Intraday Action Continues to Trump After Hours

Over the past couple of sessions as the market has awaited Fed Chair Powell’s testimony, the S&P 500 (SPY) has not seen particularly large gaps at the open. In fact, both on Tuesday and Wednesday, the opening gap was less than 5 bps in absolute terms. That is the first time with such tiny opening gaps in back to back days since December 28th. That being said, following the small opening gap yesterday, SPY would go on to have a much more volatile session intraday as it fell over 1.5% from open to close.

In the table below, we show each other time in SPY’s history that there has been an opening gap down of less than 5 bps followed by a decline of more than 150 bps from open to close as was the case yesterday. These types of moves have been rare with only 11 prior instances, the most recent of which was in August of last year. While today saw another small opening gap and has struggled to find a direction so far, following prior instances the S&P 500 has tended to fall further the following session with average declines one week out as well. While things generally appear more positive one month to three months out, returns are mixed relative to the norm. Meanwhile, 6 month returns tend to be much weaker than the norm with a median decline of 1.6% versus the median for all of SPY’s history of a 5.32% gain.

The past couple of days’ price action in which most of the move happens intraday is a bit unusual in another way as well. As we have noted in the past and show in the first chart below, going back to the start of SPY’s trading in 1993, nearly all of the its gains have come outside of regular trading hours. In other words, the moves in the past couple of sessions have essentially been the opposite of what is historically normal. However, that oddity is not exactly new. As we first noted roughly a month ago, for most of 2023 the after hours strategy of buying the close then selling the open has dramatically underperformed the opposite strategy of only owning when the market is open. Although that relative performance has waned a little given the past couple of days’ moves, the point stands that most of the S&P 500’s move is happening during regular trading hours in 2023. As is always the case, past performance is no guarantee of future results. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Consumer Pulse Report — March 2023

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke’s Morning Lineup – 3/8/23 – Powell, Round Two

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Impossible is not a fact. It’s an opinion.” – Muhammad Ali

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After modest gains overnight and earlier this morning, futures have slipped modestly into the red following yesterday’s Powell-induced decline. While past declines in response to Powell’s comments have sometimes been justified due to seemingly abrupt changes in policy, moving targets, and/or inconsistencies in his remarks, yesterday’s testimony in front of the Senate contained essentially nothing Fed officials haven’t been saying for the last several weeks, so either the markets didn’t believe what they were hearing for the last month or yesterday was an overreaction.

Markets in Europe are modestly lower at the moment in a follow-through from yesterday and more hawkish commentary from an ECB official who noted that the bank will continue hiking rates for a period of time after the March meeting. These comments came as Q4 GDP was weaker than expected, and German Retail Sales unexpectedly declined.

Speaking of Europe, while its economy has been lagging behind the US, stocks in the region have continued their recent outperformance of stocks here in the US. The first chart below shows the performance of the FTSE Europe ETF (VGK). After a sharp rally off its October lows, VGK has been in a sideways range for most of 2023 but has still managed to trade within a close range of its 52-week high. After yesterday’s decline, in fact, VGK was just 7% from a 52-week high.

US stocks, meanwhile, have been much weaker. While the rally in VGK took it back near its highs from last Spring, the rally in the S&P 500 ETF (SPY) barely even took it back above its December highs let alone the peaks from August and April. After yesterday’s decline, SPY was twice as far below its 52-week high (-14%) as VGK.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Fedspeak Review as Powell Goes to Capitol Hill

Fed Chair Powell’s testimony on Capitol Hill over the next couple of days will be the main focus of the market, and with perceived hawkish commentary today, things don’t appear to be off to a good start. As Chair Powell highlighted, stronger-than-expected economic and inflation data has lifted expectations for interest rates which has resulted in the S&P 500 erasing earlier gains and trading down 1% on the session as of late morning.

Using data from our Fedspeak Monitor, in the chart below we show the historical average performance of the S&P 500 on days in which there is Fedspeak going back to 2018 when Powell took over as Chair (that only looks at actual Fed speakers and excludes any reports like the Beige Book, FOMC Meetings, and Meeting Minute releases which we also cover in our Fedspeak Monitor). As might be expected, hawkish commentary generally tends to be received poorly by the market with the S&P falling an average of 7.5 bps on those days compared to a 9.2 bps gain on days with dovish commentary. As for times when the speaker is Chair Powell, a hawkish tone tends to see the S&P 500 react with a decline, however, the 5.8 bps drop is smaller than the norm. That contrasts with Powell’s dovish commentary having been far more well-received by the market. More broadly, and perhaps more surprisingly, any time an active voting member of the FOMC is the speaker the average move in the S&P 500 tends to be smaller in magnitude than when it is a non-voter speaker regardless of whether the tones are hawkish or dovish. ratesd Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 3/7/23 – Powell Takes the Mound

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Observation is a dying art.” – Stanley Kubrick

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s been a wild ride for natural gas over the last two trading days. After an 8% rally Friday, natural gas plunged more than 14% on Monday for its largest one-day decline since June 30th and its 15th worst day since 1990. 2023 is barely more than two months old, but yesterday’s decline was the 5th time this year that natural gas had a single-day move (up or down) of 10%+, and that follows last year when there were a record 18 daily 10%+ moves. If the pace of volatility that natural gas has seen so far this year were to continue for the remainder of the year, there would be 28 single-day moves of 10%+. For some perspective, before last year there were just three years (1996, 2001, and 2009) where natural gas experienced ten or more single-day moves of 10%+.

The record volatility of natural gas can be further illustrated by looking at the commodity’s average daily move over a rolling 200-trading day period. Before 2022, the average daily percentage move in natural gas prices never exceeded 3.8% and from 2012 right up until COVID, the average daily move never exceeded 2.6%. Covid and the war in Ukraine changed all that, and nowadays, on any given day, a daily move of 4.6% in natural gas has become the norm as this degree of volatility in the commodity has never been experienced before.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

B.I.G. Tips – Q4 2022 Earnings; Triple Plays

Today we published our newest Earnings Triple Plays report. This season there were a total of 105 earnings triple plays out of just under 2,000 individual quarterly earnings reports from US-listed stocks.

What is a triple play? When a stock reports quarterly earnings, it registers a “triple play” when it beats analyst EPS estimates, beats analyst revenue estimates, and raises forward guidance. We coined the term back in the mid-2000s, and you can read more about it at Investopedia.com. We consider triple plays to be the cream of the crop of earnings season, and we’re constantly finding new long-term opportunities from this basket of names each quarter. You can track the newest earnings triple plays on a daily basis at our Triple Plays page if you’re a Bespoke Premium or Bespoke Institutional member. To read our newest report and see some of the triple plays with intriguing charts at the moment, start a two-week trial to Bespoke Premium!

Bespoke’s Morning Lineup – 3/6/23 – Take Two of These and Call Me in the Morning

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing a couple of aspirin can’t cure.” – Peggy Olson, Mad Men

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The headlines say that the market’s fate all comes down to the next 13 trading days, but this ‘important’ period for the market is starting off slowly. Equity futures are oscillating around the unchanged line even as Treasury yields and commodities have pulled back. Crude oil down over 1% while natural gas plunges more than 12% on little news. Just to illustrate how quiet things are this morning, bitcoin is down less than 5 dollars – not percent – but dollars!

It may be quiet this morning, but the market has been giving headaches to both bears and bulls in the last several weeks. A quick look at a chart of the S&P 500 illustrates the frustration being felt on both sides. On a side note, it was ironic to see this morning that Bayer filed its patent for the ultimate headache cure (or at least one of them), aspirin, on this day in 1899.

In late January/early February, the S&P 500 broke above its December highs and its 200-day moving average forming what looked like the first real higher high since the peak in early January. At that point, the S&P 500 was further above its 200-DMA than at any point since it first broke below that level early last year. Then, the January employment report was released.

January’s much stronger-than-expected employment report coupled with a strong Retail Sales report and higher-than-expected inflation data, shifted the narrative quickly back to one where things were overheating and inflation was going to turn higher. The market quickly reacted with a radical shift in market pricing for Fed policy as Treasury yields surged. Stocks immediately reversed much of the gains from January, and the Dow actually ticked into the red for the year. The S&P 500’s pullback wasn’t as bad, but late in the month, it was back below its 50-DMA and once again testing its 200-DMA.

An intraday bounce on that first test briefly rekindled some optimism, but by last Thursday morning, the S&P 500 was back below its 200-DMA and both bears and bulls started to prepare for another leg lower. As hope was fading, stocks staged an intraday rebound that continued right into Friday. Now, heading into the new trading week, the S&P 500 is back above its 200-DMA and 3% above Thursday’s lows. Bulls are feeling confident again, but with Jay Powell scheduled to testify tomorrow, the employment report coming out Friday, and then CPI next week, don’t start snorting at the bears just yet, they may just need that aspirin back by next week.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 3/5/23

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Climate Disruption

As Oil Companies Stay Lean, Workers Move to Renewable Energy by Clifford Krauss (NYT)

While energy companies avoid adding headcount and keep a laser focus on cashflows, renewables are rapidly scaling up and are poaching talent in the process, meaning American jobs are rapidly shifting from the oilpatch to wind and solar farms. [Link; soft paywall]

California senate pushes to stabilize the homeowners insurance market by Morgan Rynor (MSN/KFMB San Diego)

After a catastrophic run of forest fires, fire insurance in California is either not available at all or becoming prohibitively expensive, making homeowners far more vulnerable to the still-significant fire risk that has beset much of the state. [Link]

Prices

Column: With winter almost over, Europe’s gas stocks are at seasonal record high by John Kemp (Reuters)

With winter winding down, EU and UK gas storage is still 61% full, with more than 680 terawatt hours worth of gas in inventory. That offers hope that building supplies ahead of next winter will be a much easier task. [Link]

Sellers’ Inflation, Profits and Conflict: Why can Large Firms Hike Prices in an Emergency? by Isabella M. Weber and Evan Wasner (UMass Amherst Economics Working Papers)

New research that argues post-COVID inflation is mostly about expanding market power and margins rather than excessive demand. [Link]

Lilly to cut some list prices by 70% and offer $25 insulin by Bhanvi Satija and Patrick Wingrove (Reuters)

After a $35 price cap on insulin was extended to most Americans who have insurance, drugmakers have made equivalent cuts to the out-of-pocket costs of their drugs in a move that will make it much easier for diabetics to access insulin. [Link; registration required]

Ukraine

In an Epic Battle of Tanks, Russia Was Routed, Repeating Earlier Mistakes by Andrew E. Kramer (NYT)

The latest egregious blunder from Russian war planners: massed tank attacks with little infantry support or tactical flexibility to deal with ambushes, mines, and Ukrainian anti-tank doctrine. [Link; soft paywall]

Trapped In The Trenches In Ukraine by Luke Mogelson (NYer)

Remarkable dispatches from the front lines of the war in Ukraine. A very long read, but filled with incredible and engaging detail about the soldiers and environment on the battlefield. [Link; soft paywall]

National Defense

‘Havana Syndrome’ Not Caused By Energy Weapon Or Foreign Adversary, Intelligence Review Finds by Shane Harris and John Hudson (WaPo)

The malady blamed on some sort of energy weapon wielded by foreign adversaries is much more quotidian than science fiction, an embarrassing challenge to a narrative that had treated ‘Havana syndrome’ as some sort technological wonder. [Link; soft paywall]

The First Battle of the Next War by Mark F. Cancian, Matthew Cancian, and Eric Heginbotham (CSIS International Security Program)

This report summarizes the findings of a wargame run by the CSIS and designed to simulate Chinese invasion of Taiwan. The result of US/Taiwanese/Japanese resistance to a Chinese invasion is typically success but at massive cost; generally, the failure is thanks to stiff Taiwanese resistance once Chinese troops have landed. [Link; 165 pg PDF]

Crypto

Crypto Companies Behind Tether Used Falsified Documents and Shell Companies to Get Bank Accounts by Ben Foldy and Ada Hui (WSJ)

One of the owners of Tether Holdings, issuer of the tether stablecoin, admitted an effort to “circumvent the banking system by providing fake sales invoices and contracts for each deposit and withdrawal” per emails review by the WSJ. [Link; paywall]

ETFs

Are you short Jim or long Jim? by Alexandra Scaggs (FTAV)

Want to bet on or against the stocks that are mentioned by CNBC personality Jim Cramer? Luckily there are now ETFs for each. [Link; soft paywall]

Time Marches On

US senators reintroduce bill to make daylight saving time permanent by David Shepardson (Reuters)

A bipartisan group of 12 Senators wants to do away with twice-per-year clock changes in favor of a year-round constant time. [Link; registration required]

Guns

74,000 & growing: Some NC police departments stockpile guns rather than release them by Virginia Bridges (The Charlotte Observer)

Police departments in the 10 largest cities across North Carolina number 74,000 and counting as firearms seized during police actions sit in storage. State law bans cops from destroying guns for any reason. [Link; soft paywall]

Social Media

I Gave Into The New Twitter Algorithm And I Went Way Too Viral by Ryan Broderick (Garbage Day)

An anecdotal but convincing analysis of what is making Twitter’s algorithm tick these days, and a depressing accounting of how much the site has deteriorated. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Bespoke’s Morning Lineup – 3/3/23 – Three Was Enough?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“For the execution of the journey to the Indies I did not make use of intelligence, mathematics or maps.” – Christopher Columbus

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After three weeks of declines, it was looking like March would only add to the tally. Thursday’s rally pushed the S&P 500 into positive territory for the week, though, and with futures indicated higher now, equities are on pace for a positive week…if they can get through today. It’s a relatively quiet day on the economic calendar today with PMIs for the services sector, the only reports scheduled for release. These are important indicators to watch for signs of whether or not the economy is running too hot, and the international versions of these reports released this morning showed strength. January’s economic data fed a narrative that the economy just wouldn’t quit even as the Fed tried its best to squash it. This week’s data for February like Consumer Confidence, Chicago PMI, and ISM Manufacturing, though, weren’t exactly positive, and they all missed expectations.

One area of the markets not rallying this morning is crypto. After a 50% rally through its high over Presidents’ Day weekend, bitcoin has been correcting for the last two weeks capped off with a 4%+ decline in early trading today. After today’s drop, the pullback is close to 10%, and bitcoin is on pace to close below its 50-day moving average (DMA) for the first time in nearly two months.

A break below the 50-DMA is typically considered a bearish signal, but in bitcoin’s case, this type of pattern hasn’t been followed by a clear trend. During the parabolic runup from 2016 through 2017, any time bitcoin closed below its 50-day moving average after trading above it for at least 50 days it almost always immediately recovered to new highs. Beginning in 2018, though, bitcoin was slower to recover following these types of breaks. In three of the four periods since the start of 2018, prices experienced pretty sizable pullbacks at least in the short term, but they were still always followed by new highs. In dollar terms, last year’s pullback in bitcoin was unlike any other, but in percentage terms, it has been in this type of situation before. As bitcoin has ‘matured’ it has tended to follow more typical technical patterns versus the early days when all it did was win, so a pause in this year’s rally, at least in the short-term, wouldn’t be surprising.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

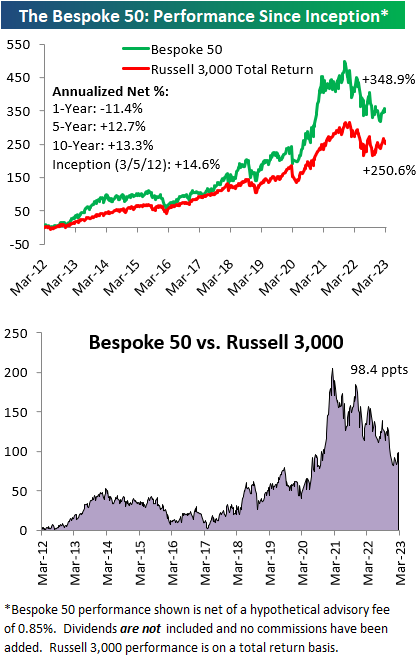

The Bespoke 50 Growth Stocks — 3/2/23

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were three changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.