 8 percentage points during this stretch, it goes down as the worst relative performance for the group since August 2011. Since the lows of the Financial Crisis, there have only been five other five day periods that saw similar underperformance, and all but the 2011 period occurred during the very early stages of the rally. You don’t see relative underperformance like this in the bank stocks very often.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Relative Underperformance, Yield Curve Diverges, Global Weakness — 3/25/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, in spite of equities’ strong performance so far this year, we highlight the asset’s underperformance relative to commodities and fixed income. Staying on the topic of fixed income, we take a look at the divergence between the long end and the front end of the yield curve, and what kinds of recessionary signals it is sending. Further, we provide an update on the market’s expectations for rate hikes and cuts based on the OIS market. Turning to macro data, we show another weak month of CPB data on global trade and industrial production, though it’s not all bad, as Germany trade and auto industry data is at least supportive.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

B.I.G. Tips – Decile Analysis and Strong Dollar Winners

Chart of the Day: Bottom-Fishing With Biogen (BIIB)

This Week’s Economic Indicators – 3/25/19

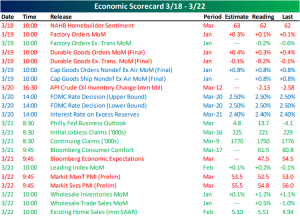

Last week saw 23 releases with pretty much an even split between beats and misses. Homebuilder sentiment was the only release on Monday; coming in unchanged from the prior month but also missing forecasts. Manufacturing data on Tuesday came in somewhat mixed. While Durable goods were weaker, Capital goods were unchanged. As expected, the FOMC did not change rates but their more dovish tone on Wednesday was a major shift. The Philly Fed came in very strong on Thursday thanks to strong shipments, although more forward-looking internals were weaker. To round out the week, much like other global Flash PMIs, the US releases for both service and manufacturing PMIs were weaker than expected.

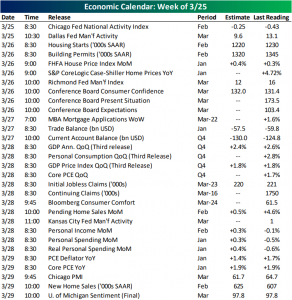

Things are slightly busier this week with 30 releases. The Chicago Fed’s National Activity Index kicked off the week this morning coming in at -0.29 versus expectations of -0.38. The Dallas Fed’s Manufacturing Activity Index was also just released showing some weakness coming in at 8.3. The Richmond Fed and Kansas City Fed counterparts will be released later in the week. In addition to several manufacturing releases, this week will have a heavy slate of housing data with FHFA and Case-Shiller Home Prices on Tuesday alongside Housing Starts and Building Permits. Pending and New Home Sales will also be released later in the week. Thursday we will get the third and final release of Q4 GDP figures which are expected to come in slightly lower.

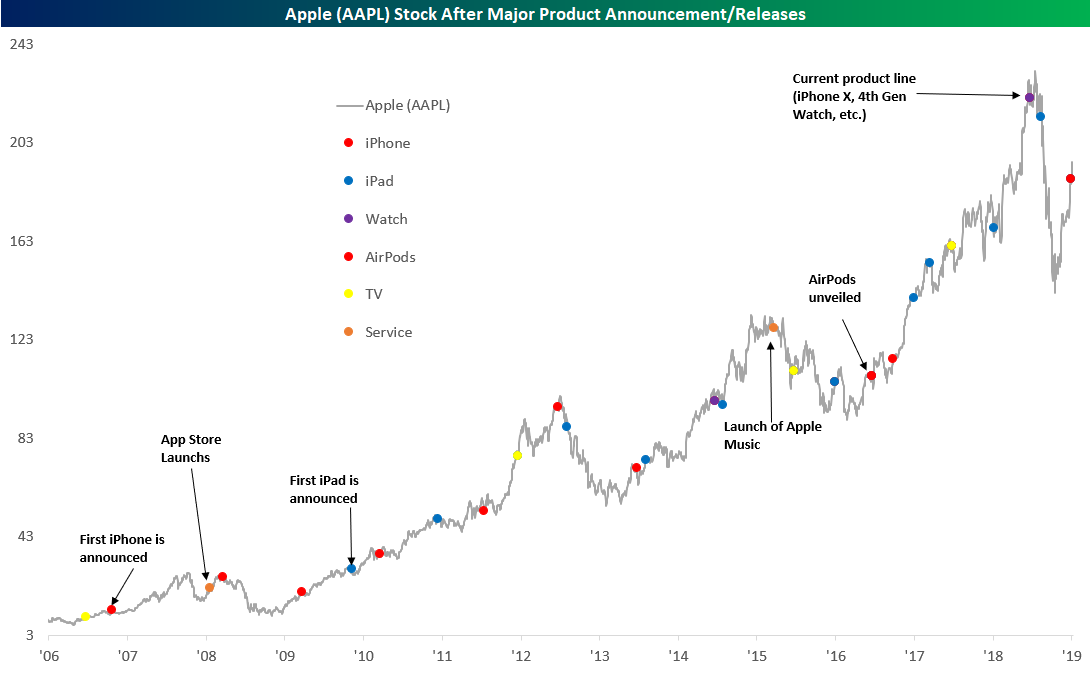

B.I.G. Tips – Apple Product Announcements

Apple (AAPL) will hold an event today at 1PM Eastern where the company is expected to make some big announcements. In addition to updated versions of existing products like their iMacs, iPads, and AirPods, Apple is expected to announce the launch of its own Netflix-like streaming service. That will also not be the only subscription service that the company is rumored to be revealing. It has also been circulated that AAPL plans to unveil a new subscription news service, taking advantage of their already popular news app. In our latest B.I.G. Tips report, we provide a summary of how AAPL stock has performed leading up to and after major product/services announcements over the years, and below we provide an annotated chart of AAPL over the years with color-coded circles to highlight announcements/releases of various products in its stable. To gain access to the full report, please start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Morning Lineup – Moving On

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium. Below is an excerpt:

The weekend’s release of the Mueller Report did not have the kind of fireworks that some were looking for but that markets can’t stand. From a political perspective, we’re probably far from the end of hearing about Russia, the elections, and any obstruction, but based on the market’s complete lack of any reaction this morning, it has already moved on.

Markets will also be trying to move on from Friday’s sharp declines after the yield curve (10y/3m) inverted for the first time in over a decade, and with the curve back in positive territory this morning, that should help stabilize things for now. Don’t forget, though, that there are just six days left in the quarter, and shortly after that Q1 earnings season kicks off, so that should be, at a very minimum, an interesting period for equities.

Following in the heels of Friday’s sharp declines, Asian equities were hit hard overnight. For China, that meant that its streak of 1% gains to kick off the week ended at six. That was still enough to be the longest such streak of 1%+ gains in over a decade.

From a technical perspective, China’s rally is still intact. While the Shanghai Composite has been consolidating gains over the last two to three weeks, the short-term uptrend that has been in place since it broke out in late February remains intact.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.