Sentiment Tanks

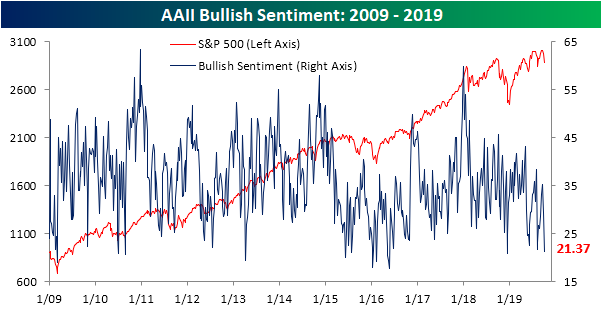

As weak economic data over the past week has sparked selling in equity markets, the S&P 500 has experienced its worst first two days to a Q4 since 2009 with the index falling just a hair under 3% so far in October. As a result, bullish sentiment has also taken a fairly dramatic negative turn. AAII‘s survey of investor sentiment only saw 21.37% of respondents report as bulls this week. That is an eight percentage point decline from one week ago. While the first couple of weeks of August saw a much sharper decline of 16.78 percentage points, this most recent drop brings bullish sentiment to its second-lowest reading of the past year. In fact, last December’s 20.9% was the only lower reading for bullish sentiment going back to 2016. Bullish sentiment is also now over one standard deviation below its historical average.

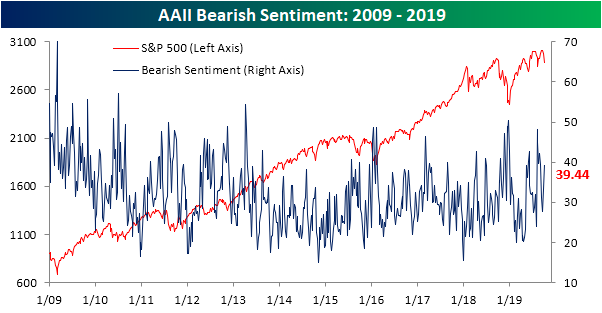

Pessimistic sentiment, rather than neutral, took the lion’s share of these losses as bearish sentiment rose to 39.44%. That is up 6.2 percentage points from last week’s 33.26% reading. While bullish sentiment has come in lower only a few times in recent memory, bearish sentiment is now back to similar levels as August. The bull-bear spread is the widest (in favor of bears) since August as well.

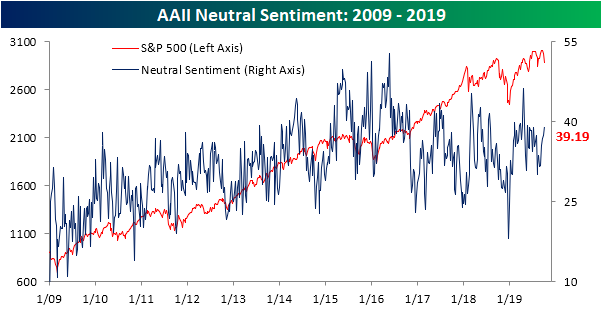

Although the largest share of losses to bulls did not go to the neutral camp, neutral sentiment nonetheless rose to 39.19%. As with bearish sentiment, this increase does not bring sentiment to any sort of historical high, but it is the highest level since late May. Additionally, neutral sentiment is back to more elevated levels that had been observed throughout the first half of this year. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Jobless Claims Flat

Just a month ago, initial jobless claims fell to one of their lowest levels since April’s multi-decade lows. Since then claims have risen for three straight weeks, to 219K today. That is the longest such streak of consecutive increases since the back half of May and early June. Forecasts were expecting a print of 215K, which would have been unchanged from last week’s revised number. Jobless claims are now back to where they stood at the last week of August and are just 1K higher from where they stood a year ago.

With the last week of August’s datapoint of 219K being replaced by an equivalent reading this week, the four-week moving average was unchanged from last week. Interestingly, there was no change year-over-year as well. Since 2000, the only other times this has happened (no change both WoW and YoY) was on August 23rd of this year, and in August of 2007. Although claims remain at very healthy levels relative to the past, this lack of change is just another example of the deceleration in improvements that we have highlighted in the past.

Coming in at 172K, NSA claims fell 3.4K this week. Similar to the seasonally adjusted data, non-seasonally adjusted claims are right near where they stood one year ago. This week’s reading was just 0.2K lower than the current week of the year in 2018. In regards to seasonal patterns, this year’s low has most likely been put in place by now, and claims will trend higher into the end of the year. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Consumer Pulse Report — October 2019

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

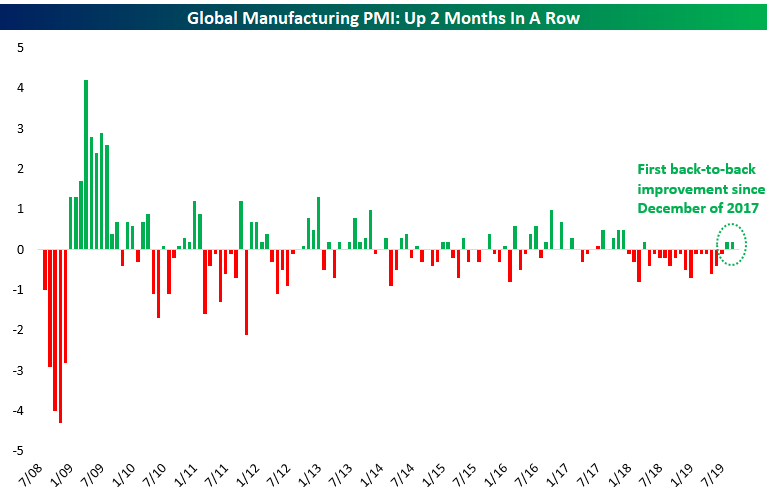

Two Months of Gains for Global Manufacturing PMI

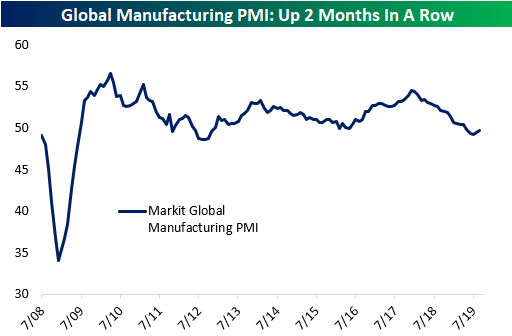

The weak US ISM Manufacturing reading earlier this week has sent the US equity market sharply lower over the last two days. At the same time, though, we’re starting to see a pick-up in the Global Manufacturing PMI reading from Markit. Weak global manufacturing has been one of the best bear cases over the last year. But last month this reading ended a 15-month streak of MoM declines, and now it’s up two months in a row. While it’s still below the 50 level that marks the dividing line between growth and contraction, the recent strength is not to be overlooked. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

US Equity Indices Back to Oversold

The S&P 500 is down 2.99% over the first two days of October, which is the index’s worst start to Q4 since 2009. In 2009 the S&P fell 3.01% over the first two days of October on concerns related to an unexpected decline in manufacturing and falling auto sales (sound familiar?). After that two-day drop, though, it went on to rally 8.77% from that point through the end of the year. Investors would certainly love a repeat of that action at this point. Below is a quick look at the S&P 500’s price chart. The recent highs made in mid-September represent a pretty significant double top at this point, and yesterday’s break below the 50-day moving average was a negative as well. Heading into today, it will be important for the S&P to hold the bottom of the multi-month uptrend channel that’s currently in place, but it’s not looking great in early trading as futures are down pre-market.

Below is a look at the selloff through our Trend Analyzer tool. As you can see, US index ETFs have really tanked over the last week, falling 3-5% across the board. Last week every one of the index ETFs we track were solidly above their 50-day moving averages, and now they’re all below their 50-DMAs and either near or at oversold levels.

Looking at sectors, only the three defensives (Consumer Staples, Real Estate, Utilities) remain above their 50-day moving averages, but even they have fallen within their ranges over the last week. Materials, Communication Services, Energy, and Health Care are the sectors that have already moved into oversold territory, with Health Care the most oversold at more than two standard deviations below its 50-DMA. Start a two-week free trial to Bespoke Premium to access our Trend Analyzer tool and our popular equity market research.

Bespoke’s Morning Lineup – 10/3/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Auto Sales, Mortgage Applications and Foreclosures, EIA, Fund Flows – 10/2/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we show just how bad breadth was today across GICS Level 2 industry groups with particular focus on the weakness in autos, despite stronger data. Next, we turn to some housing data including MBA’s mortgage applications and monthly mortgage payment performance from Black Knight. We finish with our weekly looks at EIA petroleum stockpiles and ICI fund flows.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bad Breadth on Both Sides of the Atlantic

On a Wednesday when the Dow was down almost 2% and the S&P 500 down nearly 1.8%, it’s no surprise that market breadth was very weak. For the S&P 500 as a whole, just 25 stocks in the index were up on the day. What makes today’s sell-off even more severe is that breadth was not only bad here, but it was also very poor on the other side of the Atlantic where only 12 stocks in the entire STOXX 600 were up on the day. On a combined basis, just 37 of the 1,100 stocks in the S&P 500 and Euro STOXX 600 were up on the day, and that doesn’t happen very often. The last time breadth on both sides of the Atlantic was this week was on August 5th, and there have only been 30 trading days since the start of 2009 where the combined number of advancing stocks in the two indices was less than 50.

The chart below shows the S&P 500 going back to the start of 2009, and in it we have included red dots to denote each time there was similarly weak breadth. Prior to the two most recent occurrences (today and 8/5), you have to go all the way back to September 2015 to find the last one. What’s interesting to note about these prior occurrences is that nearly all of them came in bunches during periods where the market was in consolidation/correction mode. In fact, the only one that occurred in isolation during a market uptrend was on 6/20/13 when the market freaked out about the Fed’s ‘taper’ program. Remember that one? Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

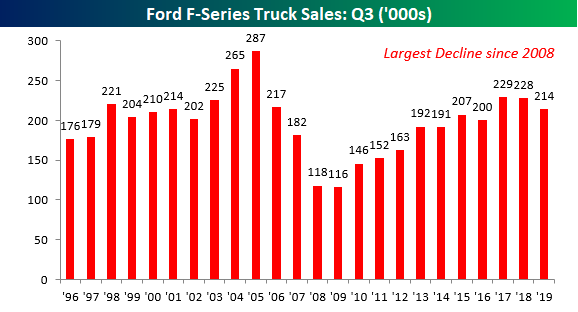

Ford Truck Sales Slow

While Ford used to release vehicle sales on a monthly basis, that changed in 2018 when the company began to switch to a quarterly reporting period. Whenever companies make the decision to give less rather than more performance data, it usually comes at a time when the numbers are getting worse rather than better. After all, have you ever heard of a company choosing to give less information when their business is booming? With that in mind, it shouldn’t come as much of a surprise that sales figures for Ford vehicles have been weakening. This morning, Ford released sales figures for the third quarter, and overall sales fell 5.6% relative to the third quarter of 2018 and are down 3.9% on a YTD basis relative to last year.

On these pages, we tend to focus on sales of Ford F-Series trucks. The reason for this is that sales of pickup trucks are often a sign of strength or weakness in the small business and construction sectors as these types of businesses are the most common users of these vehicles. Similar to the overall sales figures from Ford, sales of F-Series trucks have also been weak which suggests a more sluggish environment for small businesses. In the third quarter, total sales came in at 214,176 which was a full 6% below the same quarter last year. That may not sound like much, but the last time there was this large of a decline in Q3 sales on a y/y basis was in 2008.

Year to date, total sales of Ford F-Series trucks are down 2.4%, falling from 679K down to 662.6K. Here again, that may not sound like a whole lot, but it is only the second time since 2009 where the y/y sales pace was negative and this year’s decline is the largest since 2009. Start a two-week free trial to Bespoke Institutional for full access to our research and market analysis.

Fixed Income Weekly – 10/2/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we take a look at how corporate debt issuance is looking.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!