Mar 29, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

It’s the last day of the quarter and investors around the world are looking to end it on a bullish note. With the S&P 500 on pace for its best first quarter of the year since 1998, it may be hard to remember that the year didn’t start out on nearly that optimistic of a note. In fact, after a big decline of over 2% on the second trading day of 2019 (thanks to an Apple warning), the S&P 500 was off to its worst start of a year since 2000 and just the fifth year in its history that it was down more than 2% two trading days into the year. For all the strength in equities this quarter, though, they haven’t held a candle to crude oil which is up over 30% this year for its best quarter since Q2 2009!

Please click the link below to read today’s Bespoke Morning Lineup.

We highlighted the massive relative performance gap between the Technology sector and the Transports in last week’s Bespoke Report, and if you are a fan of Dow Theory, the underperformance of the Transports has been a source for concern. This week, the Transports put a small dent, or better yet, scratch into that streak of underperformance.

The chart below shows the relative strength of the Technology sector and the Transports relative to the S&P 500 (rising lines indicate outperformance versus the S&P 500). Beginning in late January, the two really started to diverge from each other, but this week have started to close what has been, and still is, an enormous gap between the two.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Mar 28, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

After four trading days of non-stop focus on the yield curve, investors are moving on to the new topic du jour as positive headlines with respect to China have provided a boost to equity futures. As they say, everything old is new again! The news this time around is that the Chinese government is planning to offer more access to its cloud computing market for foreign tech firms. While sentiment is positive right now, there’s a lot to focus on today with a number of economic indicators on the calendar and several FOMC speakers set to speak.

Please click the link below to read today’s Bespoke Morning Lineup.

Sentiment sure can shift quickly in financial markets, and the latest example comes from Brazil. Just a little more than a week ago, Brazil’s benchmark Ibovespa index crossed the 100,000 level on an intraday basis for the first time ever. While the index was still down over 40% in dollar-adjusted terms, crossing 100,000 was a pretty big deal.

The party didn’t last long, though. The Ibovespa was never able to close above 100,000 last week, and ever since then, we have seen steady selling. Just yesterday the index broke down through short-term support and is now down nearly 8% from its recent highs. This morning is also looking like more of the same at the open as Brazilian equities are set to open down about 1%. Easy come easy go.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Mar 27, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

The global frenzy for yield continues this morning as Mario Draghi made dovish comments suggesting more easing measures likely to come from the ECB in response to recent weakness in the economic headlines. US Treasuries are rallying again this morning, sending the yield on the 10-year to 2.38% and pushing the yield curve further into inverted territory at negative 6 basis points on the 10y/3m curve. In corporate news, Southwest Airlines (LUV) lowered guidance citing the grounding of the 737 MAX and adverse weather conditions. On a more positive note, both KB Homes (KBH) and Lennar (LEN) are trading up over 2.5% after reporting earnings.

Please click the link below to read today’s Bespoke Morning Lineup.

The chart below is from the second page of our Morning Lineup and shows where S&P 500 sectors are trading with respect to their trading ranges. For each sector, the circle represents where it is now, while the tail indicates where the sector was trading a week ago. In the chart, light red or green shading represents overbought or oversold readings (>1 standard deviation above or below 50-DMA), while dark red and dark green shading indicate extreme overbought or oversold readings (>2 standard deviations above or below 50-DMA).

Looking at the chart, can you tell which one isn’t like the others? While the S&P 500 and most sectors remain at short-term overbought levels, Financials have been hit hard and is not only the only sector trading below its 50-DMA, but it is also the only oversold sector. Keep in mind also, that this reading comes after yesterday’s rally where the sector handily outperformed the S&P 500 gaining over 1%. If there is one sector where the pain of an inverted yield curve was immediately felt, it was in the Financials!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Mar 26, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Equity investors around the world are breathing a global sigh of relief this morning as most equity markets have at least partially rebounded from Friday and Monday’s weakness. There’s a healthy dose of economic data coming up 8:30 with Housing Starts and Building Permits and then Consumer Confidence at 10 AM. Keep an eye on semis today as yesterday, they underperformed the broader market by a pretty wide margin, and then last night Samsung issued a profit warning. Semis have been the market’s leadership group for some time now, so bulls don’t want to see that group falter.

Please click the link below to read today’s Bespoke Morning Lineup.

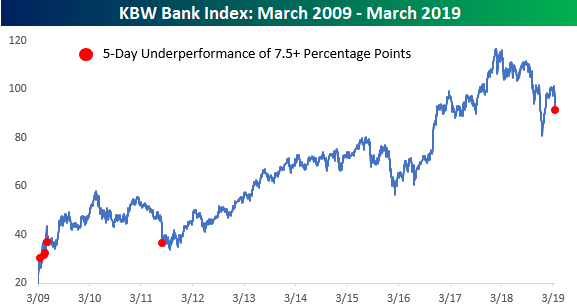

Things are looking up a bit today, but the last five trading days have been hell for bank stocks. After the KBW Bank Index briefly peaked above its 200-DMA last week for the first time since late September, it has been nothing but declines for the group ever since. During the last five trading days, the KBW Bank Index has seen daily declines of 1.32%, 3.02%, 1.53%, 3.92%, and 0.42%. In total, those declines work out to a five-day decline of just under 10% (9.83%) compared to a drop of just 1.22% for the S&P 500.

With bank stocks underperforming by more than 8 percentage points during this stretch, it goes down as the worst relative performance for the group since August 2011. Since the lows of the Financial Crisis, there have only been five other five day periods that saw similar underperformance, and all but the 2011 period occurred during the very early stages of the rally. You don’t see relative underperformance like this in the bank stocks very often.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Mar 25, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium. Below is an excerpt:

The weekend’s release of the Mueller Report did not have the kind of fireworks that some were looking for but that markets can’t stand. From a political perspective, we’re probably far from the end of hearing about Russia, the elections, and any obstruction, but based on the market’s complete lack of any reaction this morning, it has already moved on.

Markets will also be trying to move on from Friday’s sharp declines after the yield curve (10y/3m) inverted for the first time in over a decade, and with the curve back in positive territory this morning, that should help stabilize things for now. Don’t forget, though, that there are just six days left in the quarter, and shortly after that Q1 earnings season kicks off, so that should be, at a very minimum, an interesting period for equities.

Following in the heels of Friday’s sharp declines, Asian equities were hit hard overnight. For China, that meant that its streak of 1% gains to kick off the week ended at six. That was still enough to be the longest such streak of 1%+ gains in over a decade.

From a technical perspective, China’s rally is still intact. While the Shanghai Composite has been consolidating gains over the last two to three weeks, the short-term uptrend that has been in place since it broke out in late February remains intact.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Mar 22, 2019

Investors are scrambling for fixed income this morning after some truly bad economic data in Europe. 10-year bunds are back to negative yields and the US Treasury yield curve (10y vs 3m) is just 2 basis points (bps) from inversion. As you might expect, equity futures aren’t taking too kindly to the moves in fixed income and are looking to close out the week on a down note.

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/22/19

As noted in our Closer report last night, one of the defining characteristics of the rally off the Christmas Eve lows for the stock market was the trend of strong buying in the last hour of trading and right into the closing bell (light blue line), which is generally considered a positive market signal. That strength stood in stark contrast to the period from 9/21 through 12/24, where the S&P 500 typically sold off towards the close (red line). Over the last two weeks, late day buying power has started to weaken (dark blue line). Up to this point, we haven’t seen it turn outright negative, but it has shifted to a more neutral trend and something that bears watching in the weeks ahead.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.