Apr 8, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

It’s a pretty quiet start to the trading week with just modest moves overnight and this morning in foreign markets, and little in the way of movement in treasuries. Dow futures are being weighed down by Boeing (BA), which cut production guidance on Friday after the close and received a downgrade over at Merrill Lynch this morning. General Electric (GE) is also trading down 5% after JP Morgan downgraded the stock to underweight.

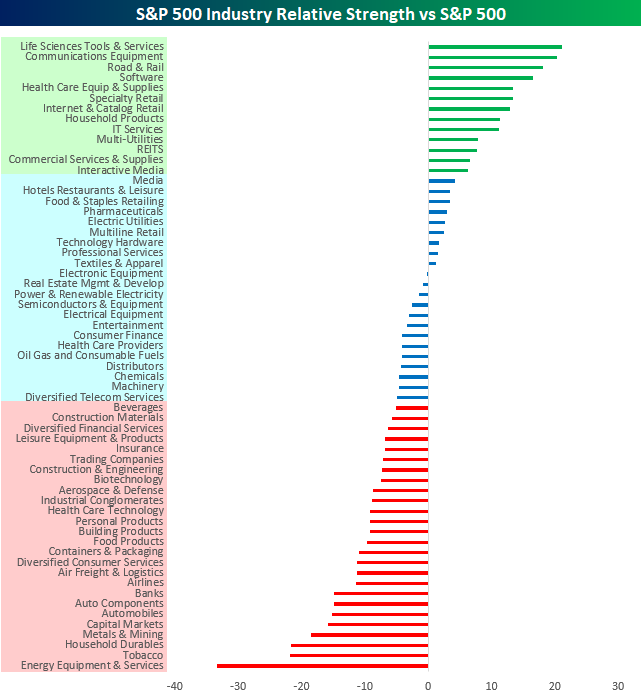

In this weekend’s Bespoke Report, we provided a detailed chart check-up and included snapshots of the setups for each of the S&P 500’s industries. To summarize how things looked on a group by group basis, the chart below summarizes the relative strength of each S&P industry’s performance versus the S&P 500 over the last year. Groups with green performance bars have significantly outperformed the S&P 500 over the last year, groups in blue are either modestly outperforming or underperforming the S&P 500, while groups in red have significantly underperformed in the last year. Leading the way higher, Life Sciences, Communications Equipment, and Road & Rail have been the top three performing groups, while Energy Equipment, Tobacco, and Household Durables have been the biggest laggards.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Apr 5, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

Ever since it moved back out of inversion last week, the yield curve has taken a back seat in the conversation. Currently, the spread between the 10-year and 3-month US treasuries is at 12 basis points, and if you look at the chart below, you can see that it has been trying to hook higher in the last couple of days. Where it goes in the short-term, though, is likely to be guided by today’s Non-Farm Payrolls report. A much better than expected reading will likely move the curve even steeper and dismiss further concerns over inversion, while a weaker than expected print has the real potential to move us much closer back to inversion and bring those concerns back to the fore.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Apr 4, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

US-China trade talks are in the spotlight again this morning as the President is set to meet with the Chinese Vice Premier shortly after the close this afternoon, and he just tweeted that talks are ‘moving along nicely’- a phrase we have been hearing for months now. Jobless Claims were just released and came in lower than expected at a 49-year low of 202K versus forecasts for 215K. We’ve said it numerous times before, but Jobless Claims continue to amaze! While not a new low, Continuing Claims also saw their largest weekly drop since November.

Yesterday marked the 100-day mark since the 2018 closing low in US equity markets. During that stretch, the S&P 500 has rallied 22%, which for most people would be considered a great year let alone a great quarter. Among various industries, though, some of the gains have been even more extraordinary. The table below lists the best and worst performing S&P 500 industries since the close on December 24th, along with each one’s overall weighting in the index.

As far as winners are concerned, there have been some big ones as 13 have seen gains of over 30%. Personal Products, a member of the Consumer Staples sector has led the way higher with a gain of just under 39%! Consumer Staples is not normally the sector that comes to mind when you think of big rallies, but there it is right at the top of the list! Behind Personal Products, Communications Equipment (36.5%), Construction & Engineering (36%), and Real Estate Management & Development have all gained 35% or more. While an industry from the Consumer Staples sector has been the top performer, industries from the Technology and Industrials sectors are the most well-represented with five and four, respectively.

On the downside, there hasn’t been any as every industry in the S&P 500 is up since the 12/24 lows! In terms of laggards, Health Care Providers and Diversified Consumer Services are the only two groups that are up less than 5%. Additionally, there are only two others that are up less than 10%. Hard to believe that being up over 10% in just over three month’s time can still be trailing the S&P 500 in a big way.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Apr 3, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

Just about anywhere you look around the globe this morning, the picture is the same. Equities are rallying and breaking above intermediate-term resistance levels in the process. US futures are indicating a higher open this morning on positive sentiment related to the never-ending US-China soap opera, but globally sentiment is improved as economic data showed encouraging improvement/stabilization. One negative economic data point just released, though, was the ADP Private Payrolls report which showed weaker than expected job gains in March (129K vs 175K estimate). So far, there has been little reaction from the market to the report.

The perfect way to illustrate the global nature of the rally is through a chart of the Bloomberg World Index. After breaking down below support just under 240 last fall, that level was poised to act as resistance on the way up. In its first test of that level last week, the Bloomberg World Index pulled back a bit, but it quickly regained its composure and bounced back above that level in this morning’s trade. There’s no arguing the fact that markets are overbought in the short term (a topic we cover in this morning report), but as long as these resistance turned support levels hold, bulls have the momentum.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Apr 2, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

We have a quiet day of economic data today as the only reports of note are Durable Goods and Auto Sales. Durable Goods were just released and showed a decline of 1.6% for their third monthly decline in the last four months. Equity futures are trading right around the unchanged level, which is actually an improvement from where they were trading overnight as bulls try and keep up the momentum going from Monday’s strong start to the quarter. One of the bigger stories, though, is crude oil, which just topped its 200-DMA for the first time since last October.

The days of the internet and online shopping being “just a fad” have come a long way over the years, but February’s Retail Sales report (released Monday) highlighted another of many major milestones that the growth of online shopping has reached over the years. In this case, it was the total share of Retail Sales that Non-Store retailers account for. Over the years this sector has been sucking up share at the expense of just about every other sector seeing its total share of sales rise from under 5% in the late-1990s to nearly 12% today. In February, Non-Store retail accounted for 11.813% of total sales overtaking General Merchanside (11.807%) for the fourth largest sector overall. Sure, we had to go out to three decimal places, so the margin of different is extremely small, but looking at the chart the trend remains clear; the share of total sales for each sector are clearly going in opposite directions.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Apr 1, 2019

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Equity markets around the world are kicking off the new quarter right where they left off in Q1. In Asia, stocks are once again back to “Monday Rally Mode” as stronger than expected PMI data in China has provided a boost. Meanwhile, in Europe equities are higher following weaker than expected PMI data. Finally, in the US futures are up over 0.5% and holding onto those gains even after weaker than expected Retail Sales data for February.

Please click the link below to read today’s Bespoke Morning Lineup.

With just under an hour to go before the second quarter kicks off, we wanted to highlight one last aspect of Q1 that warrants mentioning. Throughout the quarter, we frequently highlighted the market’s strong breadth here in the US (and many other places around the world). With that breadth holding up throughout the first three months of the year, the S&P 500’s cumulative A/D line for the entire quarter went down as the strongest going back to at least 1990 when our records begin.

The chart below shows the S&P 500’s cumulative A/D readings for each quarter going back to 1990. Not only was this quarter the strongest, but besides the first quarter of 2013, it wasn’t even really close as no other quarters even had a cumulative A/D line greater than 3,500!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.