March Volatility Emerging

The month of March is nearly halfway through and volatility has begun to pick up. Whereas the S&P 500 was up around 2% month to date as of this time last week, currently the index is down over 2.5%. As shown below, since the end of WWII March ranks in the middle of the pack with regards to the average spread between its Intra month high and low (on a closing basis). That compares with months like October—the most volatile of the year—which has averaged an Intra month range of just under 8%.

Although historically March might not be the most volatile month, in recent years that Intra month volatility has kicked up. In the chart below we show the spread between March’s Intra month highs and lows for each year since the end of WWII. Over time, there has consistently been some ebb and flow in this reading with some outlier years in particularly volatile times like the late 1990s and early 2000s and then of course 2020. October has historically been known as a month for market turnarounds, but March has become increasingly active on that front as well. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 3/13/23 – Seven Dangerous Words

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The fundamentals of America’s economy are strong.” – John McCain 4/17/08

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Phrases like the seven words above never seem to be made when markets and the economy are running smoothly, and we’ve heard a number of similar phrases like this made by officials over the weekend and this morning. That’s definitely not to say that the events of the last week and today are a repeat of 2008, but these types of comments almost never have their intended purpose of providing comfort to investors.

What’s happened over the weekend has been notable and will have both intended and unintended ramifications down the line. With deposits at US banks having essentially been backstopped by the actions of the Federal Government, one could argue that the banking system has been de facto nationalized, and the consequences of that are completely unknown, so we won’t even begin to speculate.

The flight to safety has been incredibly pronounced in the Treasury market as the 2-year yield is down nearly 50 basis points (bps) this morning after falling 29 bps on Friday and 20 bps Thursday. What’s truly remarkable about these declines is that they came just after the 2-year yield topped 5% for the first time since June 2007. Going all the way back to 1977, the last time the 2-year yield dropped more than this in a three-day span was just after the 1987 crash, and then before that, it happened in multiple periods from late 1979 through early 1983.

Finally, despite little direct connection between what’s going on with SVB and other US regional banks, European bank stocks have also seen sharp declines in the last two days as the STOXX 600 Bank Index is down over 9%. Analysts are out defending the banks as having ‘limited risk’. That may be true with regards to SVB and other regional US banks specifically, but European banks aren’t immune to the overall trend impacting US banks (a rapid surge in interest rates shortly after central bank officials were assuring markets that any increase in rates would be gradual).

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 3/12/23

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Entertainment

WWE in talks with state gambling regulators to legalize betting on scripted match results by Alex Sherman (CNBC)

Seeking to get in on the sports gambling goldrush, wrestling matches (which are scripted with results pre-determined) are trying to become legally sanctioned gambling events. [Link]

Why Are So Many Guys Obsessed With Master and Commander? by Gabriella Paiella (GQ)

An investigation into the enduring popularity of a mid-budget sailing movie set during the Napoleonic Wars which has persisted to become a near-obsession for men of a certain age. [Link]

The Stunt Awards by Bilge Ebiri and Brandon Streussnig (Vulture)

An important corrective to the glaring omissions of the traditional Academy Awards, which conspicuously overlook the stunt professions which make movies great. [Link]

Doom Loops

The Dollar’s Imperial Circle by Ozge Akinci, Gianluca Benigno, Serra Pelin, and Jonathan Turek (Liberty Street Economics)

A new model characterizes the dollar’s role in the global economy as a procyclical force which wrecks factory activity and commodity prices as the greenback gains steam. [Link]

North Carolina trucking company to shut down after top customer pulls out by Clarissa Hawes (FreightWaves)

Demands for “massive rate and volume concessions” from customers led FreightWorks to shutter the doors, laying off 200 employees including 140 drivers. [Link]

Real Estate

Millionaires row no more: Number of houses that cost seven figures nationwide is dropping by Swapna Venugopal Ramaswamy (USAToday)

Only about 7% of the US housing market is worth more than $1mm, a drop of 1.6 percentage points versus the peak of the market but still almost double the 4% at that price level from January of 2020. [Link; auto-playing video]

Ukraine

Dispatch From Kyiv: Ballet in a Time of War by Carol Schaeffer (The Nation)

Ballet, bombs, and the strange world of Kyiv which has been spared Russian occupation but is still a acutely war-time city as the invasion pushes through its second year. [Link; soft paywall]

Renewables

This geothermal startup showed its wells can be used like a giant underground battery by James Temple (MIT Technology Review)

A Nevada geothermal company thinks it may be able to turn its wells into what is in effect a giant battery, with important implications for keeping amperage flowing when renewable generation is no longer operating. [Link]

Unhappy Customers

How ‘Excuseflation’ Is Keeping Prices — and Corporate Profits — High by Tracy Alloway and Joe Wiesenthal (BNN/Bloomberg)

Corporations have been eager to push prices higher and take advantage of unique disruptions, driving prices higher with input costs but not returning the favor after input disruptions calm. [Link]

As Customer Problems Hit a Record High, More People Seek ‘Revenge’ by Katie Deighton (WSJ)

The National Customer Rage Survey has been run since 1976 and its 2023 edition showed a uniquely poisoned relationship between businesses in aggregate and their customers. [Link; paywall]

Elon

Bodyguards Follow Elon Musk Everywhere at Twitter HQ, Even to Restroom, Says Engineer by Philippe Naughton (The Daily Beast)

Employees report Twitter and Tesla CEO Elon Musk gets followed around the social media company’s headquarters by two bodyguards. [Link]

Elon Musk Is Planning a Texas Utopia—His Own Town By Kirsten Grind, Rebecca Elliott, Ted Mann, and Julie Bykowicz (WSJ)

The company town is back, this time plotting itself outside of Austin, TX. A “Texas utopia” is in the cards near SpaceX and Boring Co facilities in the Lone Star State. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

This Doesn’t Happen Often

After a surge earlier this week that took the yield on the two-year US Treasury up above 5% for the first time since 2007, concerns over the health of bank balance sheets have caused a sharp reversal lower. From a closing high of 5.07% on Wednesday, the yield on the two-year US Treasury has plummeted to 4.62% and is on pace for its largest two-day decline since September 2008. Remember that?

A 45 basis point (bps) two-day decline in the two-year yield has been extremely uncommon over the last 46 years. Of the 79 prior occurrences, two-thirds occurred during recessions, and the only times that a move of this magnitude did not occur either within six months before or after a recession were during the crash of 1987 (10/19 and 10/20) as well as 10/13/89 when the leveraged buyout of United Airlines fell through, resulting in a collapse of the junk bond market. As you can see from the New York Times headline the day after that 1989 plunge, just as investors are worrying today over whether we’re in for a repeat of the Financial Crisis, back then they were looking at ‘troubling similarities’ to the 1987 crash. The year that followed the October 1989 decline wasn’t a particularly positive period for equities, but a repeat of anything close to the 1987 crash never materialized. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 3/10/23 – Running into the Weekend

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I believe that banking institutions are more dangerous to our liberties than standing armies.” – Thomas Jefferson

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures are lower this morning heading into the 8:30 Non-Farm Payrolls report but given the action in SVB Financial (SIVB) which is trading down over 60% for the second straight day, the biggest surprise may be that futures aren’t even lower.

The February Non-Farm Payrolls report was just released and while it was mixed relative to expectations, it was generally positive for markets. Economists were expecting the headline reading to come in at 225K this morning, but the actual reading came in at 311K. Below the surface, though, the Unemployment rate was higher than expected, average hourly earnings were lower than expected, and average weekly hours were also lower than expected.

Yesterday was one of the worst days for bank stocks in years. In the 17 years that the S&P Regional Banking ETF (KRE) has been trading, Thursday’s 8.11% plunge was only the 22nd single-day decline of 7.5% or more, and it was the first since the COVID shock in early 2020. Before that, you have to go back to the debt limit and US credit rating downgrade of August 2011 to find the next occurrence when there was one day (8/8/11) when the ETF fell just under 10%. During the Financial Crisis, moves like yesterday’s almost seemed common. Whether yesterday was a one-day shock in the bank stocks or not remains to be seen, but based on the history of prior occurrences, like cockroaches, more often than not, when there’s one single-day large decline, others are usually lurking.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

50-DMAs Couldn’t Hold

Worries about banks today left major US index ETFs across the market cap spectrum back below their 50-day moving averages. The uptrend channels that have been formed over the last six months are also getting tested with this week’s move lower. You can see the current set-ups in the snapshot from our Chart Scanner tool below.

Looking at our Trend Analyzer, every sector ETF except for Technology has now moved back below its 50-day moving average. Six of eleven sectors are actually oversold (>1 standard deviation below 50-DMA), with Financials (XLF) and Health Care (XLV) at “extreme oversold” levels. XLF had been up more than 8% on the year about a month ago, but it’s now down 1.93% YTD.

Technology (XLK) and Utilities (XLU) are the only two sectors up over the last week. Interestingly, Utilities (XLU) has been one of the worst performing sectors so far this year, while Tech has been the best.

With Financials seeing such a sharp decline this week, below is a snapshot of various banks and brokers in the sector with the ones highlighted in red all now trading at least 5% below their 50-DMA. As shown, Charles Schwab (SCHW) is down the most over the last week with a decline of 12.6%, which has left it 16.4% below its 50-DMA and down nearly 20% on the year. Other names like Bank of America (BAC), JP Morgan (JPM), and Raymond James (RJF) are in extreme oversold territory as well. Of the major banks and brokers listed, Goldman Sachs (GS) has actually held up the best over the last week with a decline of just 2%. Click here to learn more about Bespoke’s premium stock market research service.

The Bespoke 50 Growth Stocks — 3/9/23

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

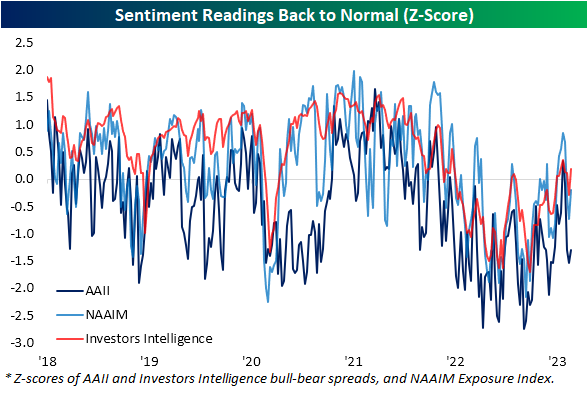

Bearish Sentiment Remains

The S&P 500’s swings higher and then lower over the past week have left sentiment little changed. For the American Association of Individual Investors’ (AAII) weekly survey, 24.8% of respondents reporting as bullish compared to 23.4% the previous week. That is the second higher reading in a row but still well below the recent high of 37.5% from one month ago.

Along with a modest bounce in bullishness, bearish sentiment has taken a modest decline falling from a recent high of 44.8% last week down to 41.7% today. That is the first decline in a month, leaving it in the middle of its range since the start of last year.

Given the moves in bullish and bearish sentiment, the bull-bear spread remains skewed in favor of bears for the third week in a row.

Following a sharp eight percentage point decline last week, neutral sentiment has bounced rising to 33.4%. Albeit higher, outside of last week, that reading would be the lowest since the end of 2022.

Although recent weeks have seen the AAII survey return to deeply bearish sentiment, other surveys are not nearly as pessimistic. While the AAII survey’s bull-bear spread sits well over a standard deviation below its historical average, the NAAIM Exposure index continues to show only modestly long positioning among active managers. Currently, that reading is 0.2 standard deviations below the historical norm. Meanwhile, the weekly Investors Intelligence survey is actually showing respondents are reporting as more bullish than has been historically normal. Click here to learn more about Bespoke’s premium stock market research service.

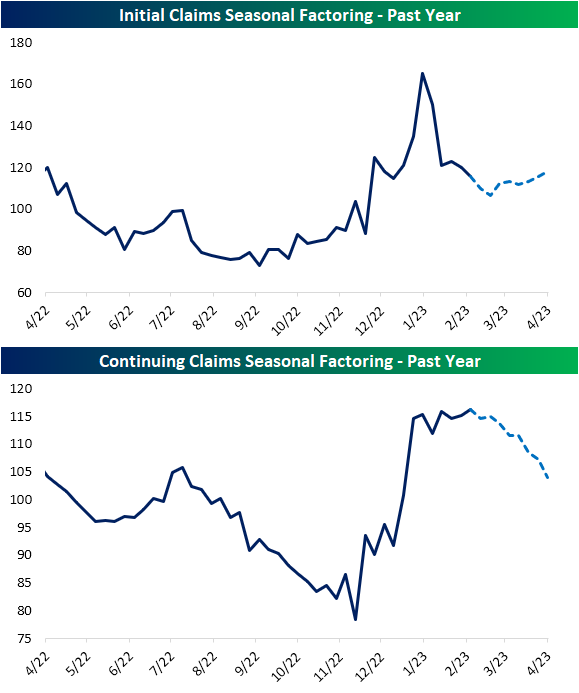

Seasonal Headwinds Dying Down for Claims

The S&P 500 is rallying this morning in the wake of today’s weekly jobless claims print which gave investors at least some hope that data is flying in the face of the Fed’s recent hawkishness. Whereas expectations called for initial claims to remain below 200K for the eighth week in a row, claims jumped by 21K to 211K. That is the highest reading since the week of December 24th.

As we have noted in recent weeks, although the seasonally adjusted number has gone on an impressive streak of sub-200K prints, the unadjusted number never fell below that threshold. This week saw the reading rise to 237.5K, the highest since only the second week of the year. As shown in the second chart below, the first few months of the year have historically seen claims fall with the current week standing out as one with consistently higher claims week over week. Although the direction of non-seasonally adjusted claims this week is not particularly unusual, the 35.4K increase was much larger than the historical median increase of 14k usually seen for the comparable week of the year.

All of that means that claims in general are following seasonal patterns as could be expected. In the charts below, we show the seasonal factors for initial and continuing claims. Essentially, those factors represent how elevated claims are above what has been normal historically (a reading of 100 would indicate a normal reading). Looking ahead over the next several weeks, seasonal headwinds will persist but not to the same degree as the first couple months of this year. As for continuing claims, the next several weeks will see seasonal factoring more consistently roll over even more sharply as we enter a period of the year with much less of a seasonal headwind.

Like initial claims, seasonally adjusted continuing claims came in above expectations this week rising back above 1.7 million. At current levels, claims matched the recent high from the week of December 17th which is back in the middle of the pre-pandemic range. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 3/9/23 – Happy Anniversary

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A minute’s success pays the failure of years.” – Robert Browning

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s been a relatively quiet morning in the markets today, but the bias had been negative as stocks in Europe are down about half of a percent. Economic data just released here in the US, though, showed that jobless claims came in above expectations with initial claims topping 200K and continuing claims topping 1.7 million. Both of these readings are the highest since December. In response to the weaker employment readings, futures have been rallying. Investors and the Fed may like this data, but you can bet that Senator Warren won’t be very happy. There’s no other data on the calendar today, so now the focus will shift to tomorrow’s February Non-Farm Payrolls.

It’s hard to believe it was 14 years ago when the S&P 500 finally made its financial crisis low setting the stage for a new bull market. Things weren’t looking good for the market or the global economy back then, but from the close on March 9, 2009, through yesterday (3/8/23), the S&P 500 rallied 490% which works out to an annualized return of 13.5%- without even including dividends!

Obviously, returns will look remarkable when you measure them from the absolute low, but what may be even more notable is to look at how an investor would have fared had they gone ‘all-in’ at the highs in October 2007 right before all hell broke loose.

The chart below shows the performance of the S&P 500 from its high on 10/9/07 through yesterday (3/8/23). Just over a year after that investment, you would have been down 50% on your way to a total decline of 57% but had you held on through those lows, your total gain since 10/9/07 would have been 155% which works out to 6.3% annualized and again, not including dividends. That’s obviously a lot less than the 13.5% annualized return you would have had from the lows in March 2009, but 6.3% still beats the level of yield you can currently get from any point on the US Treasury yield curve. The key word here is currently.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.