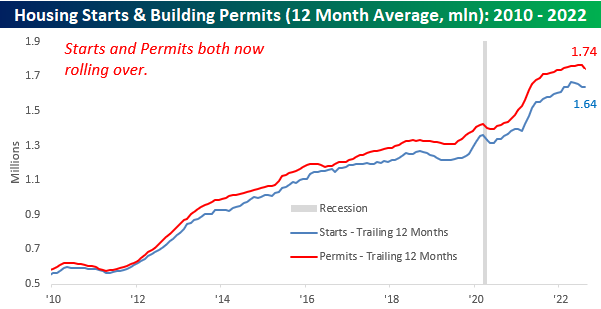

Housing Starts and Permits Mixed But Still Trending Lower

Relative to expectations, Tuesday’s report on Building Permits and Housing Starts was mixed, but overall, it was pretty lousy. Housing Starts exceeded expectations by over 100K, but Building Permits missed expectations by nearly 100K, and as shown in the table below, both are currently down on a year/year basis. Within the better-than-expected Housing Starts report, practically all of the strength was in multi-family units which increased 28% m/m. Single-family units were also positive but increased at just a fraction of the rate of multi-family units. Building Permits were a more gloomy part of the report with the headline reading down 10% m/m and 14.4% y/y. On a regional basis, Permits were down across the board with weakness concentrated in the Northeast and South.

As we have highlighted frequently over the years, Housing Starts have been an excellent leading indicator of the economic cycle. With the exception of the COVID crash, every other recession since the mid-1960s was preceded by a rollover in the 12-month average of Housing Starts (even ahead of COVID, Housing Starts technically rolled over from a peak, but nothing of the magnitude like they did ahead of prior recessions). The current magnitude of decline from the recent peak is by no means near the severity of rollovers leading up to prior recessions, but there has been a clear trend of weakness in this reading with four straight months of declines in the 12-month moving average.

Looking more closely at the post-financial crisis trends in Housing Starts and Building Permits, both appear to have reached at least a short-term peak. Building Permits had been holding up in the months leading up to August’s report, but with a current reading of 1.517 million replacing a reading of 1.772 million from 12 months ago, the one-year average took a sharp turn lower. In fact, the last time it dropped as much as it did this month was back in mid-2009.

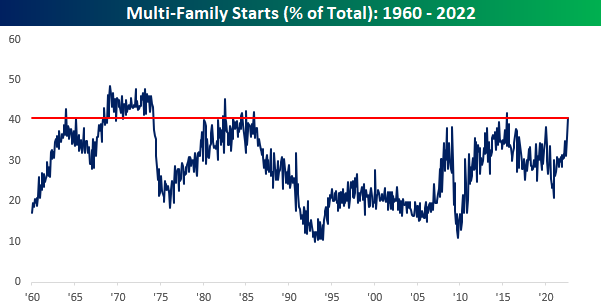

Finally, with the release of each month’s Housing Starts report, a phrase you increasingly hear is something along the lines of “but all the strength was in multi-family units”. As noted above, that was the case again this month and so much so that multi-family starts accounted for over 40% of all starts. Relative to recent history, that’s a very high percentage, and outside of one month in June 2015 when the reading was distorted due to the expiration of a tax break for multi-family units in New York, it’s the highest reading since 1985. Given their smaller size, multi-family units aren’t considered to be nearly as economically impactful as single-family units and therefore suggests that the strength of the August report wasn’t as much as it looked at the surface. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 9/20/22 – Weak Start as Fed Meeting Begins

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The sea is dangerous and its storms terrible, but these obstacles have never been sufficient reason to remain ashore.” – Ferdinand Magellan

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Just like yesterday, futures are lower this morning as interest rates continue to make new multi-year highs while crude oil is marginally higher. The major news event of the overnight session was a 100 basis point rate hike from Sweden’s Riksbank. That was the largest rate hike for the central bank since 1992. In economic news, Germany’s headline PPI increased 7.9% month over month. Yes, you read that right- month over month. In the US, Building Permits and Housing Starts came in mixed relative to expectations. Housing Starts were expected to come in roughly unchanged at 1.45 million, but the actual reading came in at 1.575 million. Building Permits, however, missed expectations by just about as much as starts beat (1.517 million vs 1.610 million consensus forecast).

As has been the case for most of the year, interest rates are on the rise again this morning. The 2-year and 10-year US Treasury yields are up about 4 basis points (bps) pushing both up to new multi-year highs. What’s somewhat notable about the moves in the last 24 hours is that for the first time in just over three months, both the 2 and 10-year yields are at 52-week highs.

In the case of the 2-year yield, its yield has been hitting 52-week highs pretty much every day since Labor Day, but the 10-year yield only took out its June highs yesterday. No matter how many times we say it, it’s hard to imagine that less than nine months ago, ten-year yields were at 1.5% while two-year yields were less than 0.75%.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Biggest Pandemic Losers

With President Biden declaring that “the pandemic is over” on 60 Minutes last night, we thought we’d take a look at stock market performance since the pandemic began. At its peak on January 3rd, 2022, the S&P 500 was up more than 40% from its closing price on February 19th, 2020 — the peak reading for the index prior to the COVID Crash. After entering bear market territory in 2022, the S&P is currently only 14% above its pre-COVID high. In the Russell 1,000 — another large-cap index — 41% of stocks are now trading below their closing price on February 19th, 2020. 20% of stocks in the index are down more than 20%! Given that two and a half years have passed, we think it’s safe to say that any stock down 20% from pre-COVID levels has been a “pandemic loser.” At least at this point in time.

Below are stocks with market caps above $15 billion that are down at least 20% from their closing price on 2/19/20. Names like Boeing (BA), Delta (DAL), Uber (UBER), and Las Vegas Sands (LVS) were some of the initial “lockdown losers” that never really recovered, but other stocks that were initially viewed as “lockdown winners” are also on the list like Netflix (NFLX), Meta (META), Spotify (SPOT), and Zoom Video (ZM). Go figure.

Boeing (BA) and Intel (INTC) have been two of the biggest losers since pre-COVID with declines of more than 56%. Other “blue chips” that have been crushed since the pandemic hit include Biogen (BIIB), Citigroup (C), General Electric (GE), Verizon (VZ), 3M (MMM), Square (SQ), Disney (DIS), Adobe (ADBE), and salesforce (CRM). It’s interesting that there’s representation from nearly every sector of the economy on this list. The only sector that’s NOT included is Energy, which is crazy since the sector was one of the hardest hit in the early days of COVID as the price of oil even went negative for a day.

Of course, COVID isn’t the reason why all of these large-cap stocks are now down so much since the pandemic began, but the performance numbers are the performance numbers, and there’s no getting around it. Management at big travel & leisure companies have always wished COVID never happened, but more and more companies in sectors like Tech that thought the pandemic might be a game-changer for them in a positive way are now staring at big 2+ year declines thinking “what the hell just happened.” Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 9/19/22 – More of the Same

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Objects in motion stay in motion in the same direction unless acted upon by an unbalanced force.” – Isaac Newton

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

There’s very little in the way of economic or earnings data this morning, the Fed is in its blackout period, and the buyback window is closed. Therefore, there appears to be very little in the way of catalysts to interrupt the current path of equities which has been lower and interest rates which have been higher. Futures are indicating a decline of about 0.75% at the open for the S&P 500, and the 10-year yield is above 3.5%. The only economic report on the calendar today is homebuilder sentiment, and given the moves in interest rates, it’s hard to imagine an upside surprise.

The negative start to this week follows what was a lousy week for not just US equities but equities all over the world. US stocks were easily the worst performers last week with the S&P 500 (SPY) and Nasdaq 100 (QQQ) both falling 5%, but other major regional equity ETFs all fell at least 2.5%. Of the nine ETFs listed below, they are all at least 4% below their 50-DMAs, all of them are oversold, and all but three (SPY, ACWI, and VPL) are down 20% YTD. It’s not even three-quarters finished, but 2022 is already shaping up to be one of the worst in the post-WWII period for not just US stocks but stocks all over the world.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 9/18/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Wealth

U.S. household wealth suffers record drop in second quarter by Dan Burns (NASDAQ/Reuters)

Rising interest rates and falling asset prices are unwinding many of the huge wealth gains from the pandemic period when soaring prices sent US net worth above $150trn. [Link]

Gulf States, Rich From Oil, Spread Influence With Financial Lifelines by Chelsey Dulaney and Rory Jones (WSJ)

Oil-rich economies are seeing a massive inflow of cash amidst high energy prices. Some are using that cash to support other countries that are reeling under balance of payments stress and natural disaster crises. [Link; paywall]

Electric Vehicles

Tesla Shifts Battery Strategy as It Seeks U.S. Tax Credits by Rebecca Elliott and Mike Colias (WSJ)

The passage of the Inflation Reduction Act earlier this year is already driving companies to re-think their approach to offshoring and supply chain design as the world’s largest EV maker may be switching battery production from Germany to the US. [Link; paywall]

Ford Reveals New EV-Selling Rules to Dealers by Nora Eckert (WSJ)

The Big Blue Oval is rolling out a new approach to selling EVs which will require no-haggle prices. New infrastructure for charging will also be a must. [Link; paywall]

Surgical Science

I Wish I Was a Little Bit Taller by Chris Gayomali (GQ)

Men who want to be a little bit taller are undertaking a dangerous surgery designed to lengthen their legs and add a few inches via broken femurs, titanium rods, and a lot of pain. [Link]

An ACL Tear That Heals Itself? by Aylin Woodward (WSJ)

Imagine your body re-growing its own ACL? A new generation of biologic treatments that create a scaffold for the ligament to grow on is being used to replace the injured tissue. [Link; paywall]

Scarcity & Abundance

Low-Paid Workers Face Worst-Ever Financial Crisis, Study Finds by Alan Jones (Press Association/Bloomberg)

The Living Wage Foundation surveyed low-wage workers and discovered more than half have used a food bank over the past year with almost as many regularly skipping meals. [Link; soft paywall]

From Shortage to Glut: Scotts Miracle-Gro Is Buried in Fertilizer by Thomas Gryta (WSJ)

The huge boom in consumer demand during the pandemic convinced goods producers and importers to ramp up their inventories. Now, that demand isn’t appearing to the same degree that was expected, a glut of inventories and over-production remains. [Link; soft paywall]

Global Food Supply Faces Fresh Turmoil With Rice Set to Climb by Patpicha Tanakasempipat, Pratik Parija, and Mai Ngoc Chau (Bloomberg)

Export controls in India are expected to drive up the price of rice globally. Global production has already been curtailed by weather and the shock of other crop prices soaring earlier this year. [Link; soft paywall]

Ukraine

Ukraine Pulled Off a Masterstroke by Phillips Payson O’Brien (The Atlantic)

The offensive that let Ukraine retake large swathes of Kharkiv Oblast in a dramatic breakout was part of a broader strategic feint which has played out over the entire summer. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

What a Way to Start the Weekend

If you’ve been in a particularly bad mood heading into weekends this year, you’re obviously paying pretty close attention to the markets. With today’s decline, the S&P 500 is in the familiar position of ending the week with a decline of 1% or more. If the current declines hold up into the close, it will be the 12th daily drop of 1% or more to end a week this year. Going back to 1952 when the five trading day week started, there have only been five other years (1974, 2000, 2001, 2002, and 2008) where there were as many or more down 1% Fridays (or last trading day of the week) in a given year. As you might expect, all five of those years were lousy for the stock market.

While this year is currently tied for having the fourth-highest number of 1%+ down days, the year isn’t even three-quarters done (heaven help us). After today there are still another 15 weeks left in the year, so there is plenty of time to move up the rankings. On a percentage basis, the S&P 500 has closed down at least 1% on the last trading day of the week just under a third (32.4%) of the time, and if that pace were to keep up for the remainder of the year, 2022 would easily set the record for the highest frequency of 1% declines to close out the week. Never have we needed a happy hour more than this year. Click here to learn more about Bespoke’s premium stock market research service.

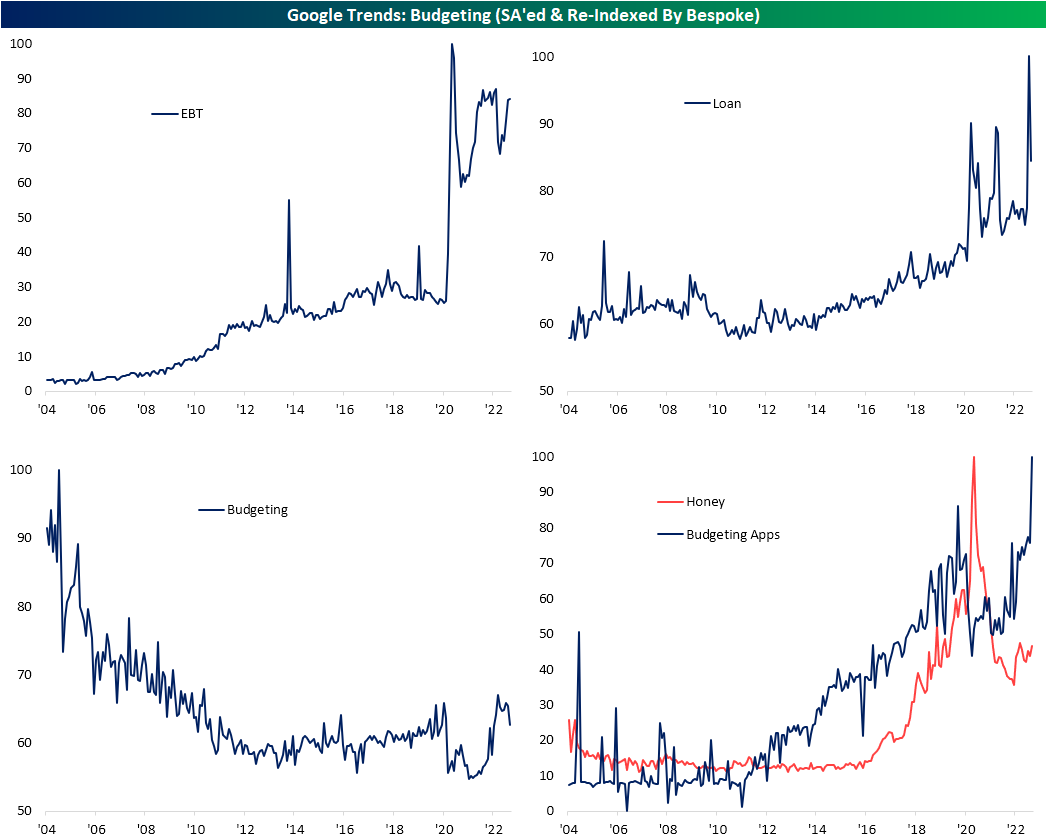

Google Trends: Tightening The Belt

Earlier this week, a hotter-than-expected CPI print countered the belief that inflation has peaked. Even with that CPI report, though, there have been a number of other indicators pointing to the opposite. For example, readings on prices from various PMIs have rolled over and PPI decelerated dramatically. Some other evidence can be found in Google searches. Google Trends provides tracking of search interest for a provided search term. Lower readings indicate fewer Google searches for a provided term whereas higher readings indicate elevated search interest with these series indexed to their peak reading. In the charts below, we have adjusted these series for seasonality and re-indexed them so that like the raw data, peak readings are indexed to 100.

Searches for “inflation” surged during the pandemic and reached a record high in August. So far in September, that reading remains extremely elevated but it has pulled back significantly. The month isn’t over yet, so time will tell if searches for inflation have in actuality reversed to that degree, but the peaks for related terms have moved even further in the rearview. For example, searches for “costs”, “high costs”, and “expensive” all surged in the first half of the year reaching a high in the spring. Since then, these readings have been on the decline, although, searches for “expensive” and “high costs” remain well above levels observed in years prior.

Taking a more granular look at specific consumer expenses shows a bit more nuanced picture. Rent has been one of, if not the, biggest single driver for CPI recently as we noted in our recap of the latest CPI release. Search interest appears to back that up as searches for the term “rent cost” have exploded higher. Even though it remains well above readings from any other period since the data begins in 2004, that reading has rolled over in the past few months. As for other housing costs, searches for “Utilities Bill” and “Electric Bill” are at and nearing record highs, respectively, after rising sharply in the past year. Those higher readings are understandable as energy prices have skyrocketed, but gasoline prices are much lower than they were at the start of the summer and search interest has reflected that. Regardless, higher gas prices makes driving less attractive. In turn, searches for “car pool” are much higher than they were at other times in the pandemic years.

Grocery and food-related searches have also spiked in recent months indicating people are looking into why they are paying more when they head to the store. Again though, similar to rent, these readings have in fact started to roll over in the past few months.

There is only so much the average consumer can do to fight inflation, and the Google Trends data provides some insight into what people are doing to cope with higher costs. For starters, searches for Electronic Benefits Transfer, or EBT, exploded at the start of the pandemic and have remained extremely elevated relative to pre-pandemic levels. Current search interest levels are below the highs from the early days of the pandemic, but they have also begun to rise toward the upper end of the range over the past several months. Meanwhile, searches for “loan” have seen a structural move higher since the pandemic began as well with a particularly sharp increase in recent months.

Searches for “budgeting” used to be much higher in the first decade of the 2000s but as technology increasingly engrained itself into society, those searches appeared to have been replaced by searches for “budgeting apps”. One more specific example is the popular Paypal (PYPL) owned Google Chrome extension Honey which automatically applies coupon/discount codes to online purchases. Over the past year, interest in each of these terms have risen as inflation remains elevated and consumers look for ways to tighten their belts. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 9/16/22 – At Least He Warned Us

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.” – Jerome Powell

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s looking like another day of declines heading into the weekend after FedEx (FDX) lowered guidance last night, making an already weak backdrop even weaker. FDX wasn’t the only company to warn since the close yesterday. Companies like GE and Huntsman (HUN) also lowered guidance citing issues like supply chain bottlenecks and high energy costs. If the S&P 500 does finish down 1% today, it will be the sixth straight week of a gain or loss of 1%+ on the last trading day of the week. That would be the longest streak since May 2020 (ten weeks) and tied for the second-longest streak since at least 1952 (when the five-day trading week on the NYSE started).

The only economic report on the calendar is the Michigan Sentiment report at 10 AM Eastern. Economists expect the headline reading to bounce to 60.0 from 58.2 at its last read. The most important aspect of the report to watch, though, is inflation expectations. In that respect, economists are expecting one-year inflation expectations to fall to 4.6% from 4.8% while 5-10 year inflation expectations are forecast to remain unchanged at 2.9%.

When Powell said back in August that businesses and households would feel ‘pain’ from higher interest rates he wasn’t lying, but is a situation like FedEx (FDX) what he had in mind? The stock is currently trading down over 20% in the pre-market which would rank as the worst single-day decline for the stock since its IPO in 1978. Declines of this magnitude weren’t even felt during the 1987 crash, the financial crisis, or during the COVID crash. At the open today, FDX will still be well above its COVID lows (when global trade essentially shut down temporarily), but it will be right at levels it was trading at right before COVID hit US shores.

Given the trends we have seen this year, you would have expected FDX to be blaming increased labor and energy costs as well as supply chain bottlenecks for the weakness in results, but those issues were notably absent. Instead, FDX cited “global volume softness that accelerated in the final weeks of the quarter” and “macroeconomic weakness in Asia and service challenges in Europe”. With a warning like this, it raises the question of whether the Fed is too busy fighting yesterday’s battle and missing what’s on the horizon.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

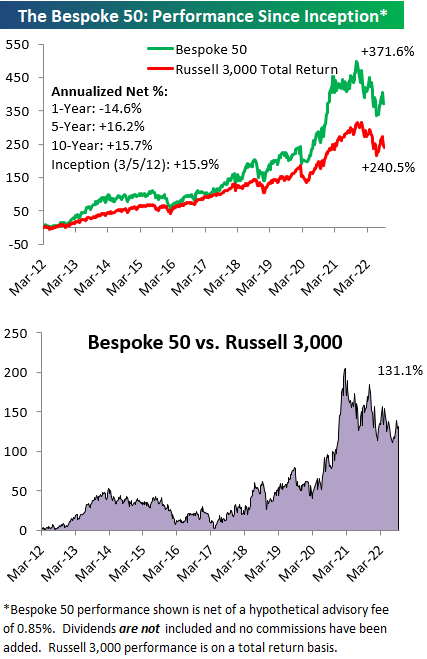

The Bespoke 50 Growth Stocks — 9/15/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Sentiment Contradicts Price Action

The S&P 500 may have fallen around 1.5% over the past week, but individual investors have reportedly become increasingly bullish. 26.1% of responses to the weekly AAII sentiment survey reported as bullish this week, up from a recent low of 18.1% last week. With the S&P 500’s worst day in since June 2020 and a hotter-than-expected CPI print occurring late in the response collection period (12:01 AM on Thursday through 11:59 PM Wednesday night), the timing of responses is a potential cause for the increase in optimism that was contrary to equities’ price action. In other words, responses that came in prior to Tuesday were likely far more bullish than those that came in afterward and therefore elevating the level of bullish sentiment. As such, next week will be a more telling read on individual investor sentiment as it will more fully capture recent price action and inflation data.

While bulls rose back above a quarter of responses, bears fell back below 50%. Bearish sentiment dropped to 46% which was only the lowest level since the week of August 24th.

Those moves meant the bull-bear spread rose 15.3 points week over week going from -35.2 up to -19.9. That was the largest one-week jump in the reading since the end of June. However, that indicates sentiment remains heavily in favor of pessimism as the streak of negative readings grows to 24 weeks long; the second longest streak of negative readings on record.

The AAII survey was not alone in showing a rebound in sentiment. Both the Investors Intelligence survey and the NAAIM Exposure Index highlighted increased bullishness in the latest week’s data. As with the AAII survey, though, the collection periods likely did not fully capture the effects of Tuesday’s inflation data and historic one-day decline. Overall, the story remains that investors are remarkably bearish. Click here to learn more about Bespoke’s premium stock market research service.