2020 Outlook – Housing

Our 2020 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2020.

The 2020 Bespoke Report contains sections like Washington and Markets, Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2020 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Housing” section of the 2020 Bespoke Report, which takes a close look at the state of this key area of the economy and whether strength in 2019 can continue in 2020. Lower interest rates in 2019 helped housing recover from a weak 2018, and there are signs that the strength can continue into 2020. We tell you why in this section.

To view this section immediately and all other sections, become a member with our 2020 Annual Outlook Special!

2020 Outlook – Commodities

Our 2020 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2020.

The 2020 Bespoke Report contains sections like Washington and Markets, Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2020 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Commodities” section of the 2020 Bespoke Report, which focuses on performance and long-term trend shifts of every major commodity.

To view this section immediately and all other sections, become a member with our 2020 Annual Outlook Special!

Bespoke’s Morning Lineup – 12/10/19 – Small Business Sentiment Improving

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Copper Spike, Decile Data, Positioning Pushed – 12/9/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a review of copper’s breakout after Friday’s rare 3% rally. Next, we look at what has driven stocks in the US and Europe with a decile analysis based on several factors like leverage, EPS growth, dividend yield, P/E, and more. We finish with Commitment of Traders data showing investors going long crude and short interest rates.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bear Market Performance

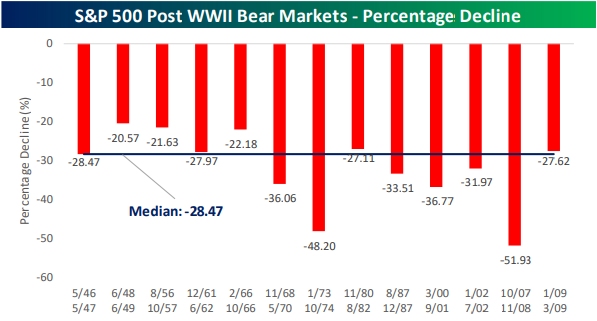

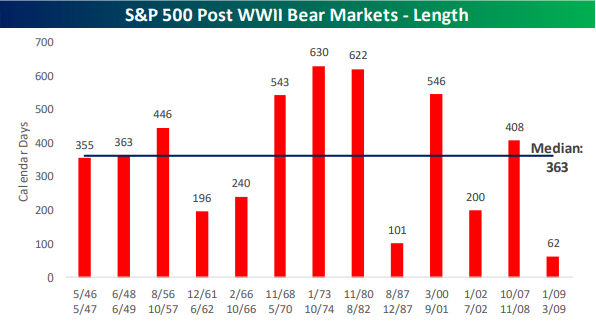

On Friday, we released the first taste of our 2020 outlook report with the Market Cycles and Economic Cycles sections. As the S&P 500 closed at another record high in November (currently just under a quarter of a percent away from this high), the bull market remains fully intact as the picture looks very different from the time of our last end-of-year report when the bull market was on the verge of coming to an end. We define a bull market as any period in which the S&P 500 rallies 20% or more (on a closing basis) without a 20% or larger drawdown. Bear markets, on the other hand, are a 20% decline from a high without a 20% rally in between.

Even though we are far from a bear market (S&P 500 would need to fall to 2522.9 from the November 27th high to meet the criteria), in the Market Cycles section, in addition to gauging where in the cycle we currently stand, we also highlighted equity market performance during bear markets. Of the thirteen post-WWII bear markets, the median decline was closer to 30% (median: -28.47%). The least severe bear market was a 20.6% decline from June 1948 to June 1949, while the most severe was during the credit crisis when the S&P 500 fell close to 52%!

There have been a number of bear markets that have been relatively short (200 days or less), but most tend to be drawn out lasting over a year. The shortest bear market was just 62 days from January 2009 through March 2009, but that was basically just an extension of the prior one from the Credit Crisis. The longest bear market in the post-WWII period was 630 days beginning in January 1973 and ending in October 1974. Sign up using our 2020 Annual Outlook Special to gain access to the entire section on Market Cycles and the full publication to be released by year end.

Mega Cap Exposure By Sector

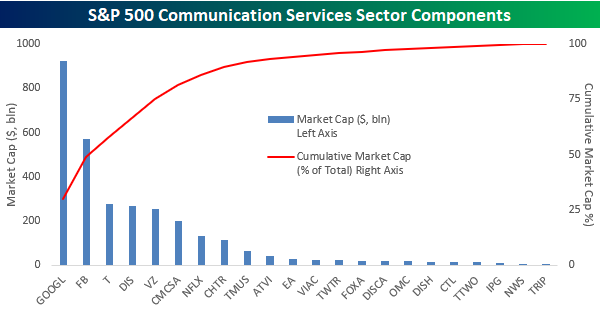

With all the talk about a potential rotation from large cap stocks to small caps, we wondered which large cap sectors were the most exposed to so-called mega cap stocks i.e., those companies with market capitalizations greater than $100 billion. Within the S&P 500, there are currently 61 stocks meeting the criteria of a mega cap. As you might have guessed, Technology has the largest number of mega cap stocks with 15, followed by Health Care with 12. On the other end of the spectrum, the Real Estate sector doesn’t have a single mega cap, while Materials and Utilities each have one.

The table below is sorted by sectors that have the greatest exposure to mega cap stocks in terms of the market cap of these stocks as a percentage of the sector’s total market cap. By this measure, Communications Services actually has the greatest exposure with nearly 90% of its market cap coming from stocks with market caps in excess of $100 billion. Behind Communications Services, other sectors with a large exposure to mega caps include Technology, Consumer Staples, and Health Care. If large cap stocks were to fall out of favor, these sectors would likely come under pressure.

In the chart below, the blue bars show the market cap of each stock in the S&P 500 Communication Services sector (left axis) while the red line shows the cumulative market cap of stocks in the sector as a percentage of total market cap. For example, Alphabet’s (GOOGL) $924 billion market cap accounts for 30% of the sector’s total market cap, and then when you add in Facebook (FB), the total market cap of those two stocks accounts for 49% of the sector’s market cap. Moving out further to the right, the top five stocks in the sector account for 75% of the sector’s market cap while the top eight stocks, which each have market caps above $100 billion, account for just under 90% of the sector’s entire market cap. After that, the fourteen remaining stocks in the sector could completely disappear and the impact on the sector wouldn’t be much more than a 10% correction! Start a two-week free trial to Bespoke Institutional to access our research reports, interactive tools, and more.

Longest Expansion, Lackluster Growth

Below is an excerpt from one of the first sections of our 2020 Outlook Report that was released on Friday discussing Economic Cycles which provides our outlook for the economy and equity market performance surrounding economic expansions and recessions:

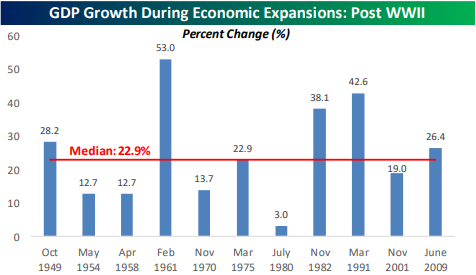

With this being the longest expansion on record, and still in good health based on the November jobs report, it wouldn’t be a leap to assume that both the stock market’s performance and economic growth during this period have also been among the best. The reality, though, isn’t quite the case.

Starting with the stock market, the S&P 500 has rallied more than 230% since the end of the recession in June 2009 which is stronger than any other expansion. It is also only the third post-WWII expansion where the S&P 500 more than doubled. Besides those three periods, though, the stock market’s gain during all other expansions was less than 55%.

Where the current expansion has been lacking, though, is in terms of economic growth. One would think that with a record economic expansion in terms of length, that overall growth would also be strong. As shown in the charts below, four other expansions have seen a stronger level of total growth than the 26.4% level in the current period (median: 22.9%). Sign up using our 2020 Annual Outlook Special to gain access to the entire section on Economic Cycles as well as other individual sections and the full publication to be released by year-end.

S&P 500 Leading and Lagging Industry Groups

Friday’s rally in the S&P 500 helped to bring the S&P 500 right back within spitting distance of its record closing high from right before Thanksgiving and back up above 25% in terms of its YTD gain. While the S&P 500 wasn’t quite able to close at a new high last Friday, a number of groups did, and in most cases, these are also the most extended groups in the market.

Topping the list is Health Care Equipment and Services. While the group has trailed the S&P 500 on a YTD basis with a gain of just below 21%, it is nearly 7% above its 50-day moving average and closed at a 52-week high on Friday. Besides Health Care Equipment and Services, the next five groups that are trading the furthest above their 50-DMAs also closed at 52-week highs on Friday. Two other groups also closed at 52-week highs on Friday but are less extended relative to the 50-day than the S&P 500. Consumer Durables is up 28.5% YTD but is just 3.3% above its 50-DMA, while the Food Beverage & Tobacco group is just 2.5% above its 50-DMA and sitting on a YTD gain of 18.8%.

While the groups mentioned above have been leading the market heading into this week, there are actually three times as many groups less extended than the S&P 500 as there are groups that are more extended (from their 50-DMAs). The biggest laggards have been Real Estate and Utilities. Both groups are more than 3% below their 52-week highs as well as below their 50-DMAs. The only other group below its 50-DMA is Retailing which is pretty disappointing given that Christmas is just eleven days away. While Retailing is still up over 21% YTD, it is one of just four groups that are down 5%+ from their 52-week highs. The others are Consumer Services, Autos & Auto Components, and Energy. Energy has by far been the biggest disappointment in the equity space this year as it’s down nearly 14% from its 52-week high and up only 3.26% YTD. Start a two-week free trial to Bespoke Institutional to access our research reports, interactive tools, and more.

Bespoke’s Morning Lineup – 12/9/19 – Quiet Start Just Below Record Highs

Friday’s rally took the S&P 500 just below its record high and helped to make what was heading into the day a negative week positive. Small caps led the charge with the largest gains, while the Dow (DIA), Nasdaq 100 (QQQ), and Russell Mid Caps (IWR) were the only losers. Relative to each index’s trading range, the picture is the same, though. The market is overbought, but no longer at extreme levels.

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Bespoke Brunch Reads: 12/8/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2020 Annual Outlook special offer.

Trainwrecks

Uber discloses 3,000 reports of sexual assault on U.S. rides last year in its long-awaited safety study by Faiz Siddiqui (WaPo)

2018 alone saw 3,000 sexual assaults during Uber rides in just the US, reflecting a staggering risk for riders. A recent safety report also tallied 97 fatal crashes involving riders, 19 fatal physical assaults of riders, and more chaos during trips. [Link; soft paywall]

“Peloton Husband” Speaks Out by Alec Beall (Psychology Today)

Social media users unloaded on the popular stationary bike brand this week, criticizing the framing of an ad that depicted a video log of a woman using a bike her husband got her as a gift. The actor published a response to the vitriol this week. [Link]

TeamHealth sent thousands of surprise medical bills in 2017 by Caitlin Owens (Axios)

Investigations into the practice of surprise billing revealed physician staffing firm TeamHealth used surprise bills to increase the rate at which it billed insurers. [Link]

Immigration

How McKinsey Helped the Trump Administration Detain and Deport Immigrants by Ian MacDougall (ProPublica)

Reporting by ProPublica and the New York Times reveals that consulting giant McKinsey played a critical role in developing practices which have attracted the greatest condemnation over the past couple of years: cutting food and medical care allocations, as well as detainee supervision. [Link]

Trump gave states the power to ban refugees. Conservative Utah wants more of them. by Griff Witte (WaPo)

While the Trump Administration is doing everything it can to reduce the number of refugees that the United States accepts every year, deeply Republican Utah is happy taking in more new arrivals. [Link; soft paywall]

Nuptials

Pinterest And The Knot Will Stop Promoting Wedding Content That Romanticizes Former Slave Plantations by Clarissa-Jan Lim (BuzzFeed News)

Two large online wedding platforms will no longer promote venues and content that romanticize weddings at plantations. [Link]

Tech Trends

Unintended Perk of the Online Mattress Boom: Never-Ending Free Trials by Stephanie Yang (WSJ)

With dozens of new mattress companies offering free trials that last more than three months, savvy consumers are taking advantage. [Link; paywall]

Inside Larry Page’s Turbulent Kitty Hawk: Returned Deposits, Battery Fires And A Boeing Shakeup by Jeremy Bogaisky (Forbes)

Google co-founder Larry Page’s flying-car company promised that by the end of 2017, customers could purchase one of the light personal aircraft. Unfortunately, deployment hasn’t been so easy. [Link]

Trade Tales

Illegal gold flowing through Miami is a ‘direct threat’ to U.S. national security, Rubio says by Alex Daugherty and Nicholas Nehamas (Miami Herald)

Illegal gold miners in Latin America tend to route their product through Miami, and while the negative effects of the mining aren’t directly felt by Floridians that doesn’t mean they aren’t serious. [Link]

Visualized: Ranking the Goods Most Traded Between the U.S. and China by Asley Viens (Visual Capitalist)

A helpful point of reference: the categories of trade goods that are most-traded between the United States and China. US imports are dominated by cell phones, computers, and routers, while exports to China amount to soybeans, airplanes, and some cars. [Link]

Workplace Wonder & Woe

Starbucks Discloses Gender and Racial Pay Gap: There Isn’t One by Jeff Green (Bloomberg)

In a remarkable break from the norm, the nation’s largest coffee chain delivered a diversity report that showed no gap in pay between men and women and no racial pay gap either. [Link; soft paywall, auto-playing video]

Emotional Baggage by Zoe Schiffer (The Verge)

A remarkable catalogue of management failure and the excessive work culture of popular luggage brand Away, where workers were subjected to dramatic demands by a management desperate to grow. [Link]

Exclusive: CalPERS Fires Most of Its Equity Managers (Chief Investment Officer)

California’s public pension has fired most of the funds it uses to manage its external equity investment portfolio, taking the allocation to that space from $33.6bn to $5.5bn and reducing 17 managers to just 3. [Link]

Media Matters

Celebrities Seek Her Advice. M.B.A.s, Executives Line Up for Her Harvard Class. by Kathryn Dill (WSJ)

Harvard Business School offers a specific class on the business of stardom; this op-ed by the professor discusses her approach to the world of athletes and performers. [Link; paywall]

The Irishman Gets De-Aging Right—No Tracking Dots Necessary by Angela Watercutter (Wired)

A look at the intense technology required to make old actors young again, deployed to great effect in The Irishman. [Link]

The Kingdom, the Heavyweights and the $60 Million Prize Fight in the Desert by Joshua Robinson (WSJ)

This weekend featured a massive prize fight hosted by the Kingdom of Saudi Arabia, featuring a temporary 15,000 person stadium, a $60mm purse, and the kind of glitz only money can buy. [Link; paywall]

Economics

The myth of crowding out by Jamie Powell (FTAV)

A summary of a recent paper that contradicts the widely-held belief that government budget deficits “crowd out” private investment by soaking up capital that would otherwise go to private projects. [Link; registration required]

Science

Ford is making car parts—with waste from McDonald’s coffee beans by Amelia Lucas (CNBC)

The waste from coffee bean roasting at McDonald’s is being put to good use, getting included in auto parts used by Ford that reduce waste both during driving (the parts are lighter) and production (the parts use less energy to make). [Link]

How the 2010s Changed Physics Forever by Ryan F. Mandelbaum (Gizmodo)

A review of the biggest achievements of the decade in physics, from CERN’s Higgs bosons to the minute fluctuations caused by massive gravitational waves. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!