Housing Starts Retreat, But Still Healthy

Both Housing Starts and Building Permits pulled back in September from their extremely strong August levels. In both cases, the pullback was expected, although in the case of Housing Starts, the decline was larger than expected (1.256 mln vs 1.320 mln estimate). Looking at the charts of both series below, September’s levels remain near their highs of the cycle.

The table below breaks down this month’s report by single and multi-family units as well as regions. While both starts and permits were down this month, all of the declines were in multi-family units (which was a driver of last month’s gains). In fact, in the case of both starts and permits, single-family units were up both on a m/m and y/y basis.

In a post on homebuilder sentiment yesterday, we noted that it would be hard to imagine that the economy is on the cusp of a recession with homebuilder sentiment being so high. Similarly, when we look at the 12-month average of Housing Starts and Building Permits over time, current trends are not suggestive of a broader economic downturn. As shown in the top chart below, every prior US economic recession has historically been preceded by a downturn in the 12-month average of Housing Starts. In some cases, the peak in starts came well before the recession started and in others, it was within a year. Looking closely at the chart, while the 12-month average most recently peaked back in September 2018, it hasn’t yet shown signs of rolling over as it did leading up to prior recessions.

In fact, if we take a closer look at both Housing Starts and Building Permits, the 12-month average has actually started to tick higher again. That’s an important trend because going back to the mid-1960s, there has never been a period where we saw rising levels of starts heading into a recession. Start a two-week free trial to Bespoke Institutional to access our actionable research and interactive tools.

Bespoke Morning Lineup – 10/17/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Weekly Fund Flows Update, Nordic Nosedive, Beige Book – 10/16/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we show the record level in EURNOK and reversal in the past couple of years build up in UST long positioning. We also show what precedent the largest banks have set for earnings given their results so far. We also take a more quantitative look at the Fed’s Beige Book with our Beige Book Index. We finish with our weekly recap of fund flows.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Netflix (NFLX) Earnings On Deck

The charts of the FAANG stocks have left something to be desired over the past several months. Streaming giant Netflix (NFLX) is a prime example. The stock managed to recover nearly all of its late 2018 losses in the first half of 2019, but it gave up the ghost in the wake of July’s earnings report when the company missed subscriber estimates. NFLX has remained in a downtrend in the months since with a recent lower low around support near last November’s lows. Granted, this recent low was still 8.9% above the 52-week low from Christmas Eve of last year. Now at the top of this downtrend, NFLX reports earnings once again tonight after the close and given its historical volatility around earnings, the stock has an opportunity to either break out or break down.

Although the 10.27% one-day decline in response to the last quarter’s report that preceded NFLX’s recent downtrend may sound bad, the move was basically par for the course. Netflix is one of the most volatile stocks on earnings with shares averaging an absolute move the day after earnings of 12.78% across all quarters since 2002. So last quarter’s decline was actually smaller than the average! As shown in the table from our Earnings Explorer tool below, that was the worst full-day decline in reaction to earnings since Q2 2016, but there was actually a larger gap down at the open just one year prior in July of 2018; although most of that decline was regained intraday. Headed into tomorrow, it should come as no surprise to investors if the stock swings wildly regardless of what the results of the quarter are. EPS is estimated to come in at $1.05 and sales are expected to grow to $5,247.5 million.

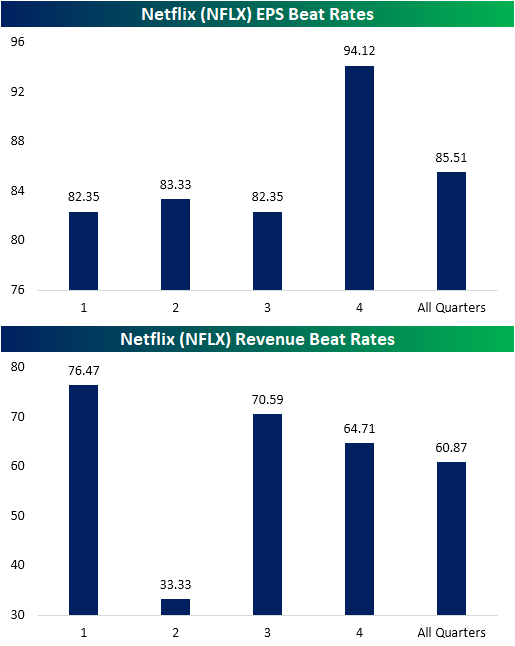

Looking at the historical trends of NFLX’s beat rates, last quarter’s revenue miss could have been expected. NFLX has only exceeded Q2 revenue estimates 33% of the time. The other three quarters have much stronger beat rates. As for today, the third quarter’s revenue beat rate is the second strongest at 70.59%, only behind the first quarter’s 76.47% beat rate. When Netflix has beaten revenue estimates in the third quarter, it has averaged a one-day share price gain of 2.74% with the stock positive two-thirds of the time. On the other hand, when there is a revenue miss in the third quarter, the stock has always declined, averaging -12.3%.

With regards to EPS beat rates, Netflix most consistently exceeds expectations in the fourth quarter having done so 94.12% of the time. Other quarters are a bit weaker in the low-80% range. For the third quarter, as with the first quarter, NFLX has beaten EPS 82.35% of the time.

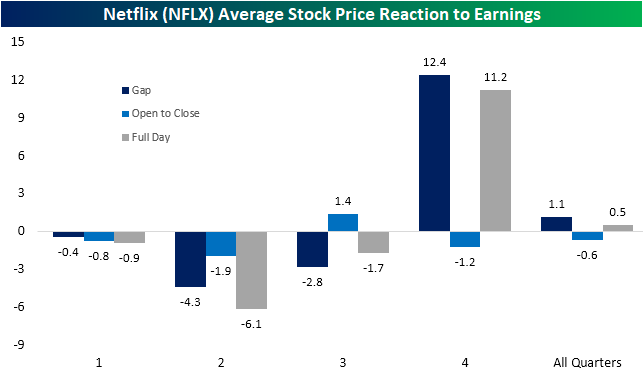

Looking at the average stock price reaction to earnings, last quarter’s decline again could have been expected as the second quarter has averaged the largest gap down, decline from open to close, and full-day decline of any quarter. Third-quarter results have only been slightly better as NFLX averages a gap down of 2.8% and a full day decline of 1.17%. One silver lining, though, is that the third quarter is the only quarter that has seen the stock rise on average (1.4%) from the open to the close after its initial opening gap. Meanwhile, the fourth quarter has typically seen the strongest overall performance with an average gap up of 12.4% and full-day gain of 11.2%. Start a two-week free trial to Bespoke Institutional to access our interactive Earnings Explorer and much more.

Fixed Income Weekly – 10/16/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review which parts of the Treasury curve did not invert this cycle.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Homebuilder Sentiment Surges

Homebuilder sentiment came in significantly better than expected in October rising from 68 up to 71 compared to expectations for the index to remain unchanged at 68. With October’s gain, overall sentiment is currently at its best level since February 2018. Also notable is the fact that over the last ten months, the NAHB Homebuilder Sentiment index is up 15 points. That’s the strongest ten-month rate of change in more than six years. With homebuilder sentiment so strong, it’s hard to imagine that the economy is on the cusp of a downturn.

Looking at the internals of the report, strength was broad-based at a national level as Present and Future Sales as well as Traffic all saw impressive gains. On a regional level, though, it was a bit of a mixed picture. While sentiment in the South and West increased, sentiment in the Northeast and Midwest declined. In the case of the South, though, sentiment hit its highest level since June 2005 (chart below)! Start a two-week free trial to Bespoke Premium to sample our actionable research. If you use this checkout link, you’ll receive a 10% discount on an annual membership if you stick with it past your trial period.

Bespoke’s Global Macro Dashboard — 10/16/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Bespoke Morning Lineup – 10/16/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Earnings, Curve, Banks, Inflation Expectations – 10/15/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we evaluate the potential of a bounce in small caps as well as what the solid results from JPM, C, UNH, and JNJ could mean for the rest of earnings season. Later on we show the breakout for banks and forward performance of the S&P 500 following similarly strong starts to earnings season. We also look at the move in Treasuries including the 3m10y curve closing in positive territory. We finish with a review of the New York Fed’s data on inflation expectations.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Semis – New All-Time Highs…Barely

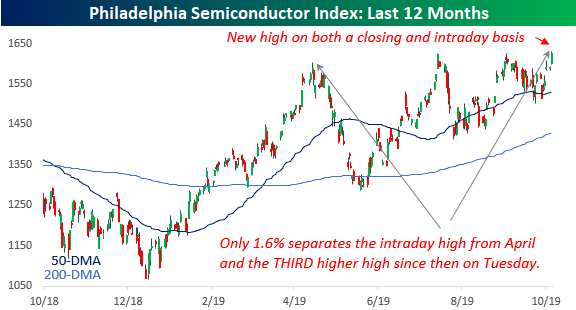

Semiconductors outperformed the overall market on Tuesday (10/15), with the Philadelphia Semiconductor index (SOX) rallying 2.22%. The chart below shows the performance of the SOX over the last year, and while you have to squint, Tuesday’s move saw new all-time highs on both a closing and intraday basis. What’s really amazing about this chart is that while the current high represents the third higher high for the SOX since its peak earlier this year in April, the percentage spread between the April high and Tuesday’s high is just 1.6%. Or to put it another way, July’s high was 1.28% above the April high, September’s high was 0.003% above July’s high, and the current high is just 0.3% above the September high. It doesn’t get much more narrow than that!

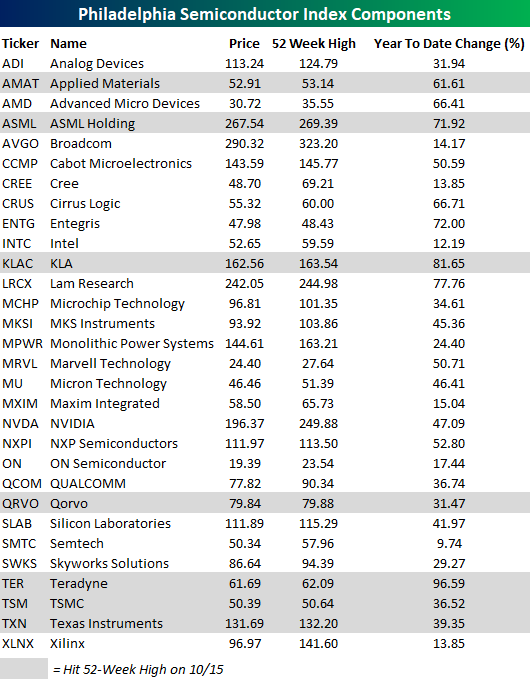

While the SOX hit a new high Tuesday, only a handful of names in the index managed to do so as well. The chart below shows how far each stock in the index finished the day from its 52-week high. Of the 30 stocks in the index, just seven (less than a quarter) hit new highs. Besides the seven new highs (shaded in the chart below), there are only six other stocks in the SOX that are within 5% of a 52-week high, so more than half of the index’s components are more than 5% below 52-week highs. Stocks that are the furthest below their respective highs are Xilinx (XLNX), Cree (CREE), and NVIDIA (NVDA). All three of these names are still down more than 20% from their respective highs, while other big names in the index like QUALCOMM (QCOM), Advanced Micro (AMD), Intel (INTC), and Broadcom (AVGO) are still down over 10% from 52-week highs. So there’s still room for upside in the index if these big names can play more catch up.

The table below lists each of the 30 stocks comprising the SOX along with their YTD change through 10/15. So far this year, the average YTD performance of the stocks in the SOX is a gain of 43%! The top-performing stocks in the index so far have been Teradyne (TER), which has nearly doubled, KLA-Tencor (KLAC), and Lam Research (LRCX). All three are up over 75% YTD. On the downside, there aren’t any, but Semtech (SMTC) is the only stock in the index that’s up less than 10%. Start a two-week free trial to Bespoke Premium to sample our actionable research. If you use this checkout link, you’ll receive a 10% discount on an annual membership if you stick with it past your trial period.