Morning Lineup – Marking Time

It’s a big week on tap for financial markets as the FOMC meets on Tuesday and Wednesday. While odds of a cut at this meeting are low, with the probability of a cut at the July meeting still over 80%, investors will be looking for some direction as to whether those high odds are warranted or misplaced. Ahead of the meeting, investors have been pretty much sitting on their hands for the last several days not wanting to take a stand in either direction.

Please read today’s Morning Lineup for a recap of markets in Asia and Europe overnight and this morning, as well as a dive into the latest export numbers out of Singapore, suggesting that global trade activity remains healthy.

Bespoke Morning Lineup – 6/17/19

As mentioned above, investors have been on the sidelines over the last few days ahead of this Wednesday’s FOMC meeting, and the chart below from page two of the Morning Lineupillustrates that holding pattern. The fact that the S&P 500 and just about every sector have little or no tails on them indicates how little in the way of movement there has been over the last week.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Semis Spoil the Party

In a post on Wednesday, we highlighted the important juncture the semiconductor space was at, and unfortunately, the group didn’t take the bullish route. After failing to break out above resistance, last night’s earnings report from Broadcom (AVGO) dashed any hopes for the sector ending the week on a positive note and above resistance. The group is poised to open lower by close to 3% this morning as AVGO dampened the outlook for a second-half turnaround. Retail Sales, which haven’t exactly inspired confidence lately, actually came in relatively well, and Industrial Production and Capacity Utilization will be released later on. Please read today’s Morning Lineup for further analysis on AVGO’s earnings and the semis in general as well as a recap of some important overnight economic data in China.

Bespoke Morning Lineup – 6/14/19

Today’s decline in the semi ETF (SMH) will mark the 16th downside opening gap of more than 2.5% for the group over the last five years. Below we list each of those prior occurrences along with how SMH performed from the open to close. Overall, SMH has seen an average open to close gain of 0.76% (median 1.73%) following these downside gaps with gains 60% of the time. For each day, we also list the opening gap of SPY to show if the downside move in SMH was market-related or more specific to semis (like today’s move). As shown, the only time SMH gapped down this much or more while the S&P 500 saw a smaller downside gap was in October 2014.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – That’s No Bull

As one might expect given the big rally over the last several days, bullish sentiment on the part of individual investors ticked higher this week, but at just 26.8%, the latest sentiment survey from AAII shows that the vast majority of investors have been slow to get back in the pool as bearish sentiment remains elevated at 34.20% and the percentage of investors who just can’t make up their mind increased to 39%.

For today, all eyes are on Jobless Claims which came in at 222K versus estimates for a reading of 215K. Going forward, this afternoon’s earnings report from Broadcom (AVGO) will help to decide the path that semis take to close out the week. Please read today’s Morning Lineup for our latest take on events from overnight and this morning, including Industrial Production out of Europe and German Auto Exports.

Bespoke Morning Lineup – 6/13/19

On the subject of Industrial Production out of Europe, this morning’s print of a decline was right inline with expectations, but that doesn’t mean it was particularly good. As shown in the chart below, m/m readings have now only increased two times in the last eleven months!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Bounce in Japanese Cap Ex; Beware of Consensus

The ‘pause’ in the rally from yesterday’s early highs is continuing this morning as equity markets around the globe are all trading moderately lower, including the US. Please read today’s Morning Lineup for our latest take on events from overnight and this morning, including the latest on protests in Hong Kong, Credit Growth in China, and some solid economic data from Japan and France.

Bespoke Morning Lineup – 6/12/19

Beware of the consensus. As data and economic models have proliferated throughout the years, investors have increasingly become reliant on them to predict future events. If the ‘market’ or excel model says it’s going to happen, then we are all too ready to take it as a given. A perfect example is the path of Fed policy. With the futures market increasingly pricing in the likelihood that the Fed will cut rates, that’s what everyone now expects. As of this morning, for example, the futures market was pricing in a greater than a three-quarters chance that the FOMC will cut rates between now and the end of July. Three weeks ago, those odds were less than 15%!

So, it’s pretty much guaranteed that the Fed will cut rates and cut them aggressively right? While it’s certainly possible that we may see rate cuts in the months ahead, keep in mind that the consensus often gets it wrong and sometimes incredibly wrong. A perfect example is the 10-year US Treasury yield. The chart below is from a Wall Street Journal article earlier this week and shows how when it came to the direction of long term interest rates in 2019, the consensus couldn’t have been more wrong.

The chart shows the path of the 10-year yield so far in 2019 compared to various forecasts from Wall Street and the economic community. At the end of 2018, not a single economist expected the 10-year yield to be below 2.5% and the average forecast was closer to 3.0%. Right now, the 10-year yield is under 2.12%!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Small Business Sentiment Back on Track

After five straight months of declines from an all-time high back in August, it appears as though small business sentiment has gotten back on track. This morning’s release of the NFIB Index of Small Business Sentiment showed a larger than expected increase as the headline index came in at a level of 105.0 compared to estimates for a reading of 102.0. While the index is still off its record high of 108.8 from last August, it has risen for four straight months now, which is tied for the longest streak of increases since the four months that followed the 2016 election.

In other news, foreign equity markets are in rally mode once again despite relatively weak economic readings. In the US, PPI will be released shortly, but as the President already tweeted, “The United States has VERY LOW INFLATION, a beautiful thing!” Please read today’s Morning Lineup for our latest take on events from overnight and this morning.

As markets have started to recover, the yield curve is still inverted (as it has been for the last three weeks), but it has become less so over the last six trading days. As shown in the chart below, the curve has steepened from a low of negative 25 bps on June 3rd to 9 bps this morning. That’s the largest six-day steepening since October.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Merger Monday Provides a Positive Encore

After the first ‘perfect’ week for the DJIA since May 2018, a slew of mergers and the deal with Mexico are helping to kick off the week on a positive note providing a nice encore to last week’s gains. In terms of economic data, the week is starting off slow but will progressively pick up as the week goes on.

Please read today’s Morning Lineup for our latest take on events from the weekend, overnight, and this morning.

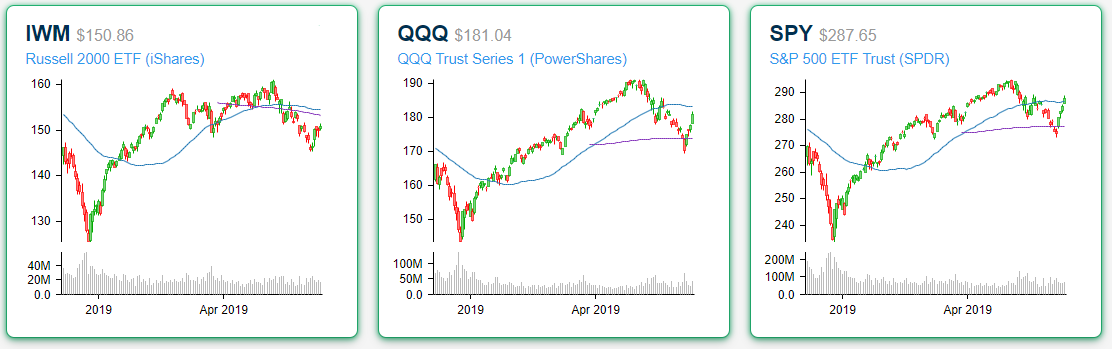

Sectors have seen quite a move within their trading ranges over the last week. As shown in the chart below, at this time a week ago the S&P 500 and every sector were trading below their 50-day moving averages and most were oversold. Fast forward five days and there are now just three sectors below their 50-DMA, and Energy is the only sector that is oversold. Meanwhile, both Consumer Staples and Utilities have moved back into ‘extreme’ overbought territory.

As far as the major averages are concerned, while the S&P 500 is trading back above its 50 and 200-DMAs, the Nasdaq 100 is still below its 50-DMA, and the Russell 2000 isn’t above either of those thresholds. If the rally is going to keep on going, they have a lot of catching up to do.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.